Silver, like gold, is a precious metal that offers investors protection during times of economic and political uncertainty.

After Russia’s invasion of Ukraine earlier this year, the flight to safety subsequently sent silver prices past the $26/oz mark, which was last seen in August, 2021.

This silver rally proved to be a flash in the pan, however. An aggressive interest rate hike campaign by the US Federal Reserve, along with a high US dollar, has kept the safe-haven metal in check.

Still, there are multiple reasons to believe that longer term, silver will rebound — possibly returning to levels last seen during the early 2021 Reddit-fueled silver frenzy.

Spot silver has already gained 20% over the last three months.

Source: Kitco

Source: Kitco

The potential forces behind silver’s next rally include: monetary demand, industrial demand, low inventories, physical market tightness, peak silver, and the gold-silver ratio.

Monetary demand

Soaring bond yields indicate that investors think the US Federal Reserve will do whatever is necessary to bring down inflation, and will succeed, without crashing the economy. But, once the Fed can no longer deny that it’s wrong about being able to control inflation, and that the economy is weaker than they think, it will go back to loose monetary policy, i.e., quantitative easing (good for gold & silver).

Gold is often touted as a smart means of portfolio diversification, beyond traditional stocks and bonds. However, new research by Oxford Economics advises that silver should also be included within a multi-asset investment portfolio.

The firm found investors would benefit from a 4 to 6% silver allocation, which is significantly higher than current holdings of silver by most institutional and retail investors.

Now, imo, would be an especially good time to start accumulating silver, or adding to an existing position, considering the inflationary environment we find ourselves in. Silver, like gold, is considered an excellent inflation hedge; unlike fiat currencies, silver does not lose its value when inflation erodes the purchasing power of a unit of currency.

Inflation is the fourth horseman

We are also on the brink of a recession, which is bad news for stock prices, but good news for precious metals. Silver and gold bulls like nothing more than an economic crisis, or geopolitical turmoil, to watch the value of their bullion grow. And while stocks enjoyed a November lift, technical analysis shows it was probably a dead-cat bounce.

The mother of all economic crises

In a recent letter to investors, Mark Spiegel of Stanphyl Capital said he believes the major indexes, though not all individual stocks, have considerably more downside — “the inevitable hangover from the biggest asset bubble in US history.”

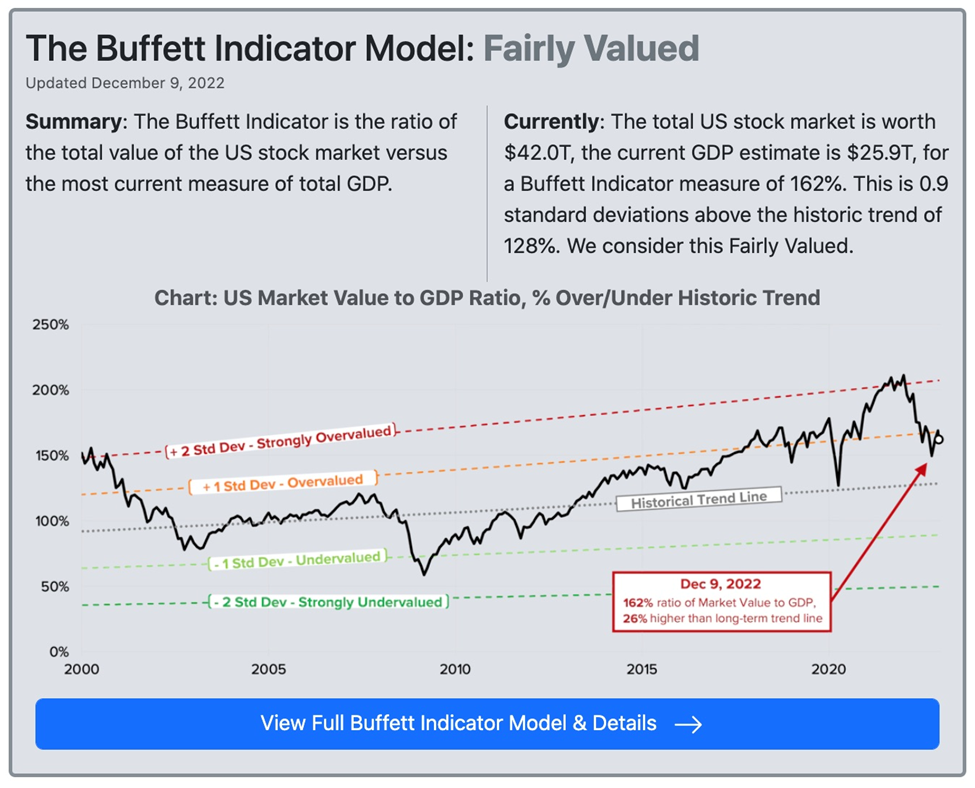

Spiegel via Quoth the Raven (Zero Hedge) also observes that the US stock market’s valuation as a percentage of GDP (the “Buffett Indicator”) is very high, and thus valuations have a long way to go before reaching “normalcy”. The indicator is currently sitting at 162%, 26% higher than the historical trend of 128%.

Source: currentmarketvaluation.com

Source: currentmarketvaluation.com

As for the Federal Reserve’s interest rate increases, and their effect on silver, the Fed will be guided by November’s inflation numbers which are due out Tuesday, right before the next FOMC meeting, on Dec. 14.

The pervasiveness of price pressures is problematic, and it will likely take two or more months of decreases for the Fed to consider pivoting from hawkish to dovish, meaning lowering interest rates and returning to its program of sovereign bond buying known as quantitative easing, or QE — that would be great for gold and silver.

The November CPI forecast, according to consensus estimates from FactSet, is for a slight lessening of the benchmark inflation indicator:

- CPI, year over year, to rise 7.3% versus 7.7% in October.

- CPI to rise 0.35% for the month versus 0.4% in October.

- Core CPI (excluding food and energy) to rise 0.3% for the month versus 0.3% in October.

- Core CPI, year over year, to rise 6.1% versus 6.3% in October.

Another key inflation measure, the Producer Price Index, rose 7.4% in November compared to 8.1% in October, the Bureau of Labor Statistics reported last Friday, via CNN. The PPI measures prices paid for goods and services by businesses before they reach consumers.

However, “Any meaningful relief for household budgets is still somewhere over the horizon,” Greg McBride, chief financial analyst at Bankrate, was quoted by CNBC following the release of the October inflation figures.

“The areas posting declines are for the most part either irregular or more discretionary in nature — airfare, used cars, and apparel,” he added.

Inflation

Song by Earnest Jackson & Sugar Daddy and the Gumbo Roux

Meaning all the stuff you buy on a daily basis is still going up, while the stuff you occasionally buy, and can do without for much longer periods, is going down. Households are increasingly having to discipline themselves into discretionary spending versus essentials.

In my opinion, precious metals’ positive reaction to lower inflation, in early November, backs up what we’ve been saying about commodities for quite some time. It’s a prelude to what will happen across the entire commodities spectrum when the dollar finally weakens after months of strength. (commodities tend to move higher when the dollar falls). The US dollar index hit a one-year high of 114.10 on Sept. 27, but it has since fallen back to 105.01, a drop of 8.6%.

Source: MarketWatch

Source: MarketWatch

Precious metals bounce is a taste of what’s to come

Commodities are the trade for riding out the Fed-caused recession

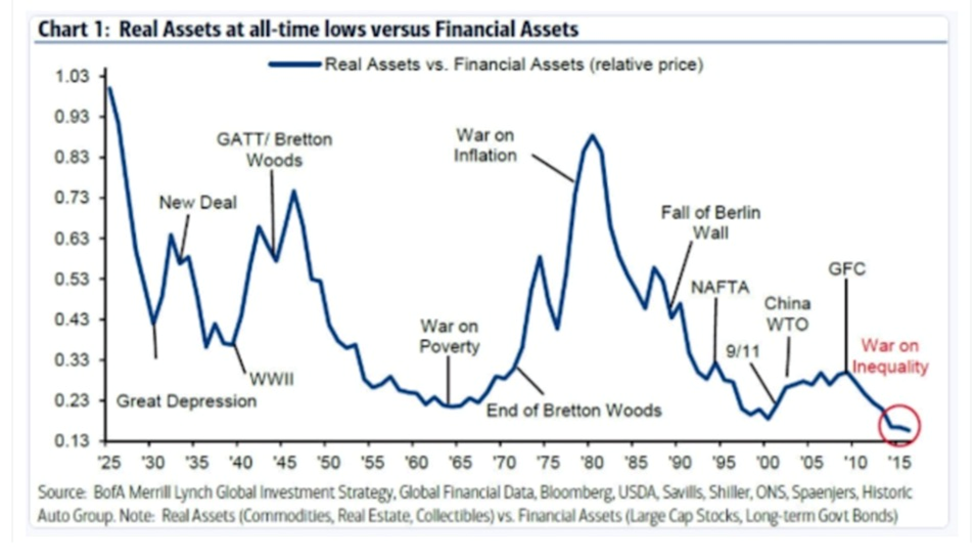

Our belief in silver is also a reflection of our faith in real assets versus financial assets.

Why real assets are better at protecting wealth than financial assets

Investopedia defines real assets as physical assets that have an intrinsic worth due to their substance and properties. They include commodities, natural resources, equipment and real estate. Real assets provide portfolio diversification as they often move in the opposite direction as financial assets, which include stocks, bonds, mutual funds, savings and cash.

Inflation, changes in currency values, and other macro-economic factors affect real assets less than financial assets, making them more stable, and good investments during periods of high inflation.

The chart below, via Harvest, graphs the price of real assts versus financial assets over time. We find that real assets explode in relative value during periods of inflation and war. This makes sense because more resources are needed, or commodities are scarce, relative to money.

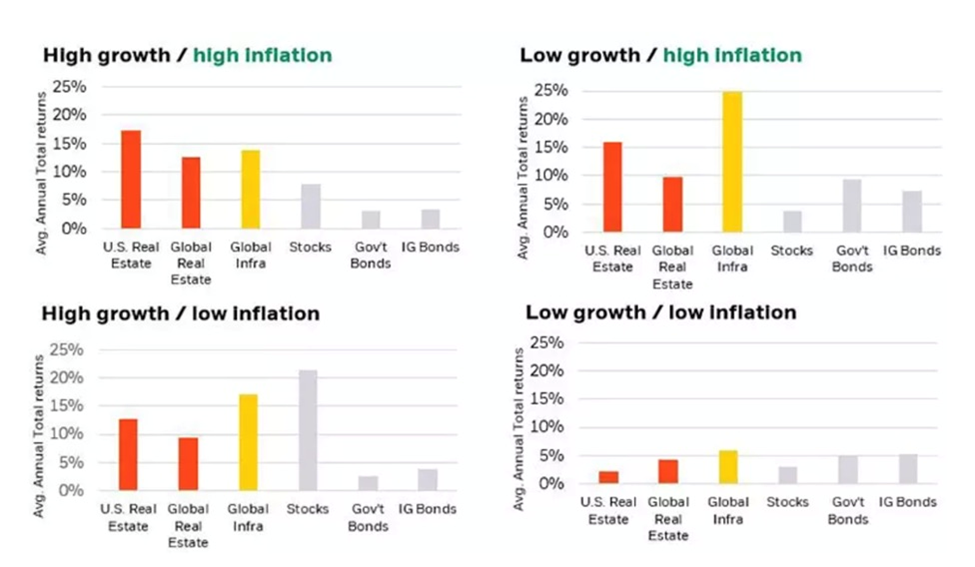

Real assets outperform traditional asset classes during high inflation environments.

Real assets outperform traditional asset classes during high inflation environments.

The chart below shows a wide dispersion between asset price inflation and real economy inflation. While real economy prices barely moved from 2009-18, asset prices exploded. Harvest states: The capital gains, dividends, or carry has favored these assets over investing in the real economy. Excess cash has used financial assets as a store of value. This is the collateral used for a levered economy.

Industrial demand

Industrial demand

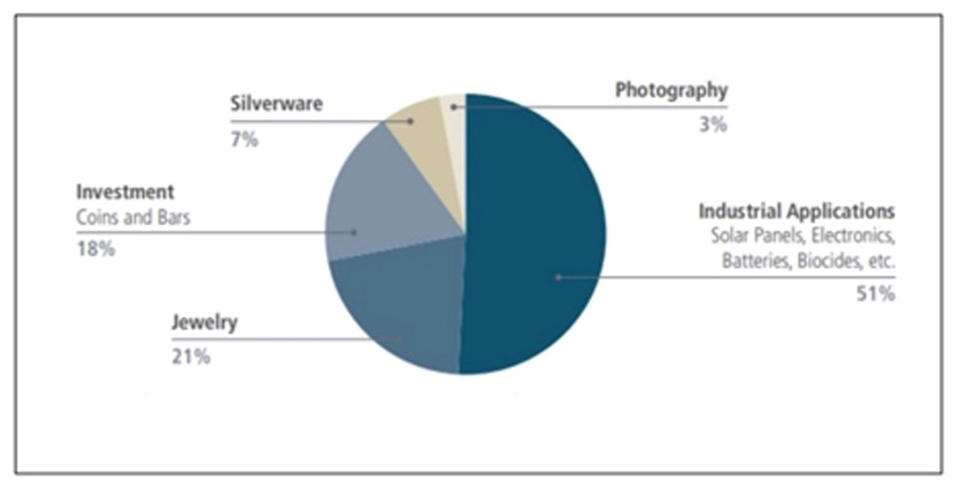

While silver is a monetary metal, much of its value is derived from industrial demand. It’s estimated around 60% of silver is utilized in industrial applications, like solar and electronics, leaving only 40% for investing.

Source: GFMS Definitive, Metals Focus, The Silver Institute, UBS

Source: GFMS Definitive, Metals Focus, The Silver Institute, UBS

Solar

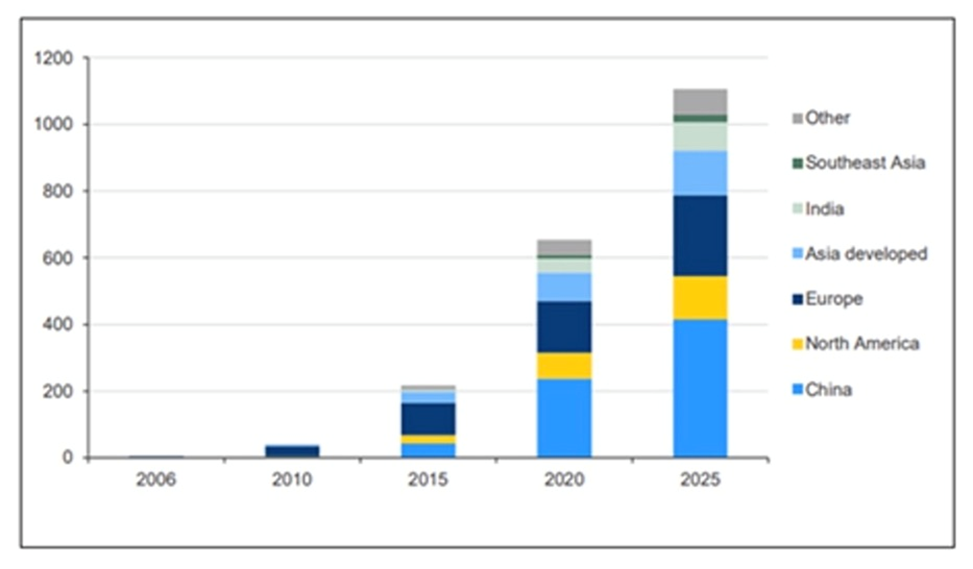

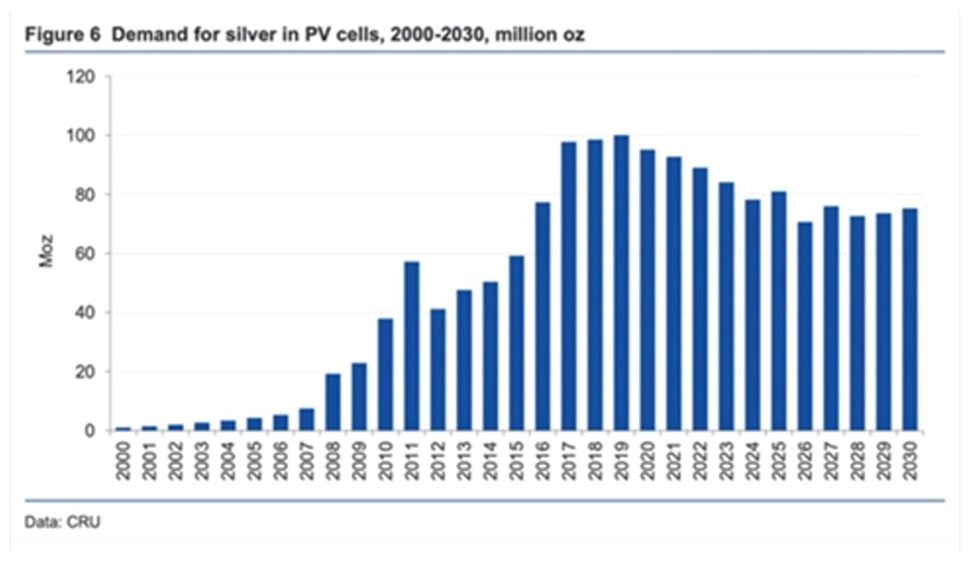

As the metal with the highest electrical and thermal conductivity, silver is ideally suited to solar panels. About 100 million ounces of silver are consumed per year for this purpose alone.

This figure is expected to rise in the coming years, with continued growth of electricity demand and renewable energy aspirations all pointing to rising solar power penetration.

Historical and forecast solar capacity by region, 2006-2025. Source: The Silver Institute & CRU Consulting

Historical and forecast solar capacity by region, 2006-2025. Source: The Silver Institute & CRU Consulting

One projection has annual silver consumption by the solar industry growing 85% to about 185 million ounces within a decade, according to a report by BMO Capital Markets.

5G

5G technology is set to become another big new driver of silver demand. Among the 5G components requiring silver, are semiconductor chips, cabling, microelectromechanical systems (MEMS), and Internet of things (IoT)-enabled devices.

The Silver Institute expects silver demanded by 5G to more than double, from its current ~7.5 million ounces, to around 16Moz by 2025 and as much as 23Moz by 2030, which would represent a 206% increase from current levels.

Automotive

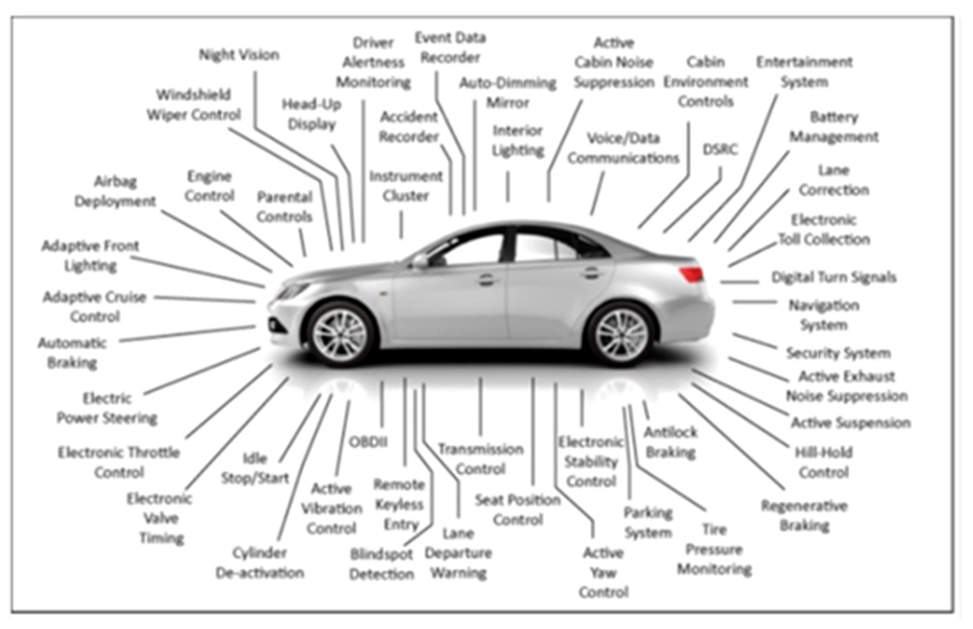

A third major industrial demand driver for silver is the automotive industry. Silver is also found in many car components throughout vehicles’ electronic systems, and despite not being used in batteries, its superior electrical properties make it hard to replace across a wide and growing range of automotive applications.

Automotive electrical and electronic components. Source: The Silver Institute

Automotive electrical and electronic components. Source: The Silver Institute

Battery electric vehicles contain up to twice as much silver as ICE-powered vehicles. A recent Silver Institute report says the auto sector’s demand for silver will rise to 88Moz in five years as the transition from traditional cars and trucks to EVs accelerates. Others estimate that by 2040, electric vehicles could demand nearly half of annual silver supply.

Brazing and soldering

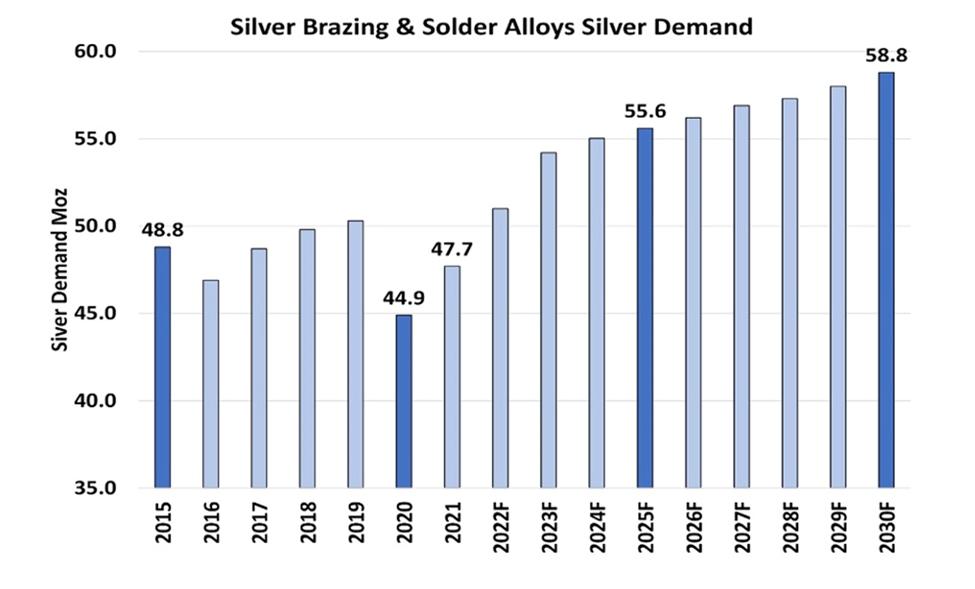

In 2021, brazing and soldering alloys used 47.7Moz of silver, representing 9.3% of the total industrial demand for silver that year. By 2030, the demand for silver used in brazing and soldering is forecast to reach 58.8Moz, a 23% over 2021, according to a Silver Institute report released in June, titled ‘Silver in Brazing and Solder Alloy Materials’.

Source: World Silver Survey and Precious Metals Commodity Management

Source: World Silver Survey and Precious Metals Commodity Management

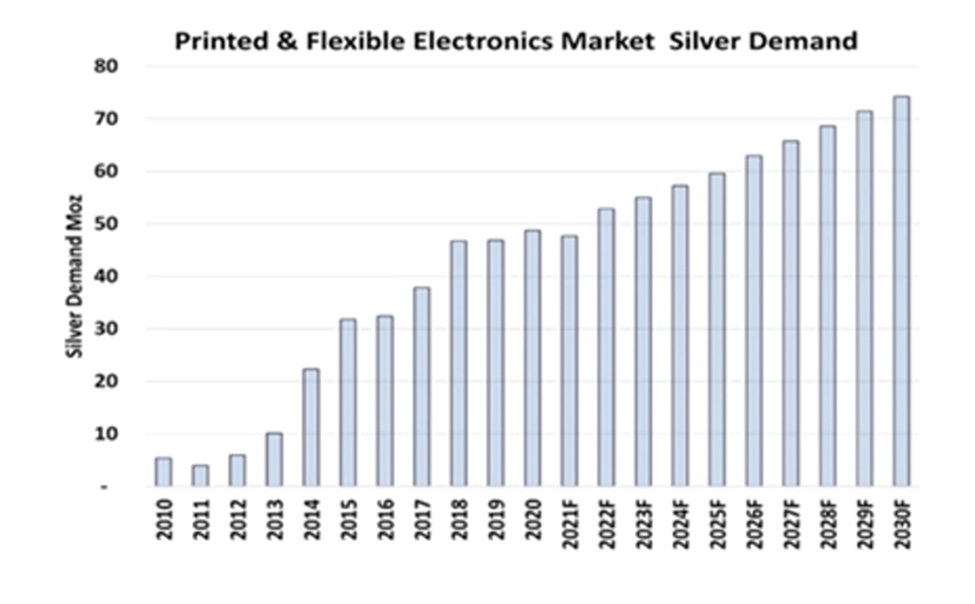

Electronics

Finally, silver demand for “printed and flexible electronics” is forecast to increase 54% over the next nine years, rising from 48Moz in 2021 to 74Moz in 2030, meaning a consumption of 615Moz during this time frame.

A Silver Institute news release describes them as “mainstays” in a variety of electronic products, including sensors that measure everything from temperature, pressure and motion, to moisture, relative humidity and carbon monoxide. They are also used in medical devices, mobile phones, appliance displays and consumer electronics.

Printed and flexible electronics market silver demand. Source: Precious Metals Commodity Management LLC

Printed and flexible electronics market silver demand. Source: Precious Metals Commodity Management LLC

Silver as critical metal

The “green economy” rejects dirty sources of energy and transportation, namely coal, oil, and natural gas. Instead, it relies on carbon-friendly modes of transport and energy production, including electric vehicles, renewable power, and energy storage, as well as mobile technology (5G) and rapid adoption of artificial intelligence (AI) technologies needing increased computing power.

Transportation makes up 29% of global emissions, so transitioning from gas-powered cars and trucks to plug-in vehicles, as well as high-speed rail, is an important part of the plan to wean ourselves off fossil fuels.

However, to accomplish all of the above will require a colossal boost in the production of mined materials, including silver, copper, zinc, nickel, lithium, graphite and palladium.

The move away from fossil-fuel-powered vehicles to EVs run on batteries is happening in almost every country. Governments are spending billions on EV charging infrastructure and subsidies to incentivize consumers to switch to hybrids and plug-in electric cars, vans and trucks. Large automakers like Volkswagen, Mercedes Benz, GM and Ford are coming out with new EV models, and are planning new EV manufacturing/ assembly plants in North America and Europe.

US battery and EV plants galore

On pace for record year

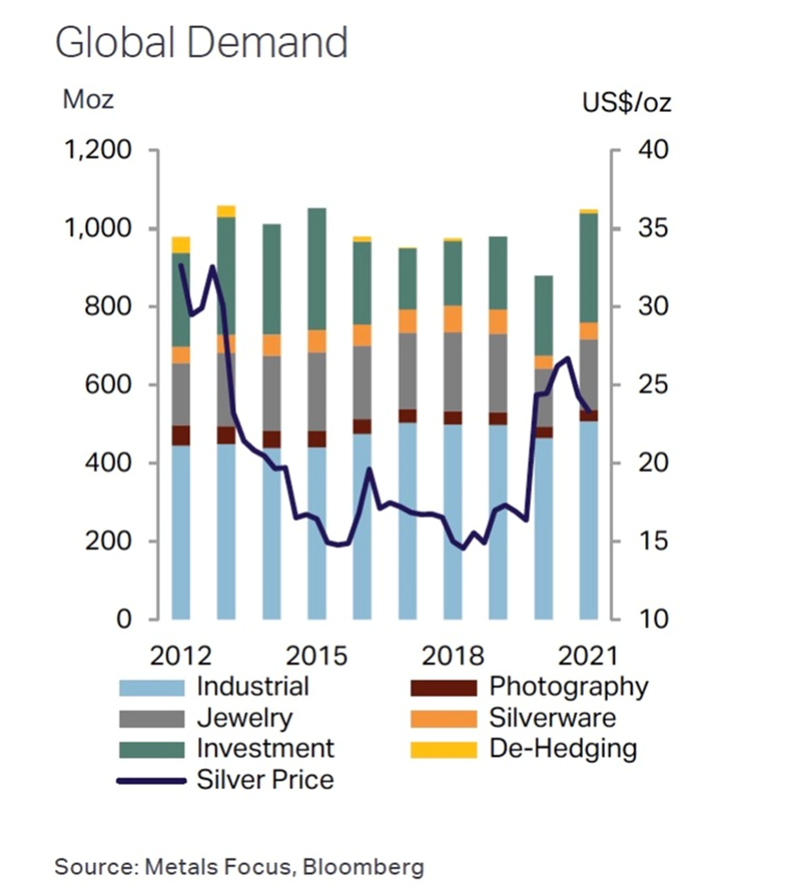

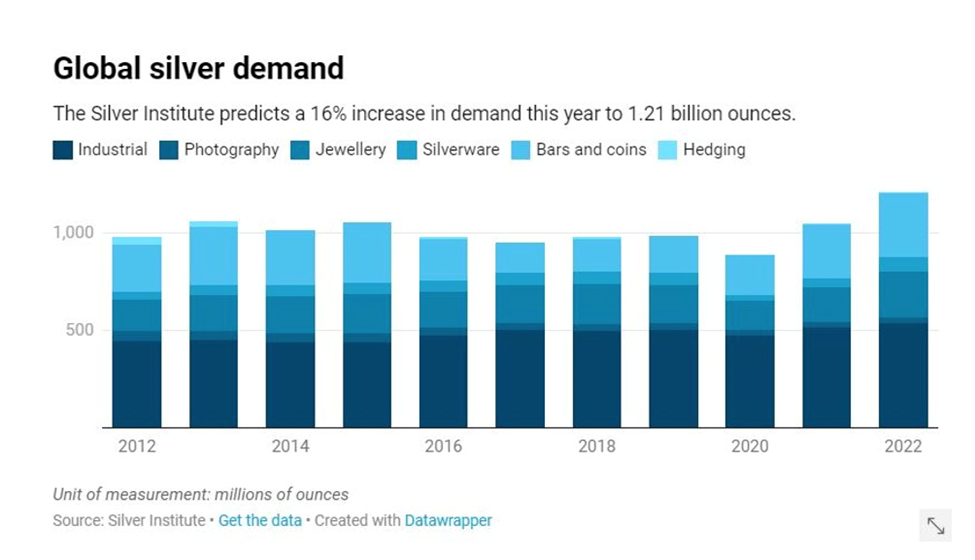

According to the Silver Institute’s 2022 Interim Silver Market Review, released on Nov. 17, global demand for silver this year is forecast to hit a record 1.21 billion ounces, a 16% increase from 2021 demand. New highs are predicted for physical investment, industrial demand, jewelry and silverware production.

While institutional demand for silver has faced headwinds, due to rising interest rates leading to a decrease in silver ETF holdings, this has been countered by a surge in physical investment, which is on pace to jump by 18% to 329Moz this year.

According to the Silver Institute, “Support has come from investor fears of high inflation, the Russia-Ukraine war, recessionary concerns, mistrust in government, and buying on price dips. The rise was boosted further by a (near-doubling) of Indian demand, a recovery from a slump last year, with investors often taking advantage of lower rupee prices.”

Source: World Silver Survey 2022

Source: World Silver Survey 2022

India buying

The Indian market is particularly strong for silver. Silver consumption there is forecast to surge by around 80% this year, Bloomberg said, as warehouse inventories are drawn down after two years of covid.

A recent article says that, while Indians bought low amounts of silver in 2020 and 2021, due to hits to supply chains and demand, this year silver sales are back on track:

Local purchases may surpass 8,000 tons in 2022 from about 4,500 tons last year, said Chirag Sheth, principal consultant at Metals Focus Ltd. That’s up from an April estimate of 5,900 tons.

Panelists at the LBMA gold conference in Lisbon agreed that physical demand for gold and silver remains exceptionally strong, particularly in Asia and the Middle East.

Record-low inventories

The amount of silver stored in vaults in London (London Bullion Market Association) and New York (Comex exchange) has fallen by about 370 million ounces, or 25% this year. (Reuters, Nov. 17, 2022)

Inventories of silver held in vaults across London dropped to a record low in October, according to data from the LBMA. Kitco News reported that Silver holdings dropped to 26,502 tonnes, down 2.2% from the previous month. The value of holdings stood at $16.3 billion, which is about 883,417 silver bars.

“This is the lowest amount of silver held in the vaults since reporting started in July 2016,” the LBMA said in its report this week [Nov. 7-11].

The drop in silver holdings is explained by the robust demand for the physical metal. “The decline reflected the ongoing strength of coin and bar demand, especially in the key U.S. and German markets,” said Philip Newman, the Managing Director at Metal Focus.

Bullion Star said an important contributor to this unprecedented demand for physical silver is India. The country’s silver imports for the first nine months of 2022 totaled 8,217 tonnes. When annualized, this amounts to nearly 11,000 tonnes, representing one-third of the world’s silver supply.

India’s massive silver demand cutting world’s warehouse stocks

Physical market tightness

According to one market analyst quoted by Kitco News, there is a significant disconnect in the silver market between investment demand in “paper” (silver ETFs) and physical bullion.

Peter Krauth, founder of the Silver Stock Investor newsletter and author of ‘The Great Silver Bull’, says the supply and demand imbalance is acutely felt among physical silver investors forced to pay record premiums for bullion because there isn’t enough supply.

A recent article by SB&C notes gold and silver prices are strongly influenced by the buying and selling of futures contracts. Unlike “paper” gold and silver, there is a limited quantity of physical metal:

As a result, it’s typical for the spot price of gold and silver to take a while to catch up with the realities of physical demand. It’s only a matter of time before that gap is reconciled…

The entire precious metals industry is struggling to keep up with the skyrocketing demand for physical gold and silver. This extraordinary rush towards physical metals has resulted in market wide supply shortages and delivery delays of some gold and silver coins, gold bars, and silver bars. The combination of fewer people looking to sell gold and silver and a growing number of buyers is squeezing the availability of physical precious metals…

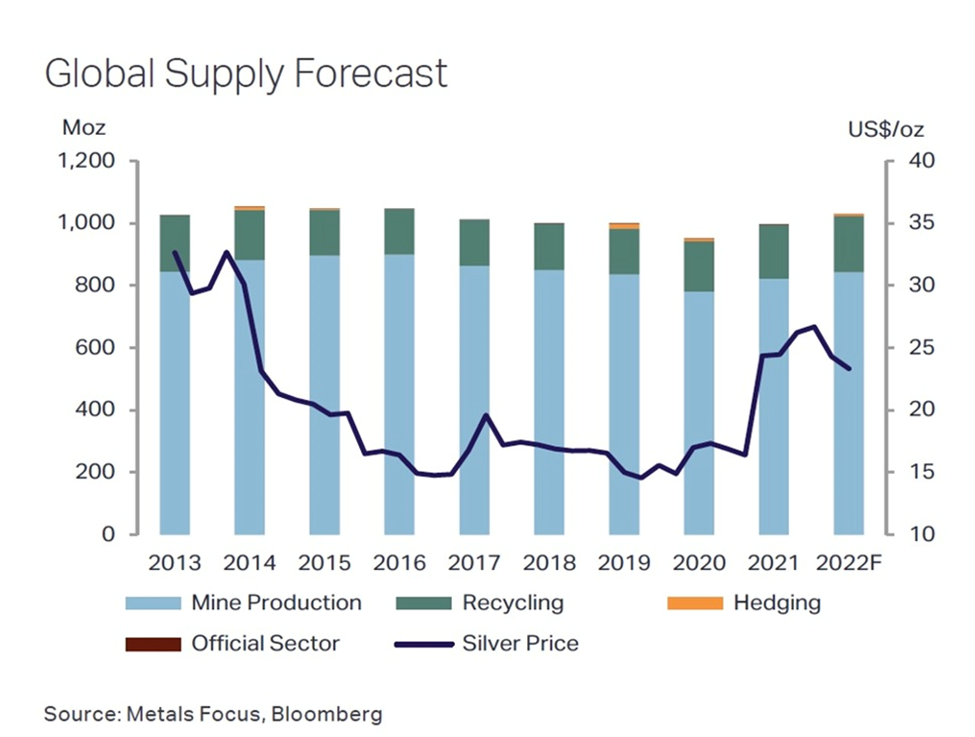

Record deficit forecast

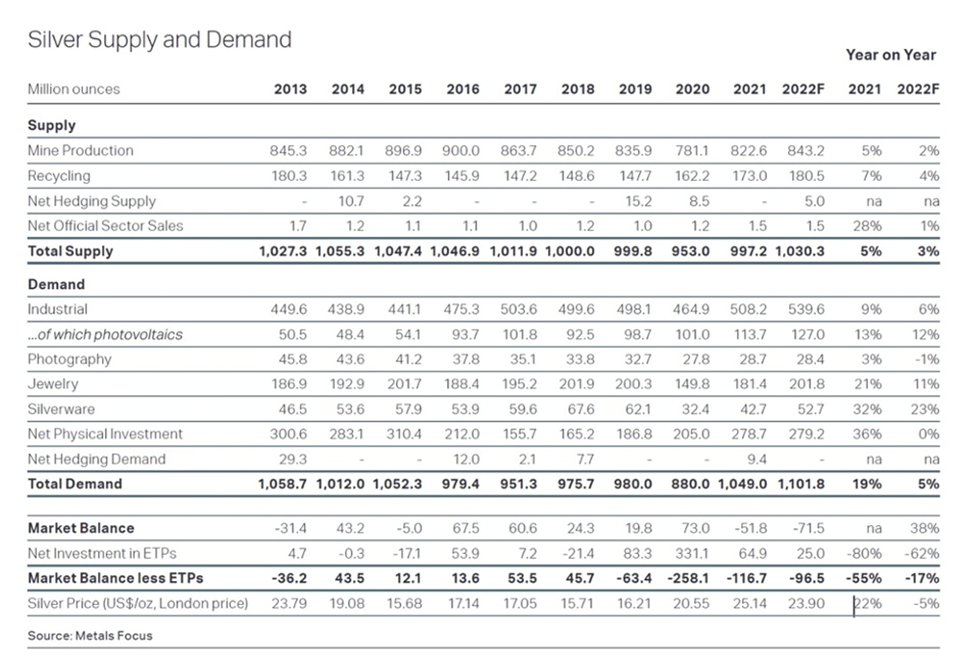

Total mined silver supply in 2021 was 25,587 tonnes, or 822.6 million ounces. The Silver Institute expects mine production in 2022 to increase by 2.5%, to 843.2Moz, with the biggest rise occurring in Mexico.

Source: World Silver Survey 2022

Source: World Silver Survey 2022

After shifting to a deficit in 2021 for the first time in six years, the silver market is expected to post a second, and record shortfall this year.

Source: World Silver Survey 2022

Source: World Silver Survey 2022

The 194-million-ounce deficit compares to 48Moz in 2021 and would be a multi-decade high, according to an article by Schiff Gold.

Peak silver

Like gold, we can study the supply-demand picture for silver to get a sense of whether we’ve reached peak mine supply.

At AOTH we differentiate between the total silver supply, which lumps in recycled silver with mined silver, versus mine supply on its own. (most recycled silver is industrial grade)

According to the 2022 World Silver Survey, in 2021 global mine production increased 5.3% yoy to 822.6 million ounces, or 25,587 tonnes. It was the biggest rise in production since 2013, largely due to economic recovery following a down year in 2020, when a lot of silver mines were disrupted due to the pandemic.

Helped by higher prices, silver recycling rose for a second year in a row, up 7% in 2021 to an 8-year high of 173Moz, or 5,382 tonnes.

Combined, therefore, we have total silver supply reaching 997.2Moz in 2021.

How about demand? According to the World Silver Survey, after a slump in 2020, global silver demand climbed by 19% last year to 1.05 billion ounces, surpassing pre-pandemic volumes and reaching its highest level since 2015.

(Remember: While most of the mined gold is still around, either cast as jewelry, or smelted into bullion and stored for investment purposes, the same cannot be said for silver. It’s estimated around 60% of silver is utilized in industrial applications, like solar panels and electronics, leaving only 40% for investing.)

All the demand categories saw gains, the largest being bar and coin purchases, followed by industrial demand. Physical investment (bars and coins) demand skyrocketed by 35% to 278.7Moz, the highest level since 2015’s record, as investors hoovered up the white metal in response to inflation uncertainty and negative real interest rates. Sales of silver bars and coins in India more than tripled.

2021 demand of 1.049 billion ounces outstripped supply of 997.2Moz, by 51.8Moz. But remember, recycling is included in the total supply. When we take recycling out, 173Moz, we get an even greater deficit of 224.8Moz. (1,049,000,000 minus 824,200,000 = 224,800,000)

This is significant, because it’s saying even though mined silver supply last year rebounded from 2020, to 822.2Moz, the highest since 2013, it was unable to meet total demand, industrial plus investment, of 1.05 billion ounces, which was the highest demand for silver since 2015. It fell short by 51.8Moz, and that was including recycling.

This is our definition of peak mined silver. Will the silver mining industry be able to produce, or discover, enough silver that it’s able to meet demand without having to recycle? If the numbers reflect that, peak mined silver would be debunked.

It didn’t happen in 2021, (or 2020) and according to the Silver Institute, it won’t happen in 2022 either.

Again, let’s look at the numbers.

The Silver Institute expects silver output in 2022 to exceed last year’s total by 2.5%, year on year, hitting 843.2Moz, or 26,226t. But again, this includes recycling; it’s set to increase for a third straight year, with a 4% gain forecast, or 180,500,000 oz.

Taking 180,500,000 oz of forecasted recycling out of the equation, we have mined supply of 662,700,000 oz, against the Silver Institute’s 2022 demand forecast of 1,101,800,000 oz (1.101Boz), leaving another forecasted deficit, and one that is nearly twice as larger as 2021’s, when recycling is excluded, of 439.1Moz.

The case for peak gold, silver and copper

Silver undervalued

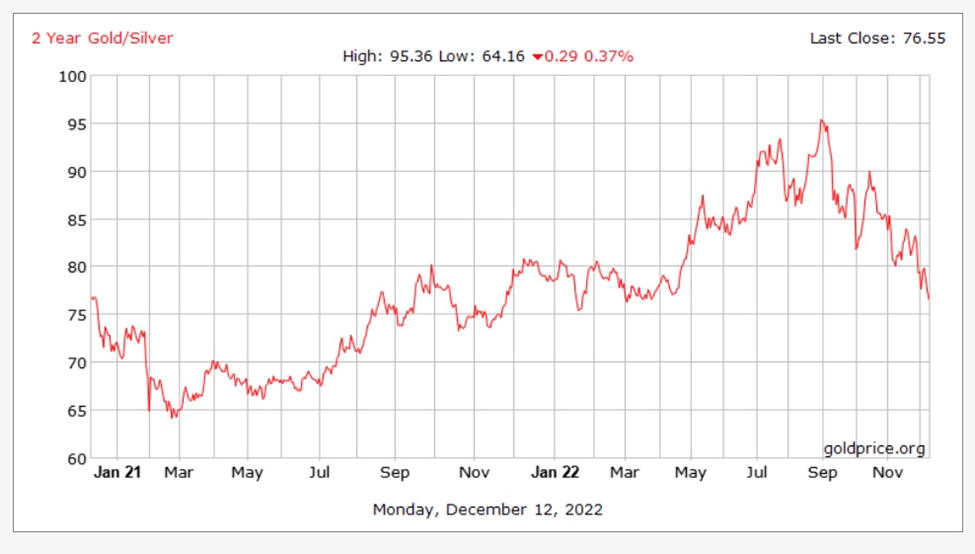

We use the gold-silver ratio to find out how silver prices compare to gold. The ratio is the amount of silver one can buy with an ounce of gold. Simply divide the current gold price by the price of silver.

The higher the number, the more undervalued is silver or, to put it another way, the farther gold is pulling away from silver, valued in dollars per ounce.

When gold is over-valued compared to silver, investors take advantage of the arbitrage opportunity, by selling some of their gold holdings to buy silver. The opposite occurs when silver is over-valued compared to gold. In that situation, they sell silver to buy gold.

As the chart below shows, the gold-silver ratio over the past two years has been all over the map, reaching a low of 64 in March, 2021, and hitting a high of 95 in September, 2022.

For the past month the ratio fluctuated between 84.0 and 76.5. This is still out of whack from the historical ratio of 40 to 50, meaning that silver is on sale.

2-year gold-silver ratio. Source: Goldprice.org

2-year gold-silver ratio. Source: Goldprice.org

Historically, the ratio has always returned to the mean.

See the chart below, and linked commentary by Schiffgold.com, showing that Historically, when the spread gets this wide, silver doesn’t just outperform gold, it goes on a massive run in a short period of time. Since January 2000, this has happened four times. As this chart shows, the snapback is swift and strong.

Source: Schiffgold.com

Source: Schiffgold.com

Conclusion

Now is a good time to be stocking up on relatively cheap gold and silver, although for me, the better investment is in junior resource companies, who are exploring for and developing the world’s future mines.

A recent Silver Institute report says electric vehicles contain up to twice as much silver as gas-powered vehicles. Charging points and charging stations are also expected to demand a lot more silver.

It estimates the auto sector’s demand for silver will rise to 88Moz in five years as the transition from traditional cars and trucks to EVs accelerates. Others estimate that by 2040, electric vehicles could demand nearly half of annual silver supply.

According to Adamas Intelligence’s State of Charge report, EV registrations rose by 42% in the first half of 2022, compared to the same period last year. This amounts to 6.23 million units, up from 4.4 million in H1, 2021. For round numbers, let’s just say that electrification is growing at 2 million units a year. How much silver will be needed for that level of demand? And remember, the mining industry still needs to mine enough silver for monetary and all the other industrial uses.

The soaring demand for silver, matched against the coming supply crunch — remember we are already at peak silver and this year’s forecasted deficit is four times higher than last year’s — all but guarantees the silver price is moving higher.

Richard (Rick) Mills

aheadoftheherd.com

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable, but which has not been independently verified.

AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness.

Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice.

AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments.

Our publications are not a recommendation to buy or sell a security – no information posted on this site is to be considered investment advice or a recommendation to do anything involving finance or money aside from performing your own due diligence and consulting with your personal registered broker/financial advisor.

AOTH/Richard Mills recommends that before investing in any securities, you consult with a professional financial planner or advisor, and that you should conduct a complete and independent investigation before investing in any security after prudent consideration of all pertinent risks. Ahead of the Herd is not a registered broker, dealer, analyst, or advisor. We hold no investment licenses and may not sell, offer to sell, or offer to buy any security.

About the author

Richard (Rick) Mills

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether or not you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.