A modified * excerpt from the February 22nd edition of Notes From the Rabbit Hole, NFTRH 903:

The Drive to the Mid-Terms

We know that the Trump administration is going to do all it can to pump the economy, or more precisely, the stock market, into the mid-term elections. It was no coincidence that AG Bondi was babbling about the Dow over 50,000 at a hearing that had NOTHING to do with the stock market. I believe Scott Bessent is hard at work trying to engineer policy of both government and Fed in order to see to a nice economic backdrop into Q4.

Politicians. These may be absurdly different ones. But politicians are politicians, and they do politician things, like attempt to hoodwink the public through fiscal maneuvering and hence, manipulate every election cycle, regardless of political party.

They’ve got the Fed at least partially playing ball. They’ve got pro-business policies kicking in, and this view is well in line with our primary macro view, which is an inflationary operation after the current disinflationary Goldilocks or something more painfully deflationary passes. The operation is expected to be perceived as beneficial at first, into year-end. Later? Not beneficial. Potentially quite destructive.

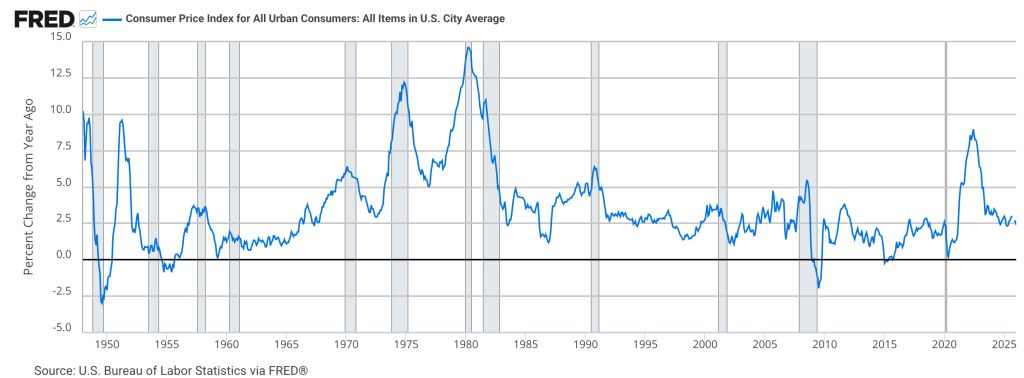

To this point, the condition, at least from the vantage point of the public, has been a steady “disinflation” from the spike levels, post-2020. What this says is that inflation is still increasing, but at a much slower rate of 2.5% compared to the hysterical 8%+ of 2022. This could be as good as it gets before the negative effects of the next inflation problem created by the Fed and government become apparent to the public.

So, sure, the next inflation problem will probably start out being perceived as beneficial, as most of them do. But my expectation is that much like after the 2020 bailout, it will not be too long before the benefits fade away and inflationary angst erupts far and wide.

I expect a virulent Stagflation to be the end result of a government and Fed trying to layer inflation on top of inflation, as opposed to an inflationary bailout of a deflationary liquidation like those that occurred occasionally during the decades-long “old macro”, before the 2022 bond market rebellion:

This is what I believe they are brewing as the Fed resumes QE behind the scenes, but is expected to hold rates steady until the June meeting, during and after which the rate cut cycle is expected to resume in earnest (ref. CME projections).

Hmm, what significant event happens in between the April and June meetings? Lemme think. Ah, yes, the hand-picked Mr. Warsh takes over the Fed in May. Pretty handy, eh?

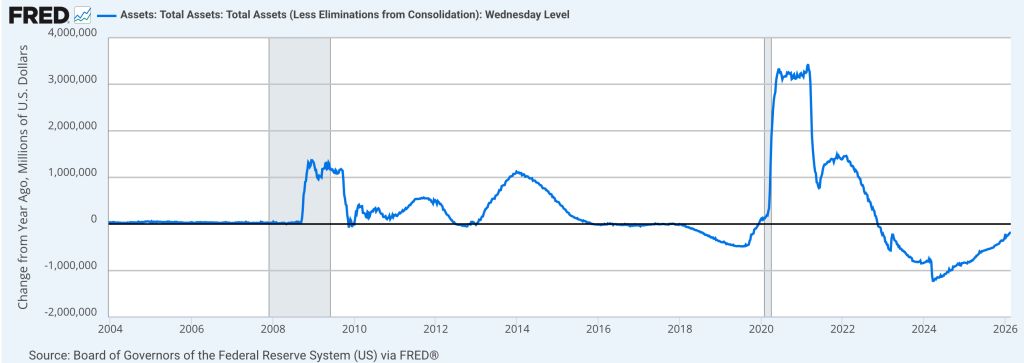

A literal look at the Fed’s balance sheet shows a gentle bottoming and a hint of Quantitative Easing after a long trend of Quantitative Tightening. That, along with their stated intent to buy Treasury bonds (but not MBS), is enough to know that this is a future inflation creator, even as it has not really kicked in yet. You can see that the change from a year ago is now trending up. QT is over, and QE (of some kind) is ahead.

Midterms, here we come.

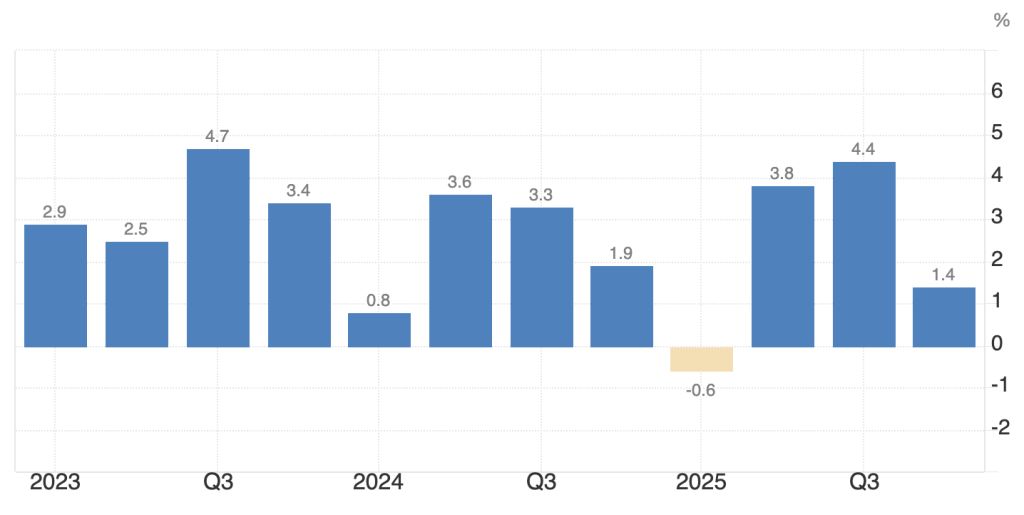

Last week, GDP came in surprisingly low (1.4% vs. 2.5% forecast). Just the excuse those itching to inflate might need. It is likely due mainly to the government shutdown in Q4. Regardless, this is a lagging indicator.

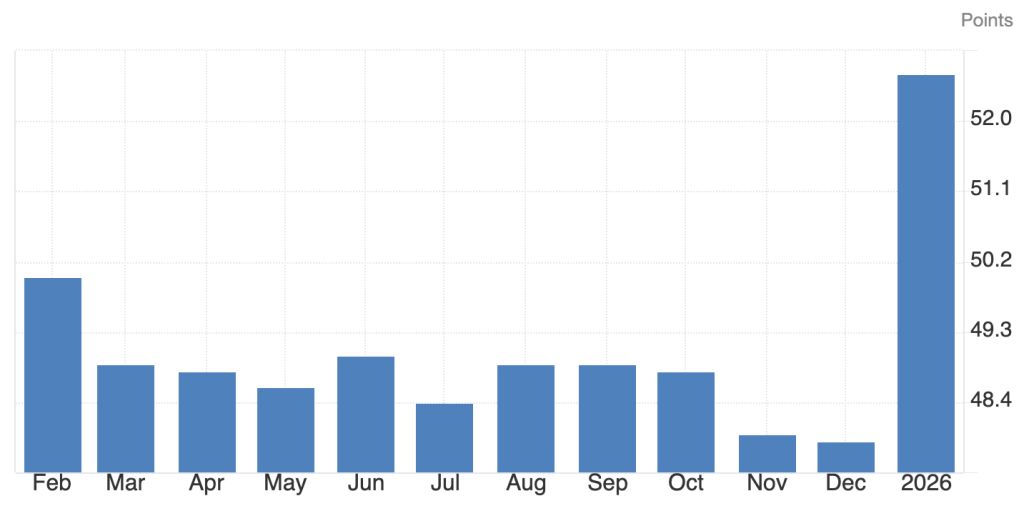

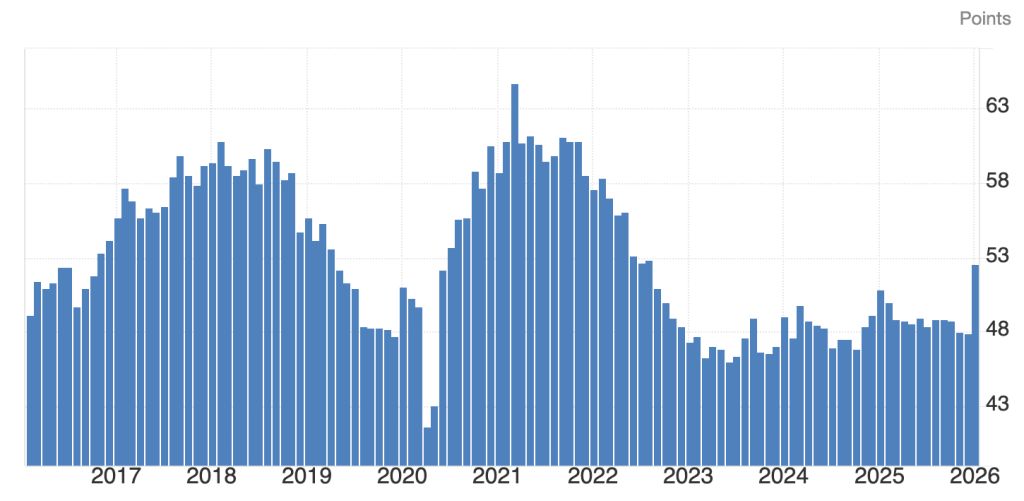

But not so fast. Manufacturing, a leading economic component, boomed in January. As if out of nowhere.

Broad PMI hit 52.6%, the first growth reading since 50.9% in January, 2025, and before that 51% in September 2022.

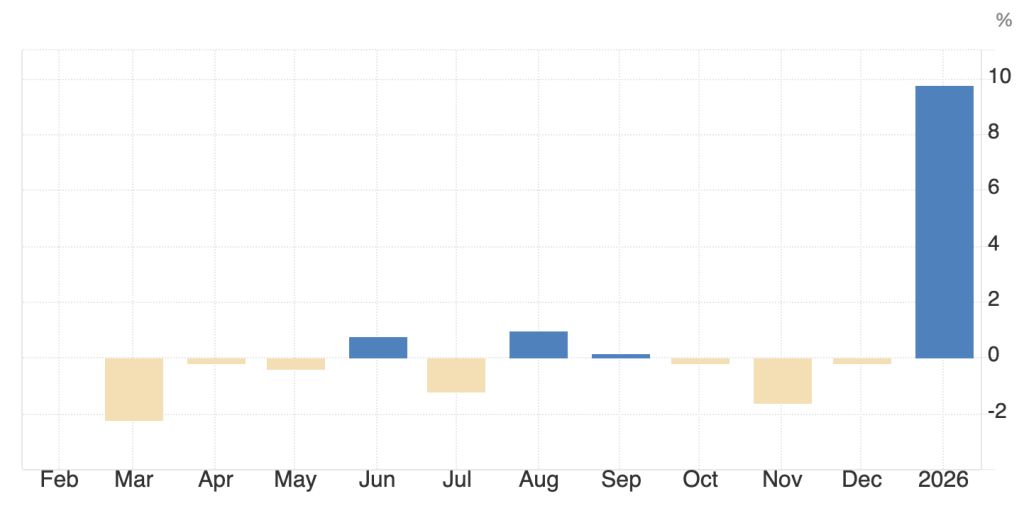

The percent change exploded out of nowhere.

As for the PMI’s more important components, they were as follows:

- New Orders: 57.1%

- Employment: 48.1% (contracting)

- Inventories: 47.6% (contracting, a positive for future orders)

- Customer Inventories: 38.7% (contracting, a positive for future orders)

- Prices: 59% (so much for waning effects of inflation)

There is no denying the fact that US manufacturing had a boom reading in January. Could this have been a one-shot wonder? Sure, with all the unnatural economic inputs mainlined into the system over the last year, anything is possible.

But if we are going to play it straight (I am), we are going to allow for the theory that regardless of any market correction that may manifest in the near-term, things are setting up nicely for the economy and stock markets to get gunned into the elections and year-end. ISM may be the first shot across that bow.

NFTRH 903 then proceeded with a mainly strategy-intensive theme (sector rotations, timing, etc.) as 2026 is going to be materially different than 2025 where effective investment strategy is concerned.

* For the purposes of wider publication.

About the author