The gold and silver prices are rallying, perhaps seemingly paradoxically so, given how this comes on the heels of Donald Trump saying that the Iran war will be over ‘very soon.’

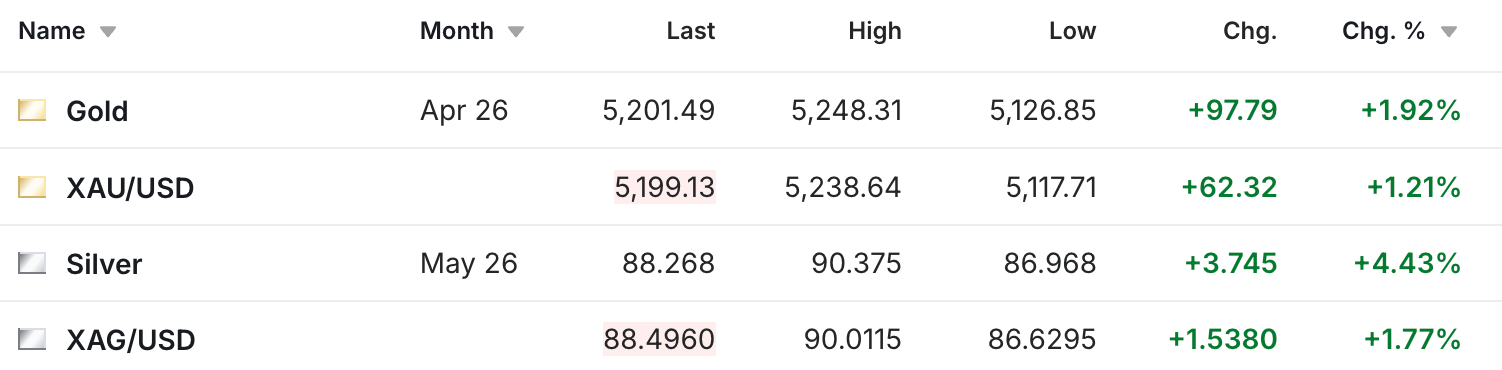

Yet the gold futures are having a big day and are currently up $98 to $5,201, while the silver futures are up $3.75 to $88.26.

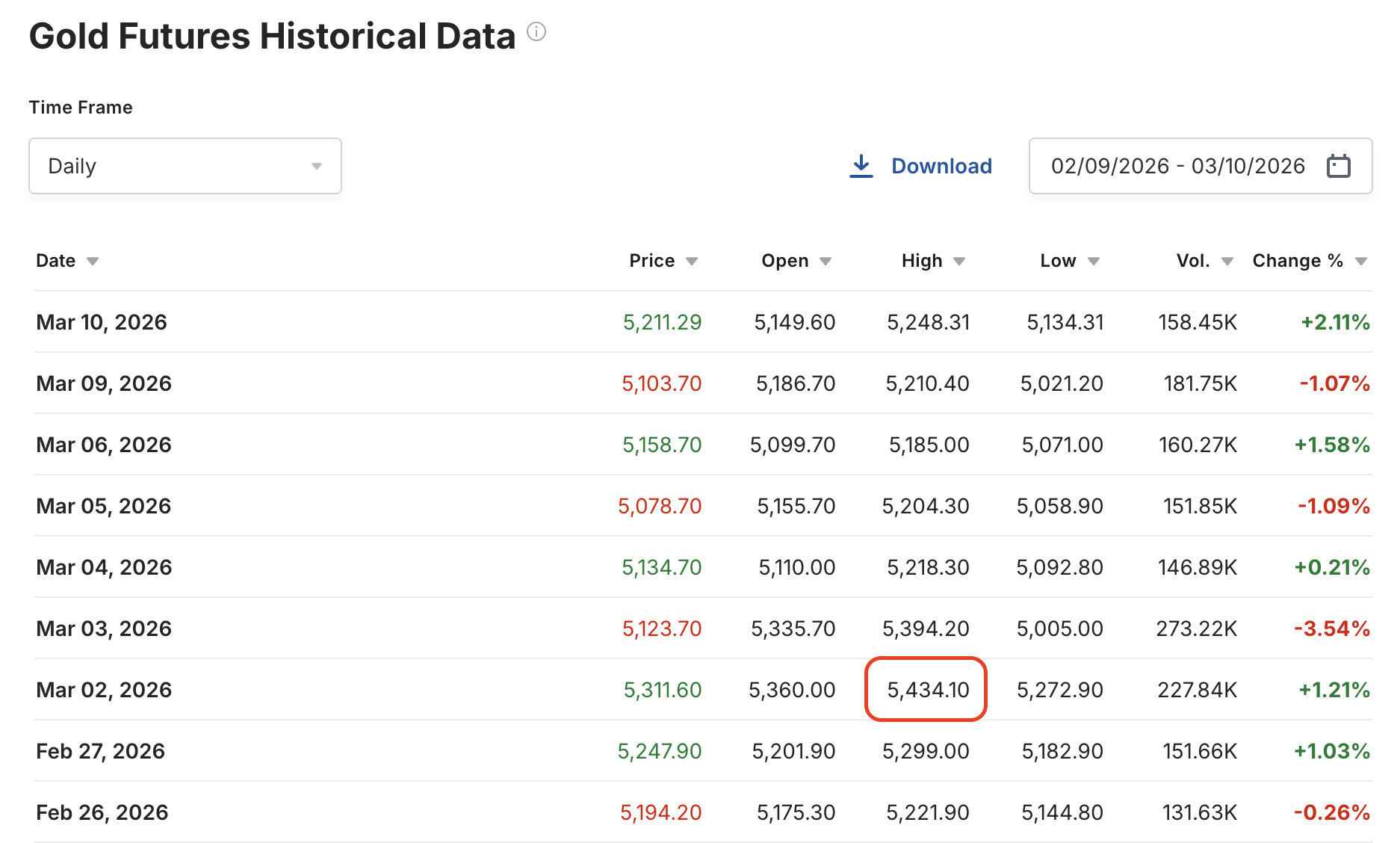

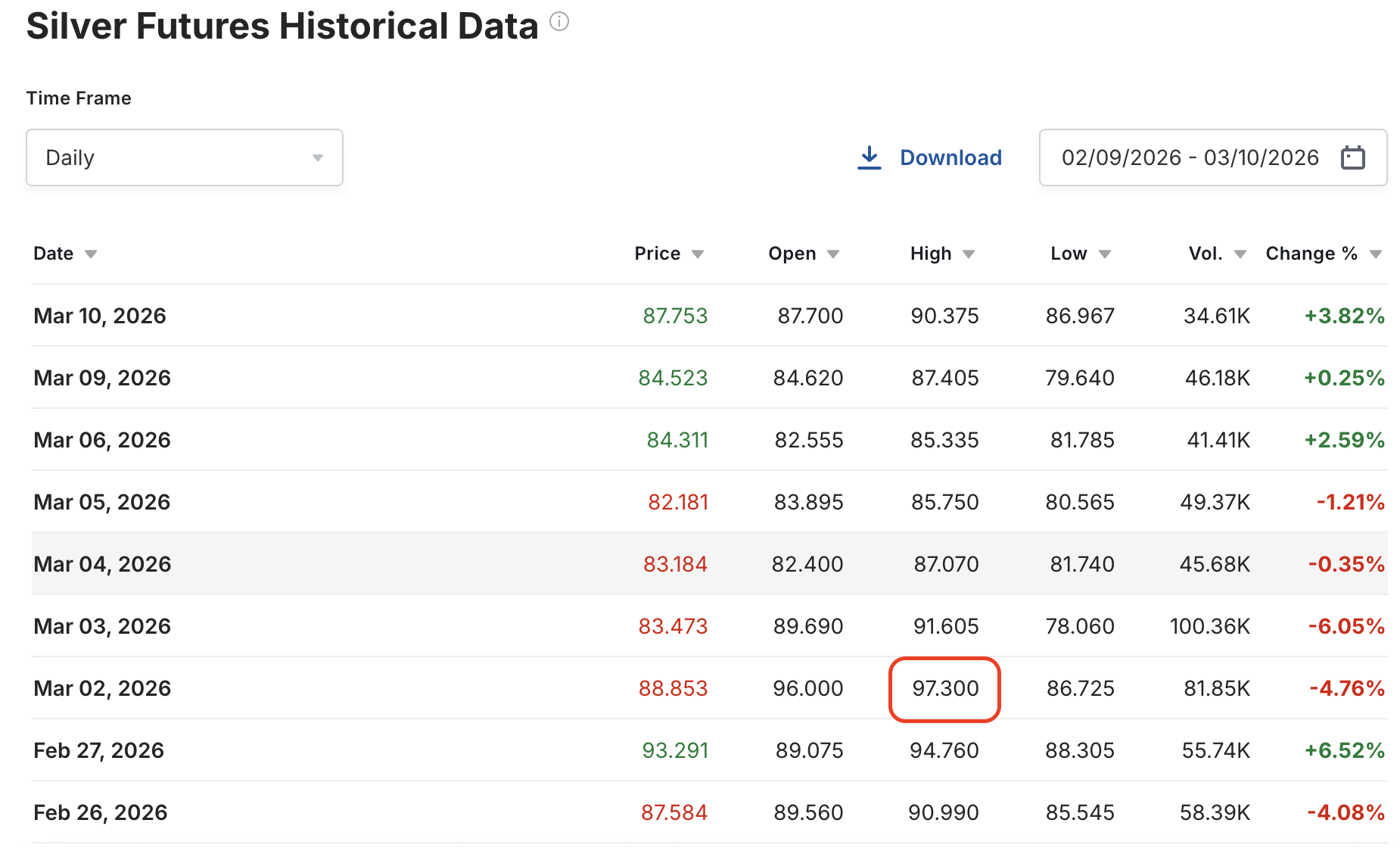

However, many gold and silver investors have been frustrated over the past week and a half, as after the gold and silver prices surged higher on the Sunday night open on March 2nd after the war in Iran began, the prices have actually fallen as things have escalated.

The gold futures are currently $230 lower than their March 2 peak, while the silver futures are $9 lower since then.

So why haven’t the metals rallied?

First, despite the belief that precious metals should rise when war breaks out, which isn’t necessarily entirely untrue, there’s also not a guaranteed relationship that the metals have to rise when there’s a new conflict. And perhaps even more significantly, we’ve seen time and time again that gold and silver just simply don’t always trade that way. Whether it makes intuitive sense or not.

A recent example can be seen in how the gold price spiked at the very onset of Russia’s war with Ukraine back in March of 2022, but then got clobbered in the following months as the Fed was raising interest rates 75 basis points at a time back then.

That was also when the central banks started their record-setting gold buying spree. But if there’s anything that gold and silver investors have learned in the past decade or two, it’s that if there’s ever been an asset that doesn’t always respond linearly on a consistent basis in the way that the conventional wisdom might assume, the precious metals are it.

Now you can debate why that is, and obviously, there’s been plenty said about different shenanigans that go on in the futures markets. But at least in terms of what is and likely will be, the correlation between war events and gold and silver spiking is simply just far less than 100%.

Additionally, I think this is also the perfect example of how the efficient market hypothesis they teach in business school sounds lovely, but really couldn’t be further from the truth in reality.

It’s based on the premise that information flows evenly to all market participants at the same time, which, of course, is ludicrous when you think about it or say it out loud. Because there are infinite things happening in the world, and it’s impossible for any one person to cover even a remote fraction of the entirety of them.

Plus, you could have two people watch the same conversation or event and come away with completely different perceptions, so the idea that everyone’s interpreting the information in the same way and at the exact same time is just not how it works in reality. And what we’ve seen over the past week serves as the perfect example of that.

Consider what Time Magazine is reporting regarding how back when this began on February 28th, Trump had suggested that it might only take two or three days, and yet, after the first day, he had already reportedly upped the timeline to four weeks.

Trump has offered conflicting timelines on how long the Iran conflict will take to resolve. Early on Feb. 28, after the initial strikes, he told Axios that he had the choice to “go long” or “end it in two to three days.” The day after the first salvo, Trump told the Daily Mail that the campaign in Iran would take about four weeks.

So how does this get incorporated into the gold and silver pricing?

Not easily.

Because the market’s still figuring out what’s actually happening, similar to the tariff situation last year. No one knows by the day what’s actually going to happen next, how extended it will be, or what the true ultimate implications are going to look like.

No one knows what the economic cost will be, how extensive the damage to all involved will be, and I’m not sure even if the entire world did know those answers, that there would be a consensus on how that ultimately impacts the gold and silver pricing. And that’s part of the tricky thing about the way the metals, and also the other commodities, are priced. There’s supply and demand, and then there’s also the degree of anxiety or nervousness of the futures traders, which is a somewhat arbitrary variable that can change frequently.

My suspicion is that this ultimately ends up playing out in similar fashion to what we saw with the confirmation of silver as a critical mineral. I remember people were disappointed that it was down the day that silver was finally confirmed, but then fast forward a few months later after governments had started forming strategic mineral stockpiles, and silver soared to over $120 by the time it was all said and done.

Similarly, if a month from now the war has escalated even further, it looks like there’s no end in sight, and people are starting to get killed in larger numbers, we may well see a much different environment in the financial markets. Also, perhaps this is somewhat of a sad statement regarding the current state of affairs in the world, but I also wonder if after four years of the Russia-Ukraine war, people have simply become somewhat emotionally tapped out and just don’t even know how to respond any more.

What is the price of gold supposed to be if a new war begins? How much is silver supposed to go up or down if one war starts or ends? These aren’t really events where you can just discount the cash flows and come up with a precise numerical answer. And I think the choppy trading you’ve seen in the gold and silver markets in the past week, that also included a shockingly weak labor report, and a massive spike in the oil price, is reflective of how volatile the markets have been, and how difficult it is to really know what tomorrow or next week will look like.

That’s also why I continue to recommend to gold and silver investors that after a big price move or event, even if you’re deciding what to do in the shorter term, start by thinking about what you think is likely to happen to the price of gold and silver over the next ten years, given everything that’s happening in the world right now, and just start there. Reflect on the things you’re thinking about and what you see happening, and I find that taking the step back has the added side benefit of somehow also making the more near-term decisions easier to see in context.

Hopefully, this doesn’t sound insensitive to what’s going on in Iran, but I believe the gold price is going to do what the gold price is ultimately going to do, regardless of whether a war with Iran lasts another week or another year. Some of these events have been set into motion long ago, and while the mileposts can alter the timeline of how long it takes to get there, certain dynamics like the U.S. balance sheet have long since passed the point of no return. We’ve already seen that reflected in the gold and silver prices as they are, and as time progresses, I believe it will continue to be reflected. Even if that hasn’t happened over the past week.

So hopefully that gives you a few ideas to consider if you’ve been trying to reconcile why there hasn’t been more of an upward reaction since the war began. I’m not saying it’s necessarily just that simple, and obviously, there are usually multiple factors at play. But I do think that captures the essence of what we’ve just seen, and hopefully it helps to put everything in context.

Lastly, there have been some rather bizarre and disconcerting developments regarding what’s been going on with Venezuela’s gold and their mining sector following the incursion to remove former president Nicolas Maduro. And I discussed that on our YouTube channel this afternoon, which I thought you might enjoy taking a look at.

But ultimately, it was another positive day for the gold and silver markets, and I’ll check back in with you on whatever else happens.

About the author