Silver’s dazzling parabolic surge this summer was overwhelmingly driven by enormous silver-ETF-share buying. Led by momentum-chasing millennial traders, unprecedentedly-huge amounts of stock-market capital deluged into the dominant SLV iShares Silver Trust silver ETF. But since silver’s resulting lofty peak, silver-ETF-share selling has been mounting. An acceleration is a major downside risk for silver prices.

Silver has certainly lived up to its wildly-volatile reputation this year. Ahead of mid-March’s brutal stock panic driven by governments’ heavy-handed national lockdowns to slow the spread of COVID-19, silver was inconspicuously grinding higher. In late February before pandemic fears flared in the US, silver was running $18.62. But it was then soon sucked into the epic maelstrom of fear as stock markets cratered.

Outsized stock-market fear infecting silver is normal. Herd psychology has an unusually-strong influence on silver price levels. Traders rush to buy silver when they grow bullish and excited, catapulting its price far higher. But when they get bearish or worried for any reason, they drop silver like a bad habit forcing steep plunges. The global silver market is tiny, further amplifying the price impacts of material capital flows.

Over the next several weeks or so into mid-March, silver collapsed 35.8% to $11.96. That deep 10.9-year secular low utterly annihilated all bullish sentiment. And 4/9ths of that plummeting was compressed into just two trading days where silver collapsed 18.9%! That proved a near-crash, crowding the formal crash threshold of a 20%+ loss in two trading days or less. That stock panic totally rebooted silver psychology.

It left silver radically oversold, trading at just 0.704x its 200-day moving average. Anything under 0.90x is extremely oversold and unsustainable. Sub-$12 silver prices were fundamentally ridiculous as well. In Q1’20 hosting that rare stock panic, the world’s major silver miners reported average all-in sustaining costs of $13.45 per ounce. No commodity’s price can languish well below the world production cost for long.

Silver indeed started violently V-bouncing out of those crazy stock-panic lows. Its initial gains were big and fast, with silver blasting 19.4% higher in the first four trading days out of that deep nadir! After that silver’s post-stock-panic upleg throttled back into something much more sustainable. By early June silver had surged 52.8% over 2.5 months, hitting $18.27. Fully 95% of its stock-panic losses had been regained.

Silver stalled from there, consolidating high over the next five weeks into early July. It wasn’t overbought at all at that initial post-panic interim high, trading at just 1.081x its 200dma. Historically, extreme levels of silver overboughtness warning of imminent selloffs start at 1.25x. Silver’s strong post-panic gains to that point were fueled by heavy differential SLV-share buying. Understanding how silver ETFs work is essential.

The mission of silver exchange-traded funds is to track silver price action. But the supply and demand for ETF shares is independent from silver’s own, leading to constant imbalances that must be addressed. Excess ETF-share supply or demand relative to silver’s own must be directly shunted into the underlying global physical silver market. If that didn’t happen, silver-ETF-share prices would soon decouple from silver’s.

The American iShares Silver Trust overwhelmingly dominates the silver-ETF space. It pioneered silver ETFs, launching way back in April 2006. Its lead has grown insurmountable since. The world authority on silver’s fundamentals is the venerable Silver Institute. Once a year it publishes comprehensive data on global silver supply and demand in World Silver Survey reports. The most recent was released in April.

That covered 2019, where SLV exited holding 362.6m ounces of physical silver bullion in trust on behalf of its shareholders. The WSS declared that gave SLV a commanding 49.8% share of all the silver bullion held by all the world’s physically-backed silver ETFs! SLV has gobbled up half of the global silver-ETF market. The next-biggest competitor out of Switzerland only ranked at 11.4%. SLV is truly in a league of its own.

Silver-ETF-share buying and selling really moves silver prices at the margin because it is the most-volatile source of silver demand by far. Most silver usage is relatively stable year after year, as evident in the Silver Institute’s annual data. But silver-ETF silver demand is radically volatile. It swung from -22.3m ounces in 2018 to +81.7m in 2019, up to 8.2% of overall demand. The WSS forecast for 2020 is +120m or 12.5%.

And that pre-pandemic outlook for exploding silver-ETF-share demand is wildly understated in this crazy new world we find ourselves in. By mid-August, SLV’s holdings had skyrocketed to an astounding new all-time-record high of 581.0m ounces. That made for +218.4m ounces in silver-ETF demand from SLV alone year-to-date! That exploding SLV-share demand was off-the-charts unprecedented, utterly incredible.

SLV’s underlying physical-silver-bullion holdings are reported daily, and their trends reveal whether stock-market capital is flowing into or out of silver. When American stock traders buy SLV shares faster than silver itself is being bought, SLV-share prices threaten to decouple from silver to the upside. That would cause SLV to fail its silver-tracking mission. So SLV’s managers must step in to offset that excess demand.

In near-real-time, they sell enough new SLV shares to absorb the differential SLV-share demand beyond silver’s own. Then they immediately plow the money raised from those share sales into physical silver. So when SLV’s holdings are rising, stock-market capital is flowing into silver. That happened in spades since the stock panic, an unprecedented frantic rush to gain silver portfolio exposure via those SLV shares.

When American stock traders sell SLV shares faster than silver itself is being sold, SLV’s share price will disconnect from silver’s to the downside. SLV’s managers must avert this by buying back enough SLV shares to sop up that excess supply. They raise the capital necessary to do these buybacks by selling some of SLV’s physical silver bullion. So falling SLV holdings show stock-market capital flowing back out of silver.

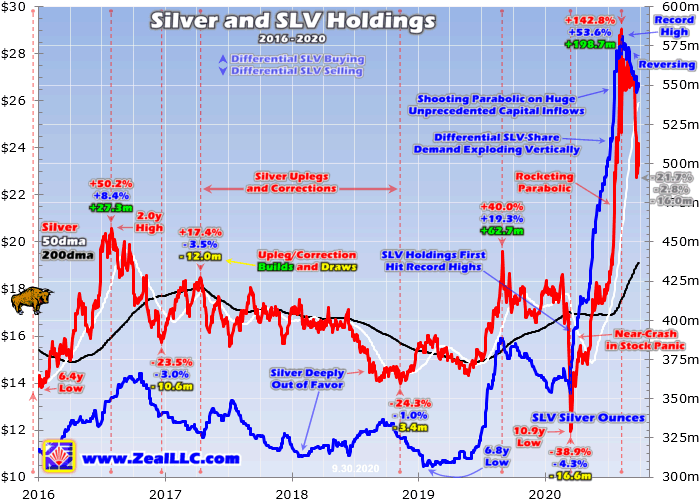

This chart superimposes SLV’s holdings over silver’s price action during its secular bull, which started to run in mid-December 2015. Since silver is so exceedingly volatile, its bull and bear markets are often rendered off gold’s which is its dominant primary driver. Silver has never witnessed differential-ETF-share buying of the magnitude seen since the stock panic! The vertical explosion in SLV’s holdings is epic.

Interestingly silver’s plummeting into the stock panic didn’t spawn much differential SLV-share selling. Inside that 3-week span where silver cratered 35.8% into mid-March, SLV’s holdings merely fell 4.4% or 16.3m ounces at worst. Shrewd bargain-hunting traders started flooding into SLV again a couple trading days before silver’s nadir, so over its selloff’s exact span SLV’s holdings actually rose 2.0% or 7.4m ounces.

The heavy SLV buying accelerated dramatically from there. In late March just six trading days after silver bottomed, SLV’s holdings surged to their first new all-time-record high of 391.9m ounces. By the time SLV’s holdings crested in mid-August, 45 new record closes had been seen! At that initial silver interim high of $18.27 in early June, SLV’s holdings had blasted up 25.8% or 95.8m ounces during silver’s 52.8% rally.

Differential ETF-share buying certainly wasn’t the only financial-market source of silver demand as this metal mean reverted dramatically higher. Speculators were also flooding into silver futures, which sport big leverage really amplifying their silver-price impact. But American stock traders rushing into SLV shares were the primary source of capital chasing silver’s big gains to ride its strong momentum higher.

Interestingly when silver spent those five weeks consolidating high between early June to early July, the heavy differential SLV-share demand persisted. During that span where silver just ground sideways at best, SLV’s holdings surged another 8.0% or 37.2m ounces! The trading day before silver barely eked out its next new post-panic high, SLV’s holdings hit a momentous milestone first breaking above 500m ounces.

In March, April, May, and June SLV enjoyed major holdings builds of 27.5m, 17.6m, 50.4m, and 34.7m ounces. But that paled in comparison to July’s astounding monster 70.1m-ounce build! That is what started to force silver parabolic. Silver’s strong post-panic upleg had started to attract in an unusual new group of traders, millennials. They started aggressively piling into SLV shares to chase silver’s big momentum.

Millennials generally haven’t been big stock traders in the past. Being younger, as a group they mostly haven’t been able to generate the considerable surplus capital necessary to trade stock markets. But in one of the more-significant unforeseeable market consequences of this crazy pandemic, the millennials used it to start rushing into the markets en masse. This is so unbelievable you couldn’t make it up.

The majority of millennials mostly had service jobs, which of course were the most dramatically affected by governments’ draconian national lockdowns. So many millions of young people were laid off, suddenly finding themselves at home with nothing to do. But being unemployed during this pandemic proved quite lucrative for lower earners, thanks to the federal government’s gargantuan pandemic stimulus payments.

Millennials who had long struggled to save were suddenly making out like bandits. They got that one-time $1200 helicopter money. But the big score came in Paycheck Protection Program payments and the federal unemployment bonuses. For the first 2.5 months of being laid off, millennials who were employed by companies taking out PPP loans were paid in full. They were making normal wages with far-lower expenses.

And the millennials who filed for unemployment benefits sooner or later during the lockdowns received not only their state payments, but an extra $600 per week in bonuses Congress provided with the CARES Act. $2400 per month of free money is not trivial, annualizing to an extra $31,200 per year! Stuck in their apartments and super-bored, millennials watched the stock markets rocket higher out of March’s panic.

With big surpluses of cash and time for the first time in their lives, they decided they wanted to chase the blistering stock-market gains. So they literally transferred tens of billions, likely even hundreds, of their pandemic stimulus dollars to stock-trading accounts! The millennials themselves confirmed this through countless surveys, Internet postings, and anecdotal reporting. They started trading stocks for their first time.

Their brokerage of choice was one few older traders had yet heard of, the phone app Robinhood. This company pioneered commission-free stock trading, which was really appealing to usually-penny-pinching millennials. While Robinhood is private and doesn’t disclose its total users often, it has revealed that its userbase utterly skyrocketed this year. Millennials by the millions opened up and funded Robinhood accounts.

For years Robinhood published data on how many of its users owned specific stocks, including SLV. Up until mid-March’s stock panic, there was little interest in this dominant silver ETF. Millennials crave high-tech things like electric cars, device makers, and crypto currencies. Silver is pretty old-school and boring for them. Still from the stock panic into late June, Robinhood users owning SLV climbed from 7.7k to 14.1k.

Now 14k millennials trading SLV, with accounts averaging a few-thousand dollars each, is nothing. That wouldn’t move the needle even in the tiny silver market. But the thing that made Robinhooders’ collective trading market-moving was the way this brokerage makes money. Instead of charging commissions, it instead sells its users’ collective real-time order-flow data to high-frequency-trading firms and hedge funds.

Their computers instantly trade milliseconds ahead of the Robinhooders, front running the millennials’ herd buying and selling. The HFTs and hedgies were deploying orders of magnitude more capital than the Robinhooders had, so the millennials’ stock trades were being greatly amplified in real-time! They were the tail wagging the vastly-larger hedge-fund dog, effectively directing capital flows vastly beyond their own.

Robinhood’s user-positioning data was also seen as a great proxy for how millennials as a whole were trading across all brokerages. And they started warming to silver in early July, increasingly attracted to its strong upside price action. Gold surged back over $1800 in the first half of July, which helped catapult silver up 6.9% month-to-date by mid-July. The Robinhooders owning SLV were growing, hitting 15.0k at that point.

But silver really started captivating millennials on July 20th and 21st, when it surged up to first challenge and then smash through the psychologically-heavy $20 level. From that point on, Robinhooders owning SLV shares rocketed vertically. And orders of magnitude more fund capital followed, front running their trades. By August 10th when silver’s parabolic surge peaked at $29.04, 35.5k Robinhooders owned SLV shares.

So in essentially several weeks, millennial participation in the silver market skyrocketed 137% higher! That catapulted SLV’s holdings from 516.1m ounces on July 15th to 581.0m less than a month later. This chart above reveals how silver shooting parabolic was directly driven by the vertical explosion in SLV’s holdings. Millennials trading pandemic-stimulus money with hedge funds mirroring was the dominant driver.

By silver’s early-August peak, it had skyrocketed 142.8% higher in just 4.8 months! Over 60% of those massive upleg gains occurred in its final month alone, when Robinhooders flooded into SLV. During that silver-upleg span, SLV’s holdings soared a staggering 53.6% or 198.7m ounces! That magnitude of SLV-share demand is wildly unprecedented. Silver and silver ETFs had never before witnessed anything close.

Parabolic surges are never sustainable for long, as the capital firepower available for near-term buying soon exhausts itself. And indeed within days of silver’s parabolic peak, SLV’s holdings topped out at that incredible new all-time-record high of 581.0m ounces. Both silver and SLV’s holdings have fallen since, with silver’s abrupt loss of momentum increasingly driving SLV-share selling. This is a serious risk for silver.

After blasting stratospheric to hit 1.659x its 200-day moving average in early August, silver needed to see a major correction to rebalance away the extreme euphoria and extraordinarily-overbought technicals. That got off to a violent start, with silver nearly crashing again by plummeting 15.2% in the first trading day alone after its August peak! But silver quickly bounced, and stayed above that $24.64 close until late September.

During that subsequent high-consolidation period between correction lows, silver averaged $26.93. But SLV’s holdings have fallen rather sharply, almost symmetrically with their euphoric build into silver’s peak. By late September, SLV’s holdings had already fallen 6.2% or 35.9m ounces at worst. The big question now is whether SLV faces considerably-more differential selling, whether American stock traders will flee silver.

Unfortunately Robinhood actually ceased releasing its users’ collective positioning data within days of silver’s early-August peak. Robinhood was increasingly getting bad press, with that data cited to show that millennials were speculating recklessly with exceedingly-risky bets. They were doing ridiculously-foolish trades as a herd, piling in to chase upside momentum regardless of how terrible stocks happened to look.

Without that Robinhood data, we can’t know if millennials have largely unwound their big SLV bets or if they are mostly still in. I suspect the former, as these young traders quickly lose interest once momentum flags and some other shiny stock crops up. But regardless of who still owns SLV shares, this dominant silver-ETF’s holdings remain far above pre-parabolic norms. That suggests the risks of selling remain high.

Silver speculation is largely driven by gold’s fortunes, and gold itself faces big near-term downside risks as I’ve detailed in recent essays. Like silver, gold’s own summer surge was also largely fueled by huge differential gold-ETF-share buying. But that went missing in action after gold peaked, just like silver-ETF-share buying. So gold too has a massive overhang of potential gold-ETF-share selling that could hammer it lower.

Also like silver, gold consolidated high after early August’s lofty peak. That left it extremely overbought by its own secular bull’s standards, like silver. Gold is also in its biggest seasonal selloff between its large autumn and winter rallies. That normally drags silver lower too. With gold’s high consolidation just rolling over into a full-blown correction, silver will follow and amplify gold’s losses like usual. So caution is in order.

Before this silver bull’s next upleg can start marching higher, silver needs to see a healthy rebalancing selloff to bleed away euphoric sentiment and extremely-overbought technicals. And with SLV’s holdings so darned high, differential SLV-share selling will certainly exacerbate any significant silver selloff. With silver-ETF selling mounting, this necessary process is already underway. That could push silver much lower.

After rocketing parabolically, silver tends to correct hard back down to or even through its 200dma. As the black line on this chart shows, that is a heck of a long way lower from here. This week silver’s key 200dma baseline is still way down at $19.13! To re-converge would require a 34.1% correction, making for lots more pain. But that would lead to an excellent mid-bull opportunity to buy back in relatively low.

All bull markets naturally flow then ebb, taking two steps forward before retreating one step back. Their price action gradually meanders around uptrends. This normal upleg-correction pattern keeps sentiment balanced, extending bull markets’ longevity. And it is a huge boon for traders, greatly expanding bulls’ potential gains. Look to aggressively buy silver and its miners’ stocks as this silver correction runs its course.

At Zeal we started aggressively buying and recommending fundamentally-superior gold and silver miners in our weekly and monthly subscription newsletters back in mid-March right after the stock-panic lows. We layered into dozens of new positions before gold stocks grew too overbought, which were later stopped out at huge realized gains running as high as +199%! Our subscribers multiplied their wealth within months.

To profitably trade high-potential gold and silver stocks, you need to stay informed about what’s driving gold. Our popular newsletters are a great way, easy to read and affordable. They draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. Subscribe today and take advantage of our 20%-off sale! Corrections are the time to do your gold-stock and silver-stock homework, preparing to redeploy as they pass.

The bottom line is silver-ETF selling is mounting. Since silver’s parabolic surge driven by massive capital inflows from differential SLV-share buying peaked, this dominant silver ETF’s holdings have been falling on balance. That reveals American stock traders are exiting silver, selling SLV shares faster than silver is being sold. And with SLV’s holdings remaining spectacularly high, they could have much more yet to do.

This potential-silver-ETF-selling overhang is a big downside risk for silver. With silver’s high consolidation failing into a correction, downside momentum will accelerate. That will scare many SLV shareholders into dumping their positions, exacerbating silver’s selloff. This vicious circle of selling could cascade until silver’s sentiment and technicals are rebalanced. And that’s probably a long way down from current prices.

Adam Hamilton, CPA

October 2, 2020

Copyright 2000 - 2020 Zeal LLC (www.ZealLLC.com)

About the author