$KOR.TO, $CORVF, $EDV.TO, $EDVMF, $SMF.TO, $SEMFF, $EQX, $FSM, $AG, $FNV, $SOLG.TO, $SLGGF, $GORO, $GCM.TO, $JAG.TO, $JAGGF, $TPRFF, $GBR.V, $GTBAF, $KNT.V, $KNTNF, $OR, $PGM.V, $LRTNF, $ROXG.TO, $ROGFF, $SAND, $SSRM, $TGZ.TO, $TGCDF, $TXG.TO, $SVM $USAS, $AGI, $GPL, $PAAS, $CDE, $NEM, $VITFF, $VGCX.TO

Mexico has declared mining can resume early (May 18th), 12-days early relative to the date initially stated. This includes countless mining operations by the likes of America’s Gold and Silver, Torex Gold, Equinox Gold, Endeavour Silver, First Majestic Silver, Fortuna Silver, Great Panther, Alamos Gold, Newmont, Pan-American, Fresnillo, Coeur, among many others. This is a good sign as far fewer countries continue to mandate the continued suspension of mining activities.

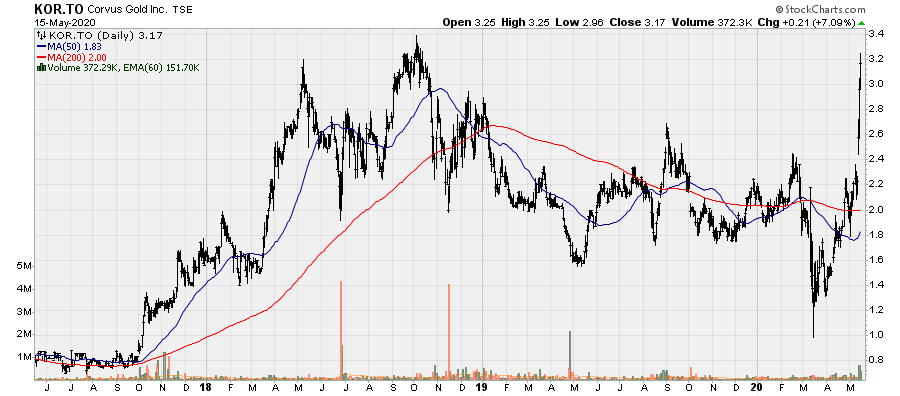

Corvus Gold: Continues to grow and expand its principal asset, the Motherlode deposit, this time making a new, large discovery below the Mother Lode deposit, highlighted by 125.5m @ 2.6 g/t Au [including 14.8m @ 8.9 g/t] and 38.2m @ 2.0 g/t [including 5.7m @ 2.6 g/t and 28m @ 2.1 g/t]. The potential of this discovery could be greater in size than the existing Mother Lode deposit. Additional drilling is needed.

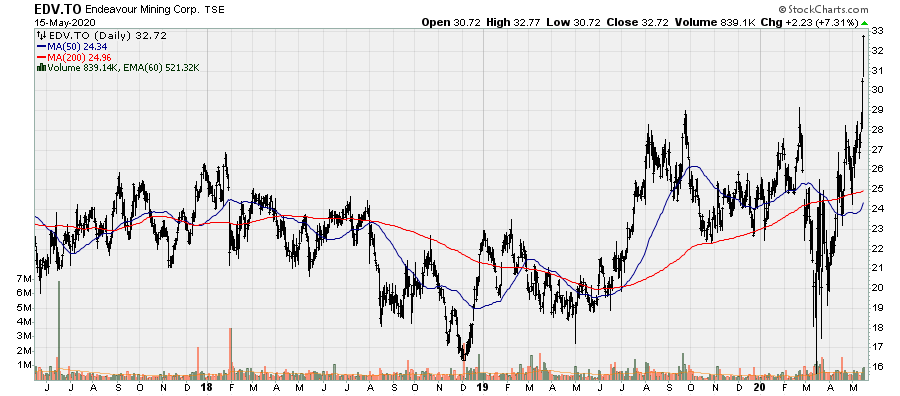

Endeavour Mining: The company had a strong start to the year with production of 172k oz. Au at AISC of $899/oz. Production increased 42% relative to Q1 2019, largely driven by the start of the Ity CIL operation, though AISC increased marginally. The company reported record operating cash flow of $126m in Q1, a significant increase over the comparable period in 2019. The company continues to deleverage its balance sheet, reducing net debt by $55m in the quarter to $473m (a $187m reduction over the past 3-quarters) as the heavy capital investment has come to an end. Current Net Debt to EBITDA if 1.06x at end of quarter, which will fall further upon completion of the SEMAFO acquisition but would continue to fall rapidly even in the absence of the cash provided by SEMAFO. The company spent $17m during the quarter on exploration or 40% of the full year budget. Endeavour has created a lot of shareholder value through the drill bit, something that will continue.

It is also worth mentioning SEMAFO quarterly performance and the deal between Endeavour and SEMAFO is expected to close this quarter, but nothing is guaranteed. The company generated $60m in operating cash flow during the quarter despite a 4-week suspension at the Boungou Mine. Gold production totaled 81.9k oz. Au in the first quarter. Full 2ktpd rates were achieved at Siou underground during the quarter. AISC during the quarter was $888/oz. The lower gold production relative to Q1 2019 (102k oz. Au) and higher costs are primarily attributable to 4-week suspension at the Boungou mine.

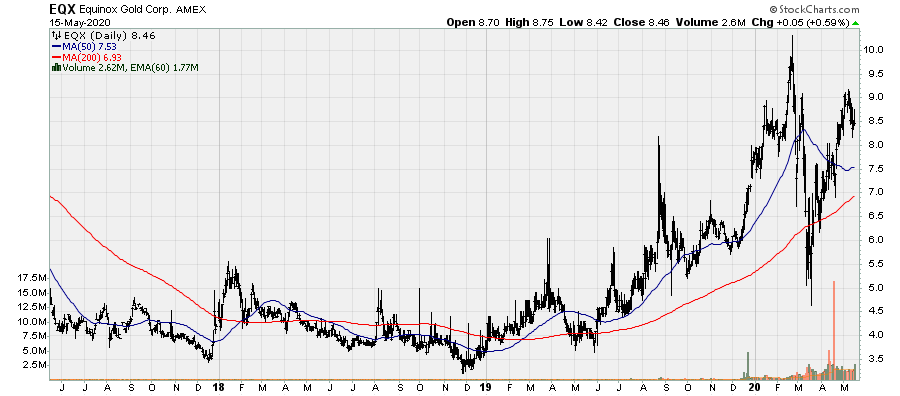

Equinox Gold: Provided an updated mineral reserve and resource estimate at Aurizona and Mesquite. Aurizona exploration success offset 2019 depletion while M&I resource (exclusive of reserves) increased 22% to 844k oz., the latter primarily as result of maiden resource estimate at Tatajuba (+112k oz. Au). Exploration will pick up at Aurizona over the next couple of years and we should see a material increase in total resources. At Mesquite, a newly identified mineralized material within dumps form historical operations accounted for greater than 60% of gold production in 2019. There is immediate additional exploration upside at Mesquite from over 40 million tons of potentially mineralized oxide dump material and new in-pit and near-pit targets. While Mesquite only has a 3.5-year mine life based on reserves, it is one of those operations which will never have a 10-year mine life, rather it should continually stay between 2-5yrs. Equinox acquired the asset a year and half ago and at that time, it has the same remaining mine life. But even if the mine became fully depleted, there are several years of residual leaching. Towards the end of the year, a significant production growth spurt will commence as its Castle Mountain Phase I (+45k oz.), followed by a 60-100% increase in output at Los Filos (320-400k oz.), a restart of operations at Santa Luz (+100k oz.), completion of Castle Mountain Phase II (+200k oz.), and the Aurizona underground (+65K --->?).

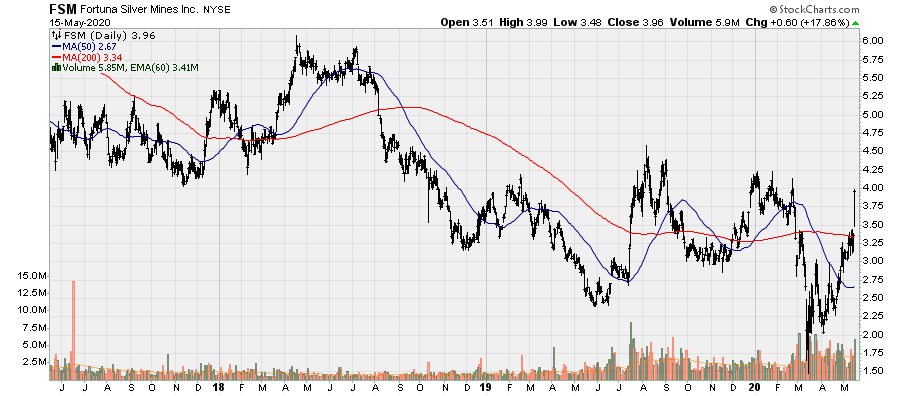

Fortuna Silver: The company continues to dilute shareholders, this time issuing 20m shares, raising $60m. Its Lindero project has taken far longer to develop than originally envisioned at much higher costs. The company now estimates total capital costs for Lindero at $315-$320m, but this is closer to $400-$440m if you take into account the cost to acquire the asset and that spent on technical studies and cash burn. Nonetheless, the company is undervalued and should easily obtain a market re-rate once Lindero is ramped to commercial production and generating material cash flow. The company also reported Q1 results, in which it produced 1.82m oz. Ag and 10.1k oz. Au but AISC per silver equivalent oz. was a bit higher at $10.70/oz. at San Jose and $16.70/oz. at Caylloma. The company generated $6.5m in operating cash flow, on the heels of a higher gold price and $16.09/oz. Ag.

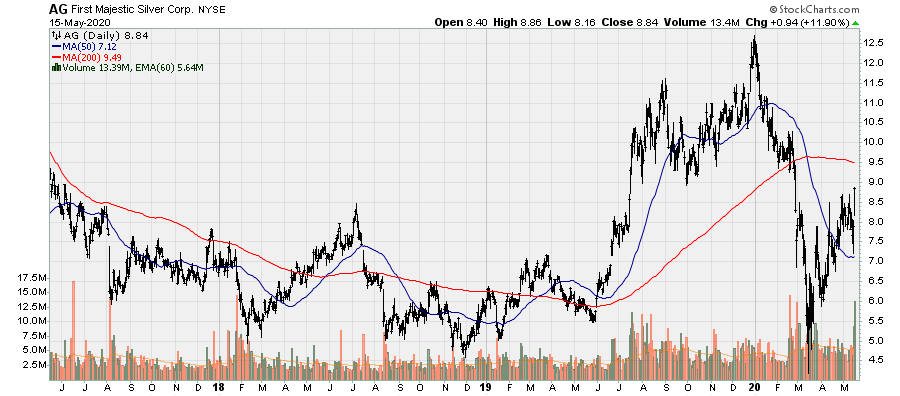

First Majestic Silver: Reported Q1 financial and operating results. Revenues were $86.1m in Q1, 1% lower relative to the comparable period in 2019, largely due to suspending sales in March as a result of low metal prices (forced liquidation due to margin calls). The company held back 292k oz. Ag and 700 oz. Au (worth approx. $5.3m at end of Q1). The company currently holds 1.045m oz. Ag and 1,459 oz. Au in inventory. The company saw reduced operating costs and AISC to $5.16/oz. and $12.99/oz. Ag. Operating cash flow was $22m ($0.11/share). The company also repurchased 275k shares at an average price of C$8.56/share (US$6.10/oz.). Despite holding back silver and gold, the company ended the quarter with $145m in cash and equivalents. The company will likely see a cash outflow due to suspension of mining operations for more than half of the current quarter.

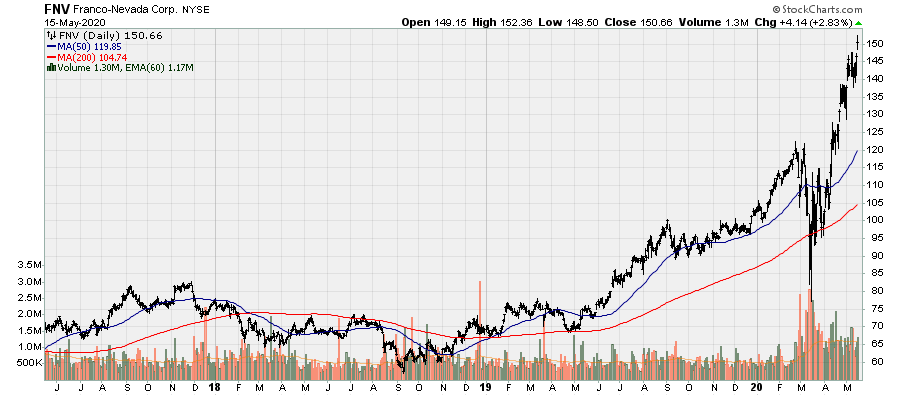

Franco-Nevada: The largest royalty and streaming company by market cap (not output) has kicked off, what I believe to the next and substantial round of royalty and stream financings over the next 12-24 months. While relatively small for the company, both cost wise and output wise, Franco-Nevada announced a $100-$150m royalty funding package for the Alpala Project. In exchange for an initial $100m paid to SolGold, Franco receives a 1% NSR royalty on the Alpala copper-gold project in northern Ecuador. SolGold has the option to upsize the royalty financing package by issuing an additional 0.50% for $50m within 8 months from the date of the agreement. SolGold retains the option, for six-years from closing, to buy back 50% of the royalty at a price that equals a 12% IRR for Franco-Nevada. Franco is also entitled to receive certain minimum royalty payments of $10m from 2028. The two companies are also discussing the option of a gold-stream and SoldGold expects that it can support up to $1b of precious metal stream financing.

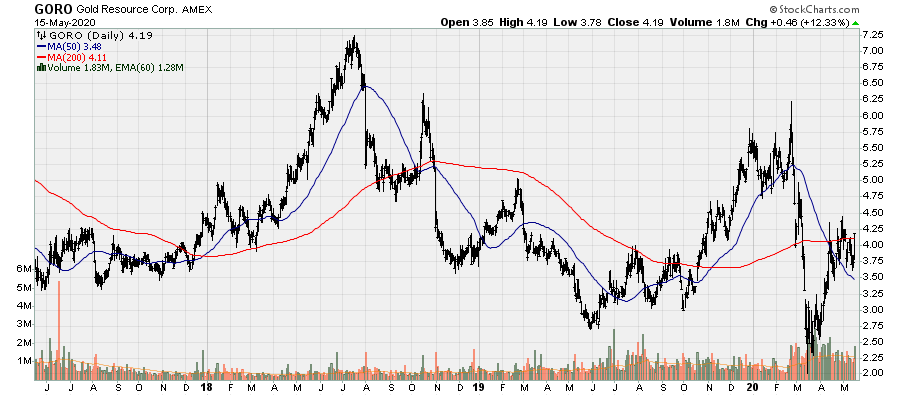

Gold Resource Corp: Announced high-grade intercepts from its Phase II drill program at the Scarlet target, 400m northwest of its Isabella Pearl mine. Near surface gold grade intercepts include: 12.19m @ 1.43 g/t Au, 9.14m @ 1.05 g/t Au, 6.1m @ 1.39 g/t Au and numerous lower-grade intercepts. The Phase III drilling program is scheduled to commence in the coming weeks. While this will never become a material operation [at least 100k oz. p.a. for at least 6yrs], It is a reasonable bolt-on operation, augmenting production and cash flow from its Mexican operations.

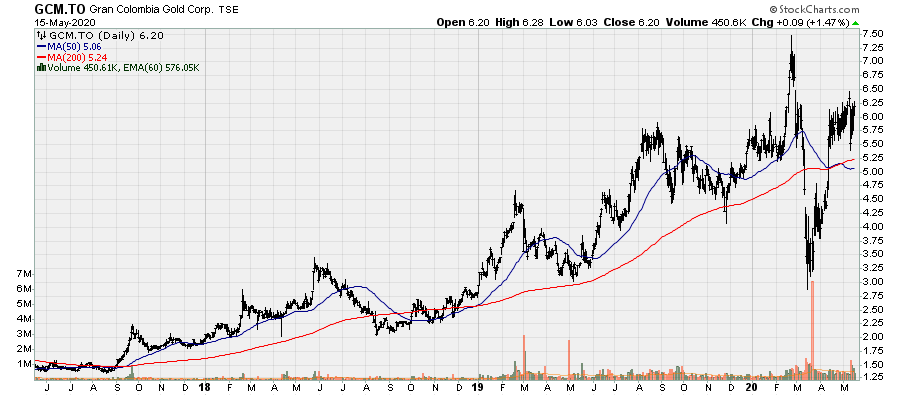

Gran Colombia: Signed a definitive agreement to complete a business combination with Gold X Mining and submitted a proposal to Guyana Goldfields to acquire all of its issued and outstanding common shares. This bid for Guyana Goldfields was higher than that made by Silvercorp last week but Guyana Goldfields rejected the bid in favor of Silvercorps’s. While the reason in unknown to why this was preferred, it could be because Silvercorp is better well financed and has a long-history of successful underground mining as well as its offer having a cash component. Gran Colombia could be better suited [given its financial constraints] toward developing either Aurora or Toroparu, not both. Nonetheless, Gran Colombia is attractive as it has two significant growth projects and owns assets in two different countries. Gran Colombia will likely both issue equity and take-out debt to finance the construction of Toroparu. It will also receive $100m from Wheaton Precious Metals as part of the gold streaming agreement. Should Gran Colombia maintain its interest in Caldas Gold, pro-forma 2024-2025 production could double to approx. 440-450k oz. Au. So this also means there is no real near-term growth.

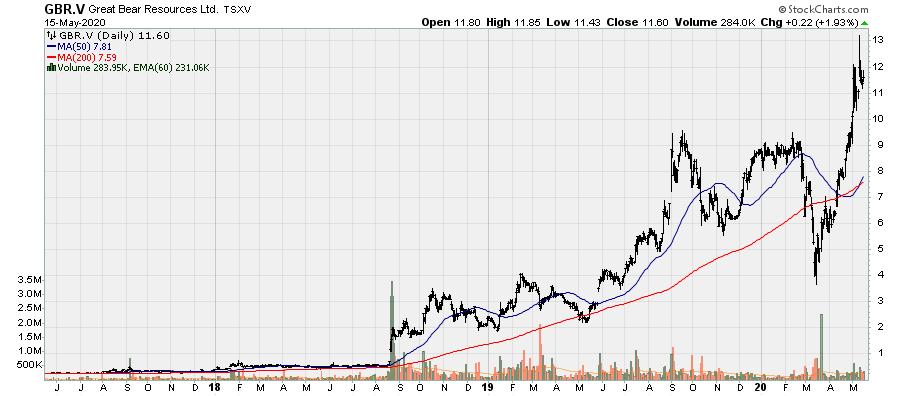

Great Bear Resources: The good news continues to roll-in for what is increasingly looking like a massive gold deposit in Red Lake. The company completed its first deep drill hole at Dixie with 19m @ 10.19 Au g/t downhole in Dixie Limb Zone. This roughly doubled the confirmed vertical depth (depth of 1,509m) of the Dixie Limb zone, intersecting the zone’s deepest, widest, and highest-grade interval to date. In Addition to the vast nearer surface mineralization at the project, this clearly illustrates the depth potential of gold mineralization at the project, which will be tested at all zones through additional deep drilling during 2020. The company also announced C$33m bough deal private placement flow-through common shares. It is a smart time to build up a treasury but as always, Great Bear is quite calculated when it comes to maintaining a tight share structure and issued 1.1765m shares @ C$17/share.

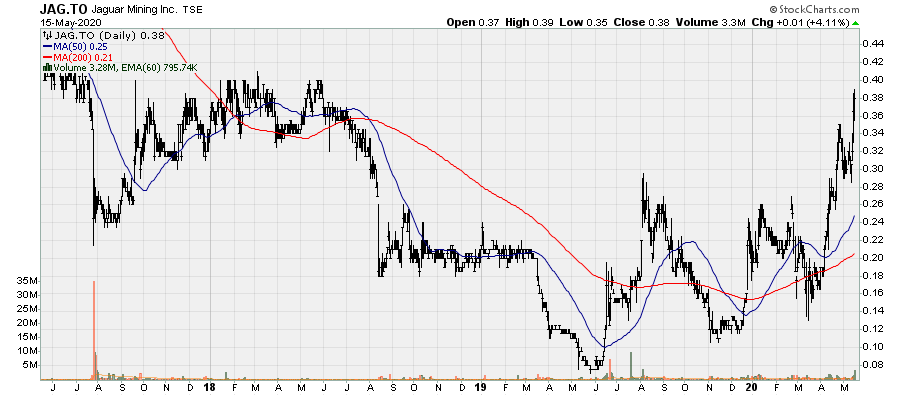

Jaguar Mining: Produced 21k oz. Au in Q1, up 28% from 16.37k oz. Au in Q1 2019. Cash operating costs and AISC declined 20% and 23% to $693/oz. and $1,103/oz., generating operating and free cash flow of $8.6m and $2.1m. The company is moving closer to its near-term objective of 25k oz. Au per quarter and being cash flow positive.

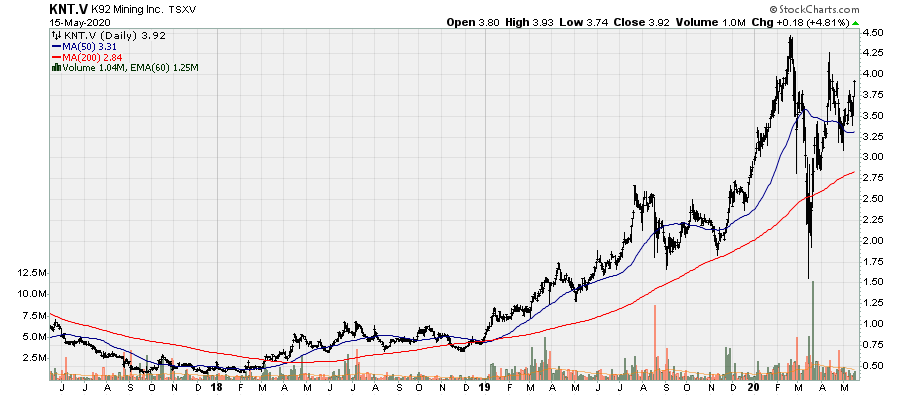

K92 Mining: The company reported the second highest quarterly production on record at 19.934k AuEq oz. Operating costs and AISC were reported at $708/oz. and $886/oz. The company generated $12.5m in operating cash flow and the company continues to report exploration success at Kora North. Costs were elevated during the quarter [relative to previous quarters] due to a significant reduction in head grade vs. the comparable period in 2019. The company withdrew guidance as a result of timing uncertainty relation to international travel and the commissioning of its stage 2 plant expansion. The company will provide an updated resource estimate in the near-term, followed by a PEA on the stage 3 expansion.

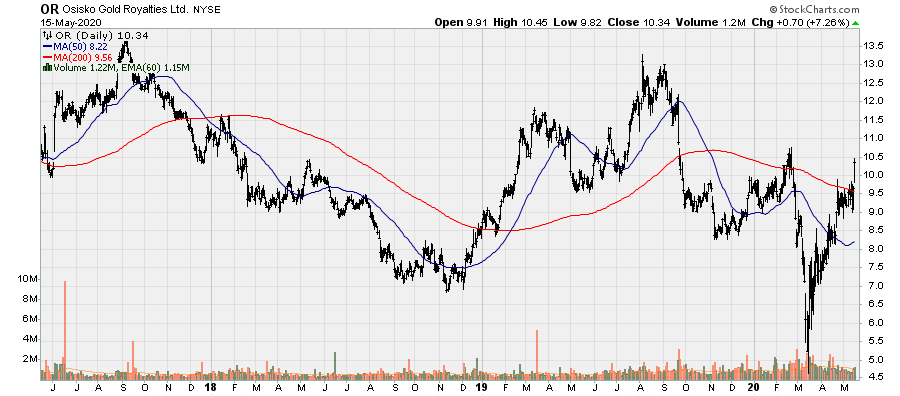

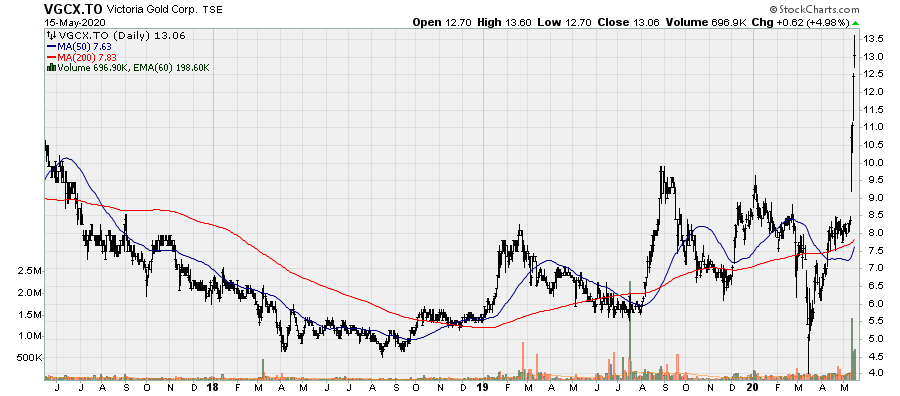

Osisko Gold Royalties: Q1 was relatively strong on the back of higher gold prices but it could have been better if not for issues at its Renard diamond stream and low diamond prices. The company earned 18.16k AuEq oz. attributable [lower relative to Q1 2019 at 19.73k oz.], generating operating cash flow of $27.9m [before changes in non-cash working capital], a 23% increase relative to Q1 2019. The company is deleveraging is balance sheet with $158m of cash on hand and up to an additional 400m available under its credit facility [which excludes the C$85m (US$60.5m) equity raise]. Its investment portfolio is also worth significantly more than it was at the end of Q1. Q2 will be marginally impacted due to suspended mining operations, most of which have resumed production. Attributable production will increase is the second half of the year, driven by its large growth royalty, a 5% NSR on Victoria Gold’s Eagle project, which is expected to achieve commercial production late in Q2-early Q3.

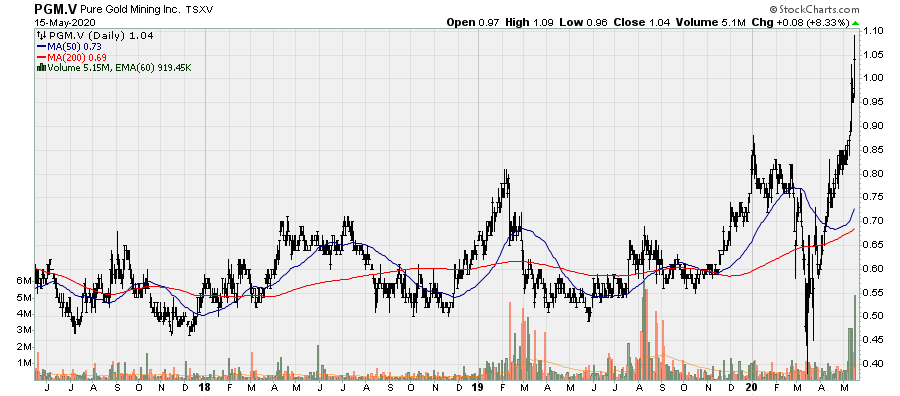

Pure Gold Mining: Canada’s next gold mine remains on track for first gold pour in Q4, provided COVID related mandated shutdowns don’t occur. This will reach production shortly after Canada’s second newest gold mine (of scale) in Victoria Gold’s Eagle mine reaches commercial production in the next 2-3 months. Pure Gold Mining is still trading at a moderate discount to Net Asset Value, which should see a market re-rate once commercial production is achieved in 1H 2021 given it is in a tier-1 mining jurisdiction and because it’s in Red Lake, which will likely be an area of consolidation over the next 24+ months.

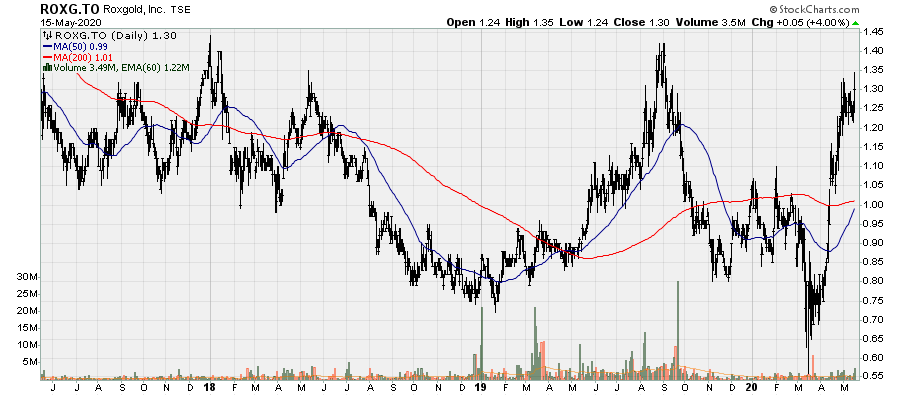

Roxgold: The company continues to generate strong cash flow, with production in the quarter of 32.38k oz. Au with cash costs and AISC of $566/oz. and $1,058/oz. sold. AISC was elevated during the quarter due to increased capital investment at the Bagassi South decline development (due to be completed in 2020). The company generated operating cash flow of $25.4m in Q1, only marginally higher than that generated in Q1 2019 due to elevated costs. Full year production is on track to achieve guidance of 120-130k oz. Au with AISC of $930-$990/oz. The company recently announced the results of the PEA for its Seguela Gold Project in Cote d’Ivoire, which outlined a project with excellent economics. The company believes further drilling with unlock further value in the project and plans to expand and optimize the PEA and will be included in the feasibility study with anticipated completion in early 2021. The company ended the quarter with $50m in cash and gold Dore.

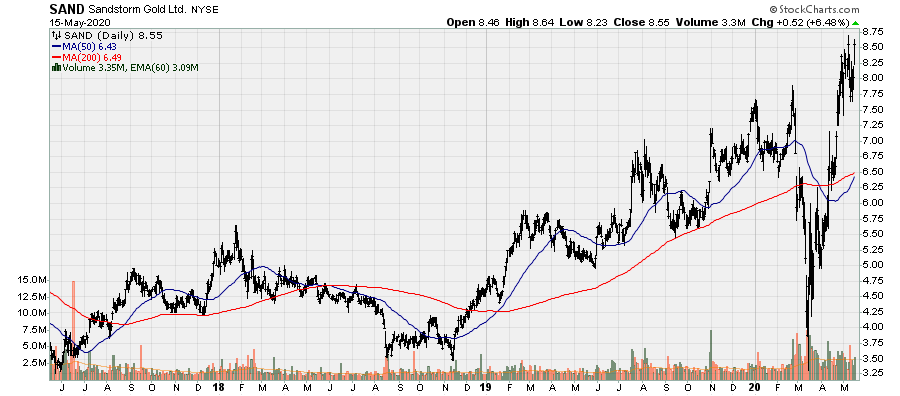

Sandstorm Gold: The company provided an asset update, which is very encouraging. Its largest asset is a 30% interest and a 2% NSR royalty on one of the highest-grade (and near surface) undeveloped gold mines, Hot Maden in Turkey. The developer and operator, Lidya Madencilik is currently conducting infill drilling while completing a pre-feasibility study and hit two absolutely incredible intercepts:

- 85.3m @ 84.3 g/t Au + 6.80% Cu from 19m

- Including 32m @ 209.4 g/t Au + 7.40% Cu from 19m

- 169.3m @ 39 g/t Au + 1.7% Cu from 20.8m

- Including 13m @ 147 g/t Au + 2.0% Cu from 63m

Beyond the major catalyst that is the Hot Maden interest and royalty, Sandstorm received its first gold delivery from Relief Canyon as part of the fixed deliveries aspect of the streaming agreement [32,022 oz. Au delivered over 5-years, dropping to a 4.0% gold and silver stream and a NSR royalties beyond the primary area of interest]. Equinox Gold released a PEA for an underground mine At Aurizona, which is being advanced to pre-feasibility, with expected completion in 2021. This will add to what is already a large royalty, that becomes a 5% NSR when the gold price is in excess of $2k Au. Furthermore, First Majestic announced it will be ramping up Santa Elena beginning May 18th as mining has been declared essential in Mexico.

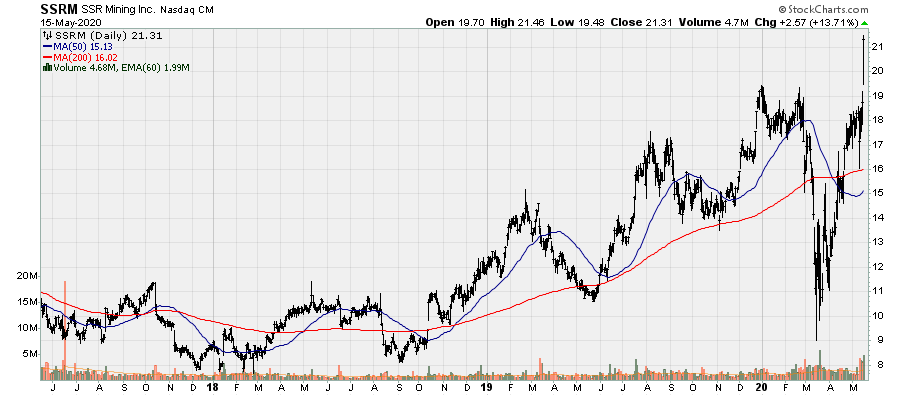

SSR Mining: The company and Alacer Gold announced an at the market merger of equals, creating a leading mid-tier gold producer. SSR’s current CEO and chairman will retain their roles for the new SSR Mining and the rest of the management team will be decided over the coming weeks. This acquisition gives the company exposure to four jurisdictions, three of which have a history of being mining friendly: Canada, Nevada (US), Turkey, and Argentina. The principal asset in this deal is the low-cost, long-lived Copler mine, which immediately becomes the company’s largest asset on a production, cash flow, and NAV basis. The combined management team has had significant success and track records regarding exploration, construction, and operations. Further, should opportunities present themselves, the new company has experience in open-pit, underground, pressure oxidation, heap leach, and flotation operations, giving the company wider scope to pursue acquisitions.

The combined company, will produce approx. 780 AuEq over the next three years with AISC of $900/oz. and will be a free cash flow machine. Pro-forma free cash flow is estimated of $450m through 2022, though this will be higher unless the gold price stays at or slightly below 1,650/oz. There are also significant organic growth opportunities in the portfolio as well as greenfield projects such as the massive Pitarilla silver deposit in Mexico and San Luis in Peru. If the company can continue its successful exploration efforts at Seabee, the mine life could and likely will be increased. There are also optimization measures that could be undertaken at Marigold to increase annual production. There are near-mine site opportunities to either increase annual production or maintain current production levels at Copler for a long period of time. The Copler project clearly has district scale potential in that new deposits could be identified. Attributable production (80%) from Copler should average 250-270k oz. over the next several years with AISC of $750-$775/oz.

A few days following this merger, SSR Mining announced it had divested its equity position in SilverCrest Metals for C$90m (US$64m). The company also reported Q1 results, with AuEq production of 107.33k oz. at AISC of roughly $1,200/oz., due to elevated costs at all three operations due to various reasons i.e. ($10.93m of capitalized stripping (Marigold), higher capital expenditures (Seabee) and mining suspensions. SSR also redeemed outstanding 2.875% senior convertible notes for $115m.

In addition to 3.3m oz. of gold reserves, there is an additional 2.7m oz. of indicated resources and 2m oz. Inferred at Copler. In short, this acquisition makes a lot of sense and has significant growth opportunities, notably Pitarilla, which has the potential, once in production, to produce upwards of 15m oz. Ag annually over a long mine life. Lastly, the company has a significant cash position (approx. $650m) with moderate debt (approx. $320m). With the free cash flow generation potential, this debt can be paid off in about 3-quarters. It remains to be seen whether SSR will pursue additional M&A opportunities but either way, it already has significant growth through its project pipeline.

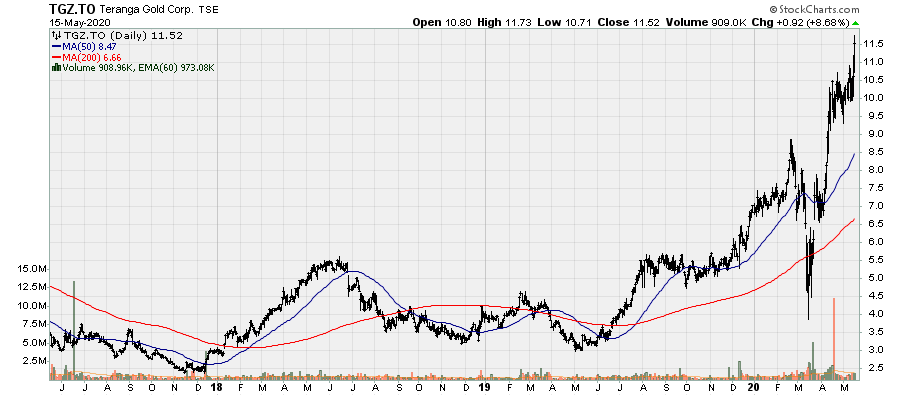

Teranga Gold: The company reported a strong Q1 2020, highlighted by a 27% increase in production to 91.3k oz. Au (vs. 71.95k oz.) and a 19% increase in the gold price at AISC of $1,097/oz. There were issues with the quarter at first glance due to swings in inventory stockpile, supplied build-up and settlements of gold advances but it was a strong quarter operationally as it was expected to mine lower grade at Sabodala negated by what will be the strongest period of the year from Wahgnion. Despite a material inventory build, adjusted operating cash flow increased 9% to $28.74m (before changes in non-cash working capital and excluding inventories). Unsold bullion inventory increased to $38m (23.6k oz. Au) due to COVID related delays in gold shipments in late March. The company ended the quarter with $40m in cash and this should increase and potentially double in Q2 on the back of increased sales (from inventory) and a higher gold price. The company is trading at a very attractive valuation and significant additional value will be unlocked as the Massawa project continues to advance.

Victoria Gold: The slower than expected ramp-up at Eagle during the first quarter is being made up for as seen through its April numbers and remains on track to reach commercial production as early as late Q2, if not Q3. In Q1, the company produced just 10.54k oz. Au but in April, the company produced 6.77k oz. This will continue in the coming quarters and should achieve an annual run rate of 13-14k oz./month within the next three to four months and exiting the year at a run rate of 205-210k oz. on an annualized basis. Victoria’s stock price didn’t at all react to the news when announced but proceeded to advance 27% the following day and continued to run higher through the end of the week. Once full-scale production is achieved and it shows an AISC profile between $775-$850/oz., it will likely be acquired as it is a perfect size (200-210k oz. for about 11-years) in a Tier-I jurisdiction with exploration upside.

About the author