The gold price took off higher as soon as trading began at 6:00 p.m. in New York on Thursday evening -- and that rally was capped at 9:45 a.m. China Standard Time on their Friday morning. It then had a quiet down/up move that ended around 2:50 p.m. CST -- and was then sold/engineered lower until around 8:35 a.m. in Globex trading in London. It then began to chop quietly higher until it really began to sail starting five minutes after the 8:20 a.m. COMEX open in New York. 'Da boyz' obviously stepped in shortly after the equity markets opened at 9:30 a.m. EST -- and again for the final time minutes after the 1:30 p.m. COMEX close. It was sold/engineered very quietly lower from that juncture until trading ended around 3 p.m. EST.

The low and high ticks in gold were reported as $4,174.60 and $4,263.10 in the February contract...an intraday move of $88.50 an ounce. The December/ February price spread differential in gold at the close in New York yesterday was $36.60...February/April was $29.90...April/June was $30.10 -- and June/ August was $29.60 an ounce.

Gold was closed in New York on Friday afternoon at $4,217.70 spot...up $61.90 on the day -- and $6.80 off its Kitco-recorded high tick. Net volume, which includes Thursday's as well, was exceedingly light at around 142,500 contracts -- and there were around 12,200 contracts worth of roll-over/switch volume on top of that.

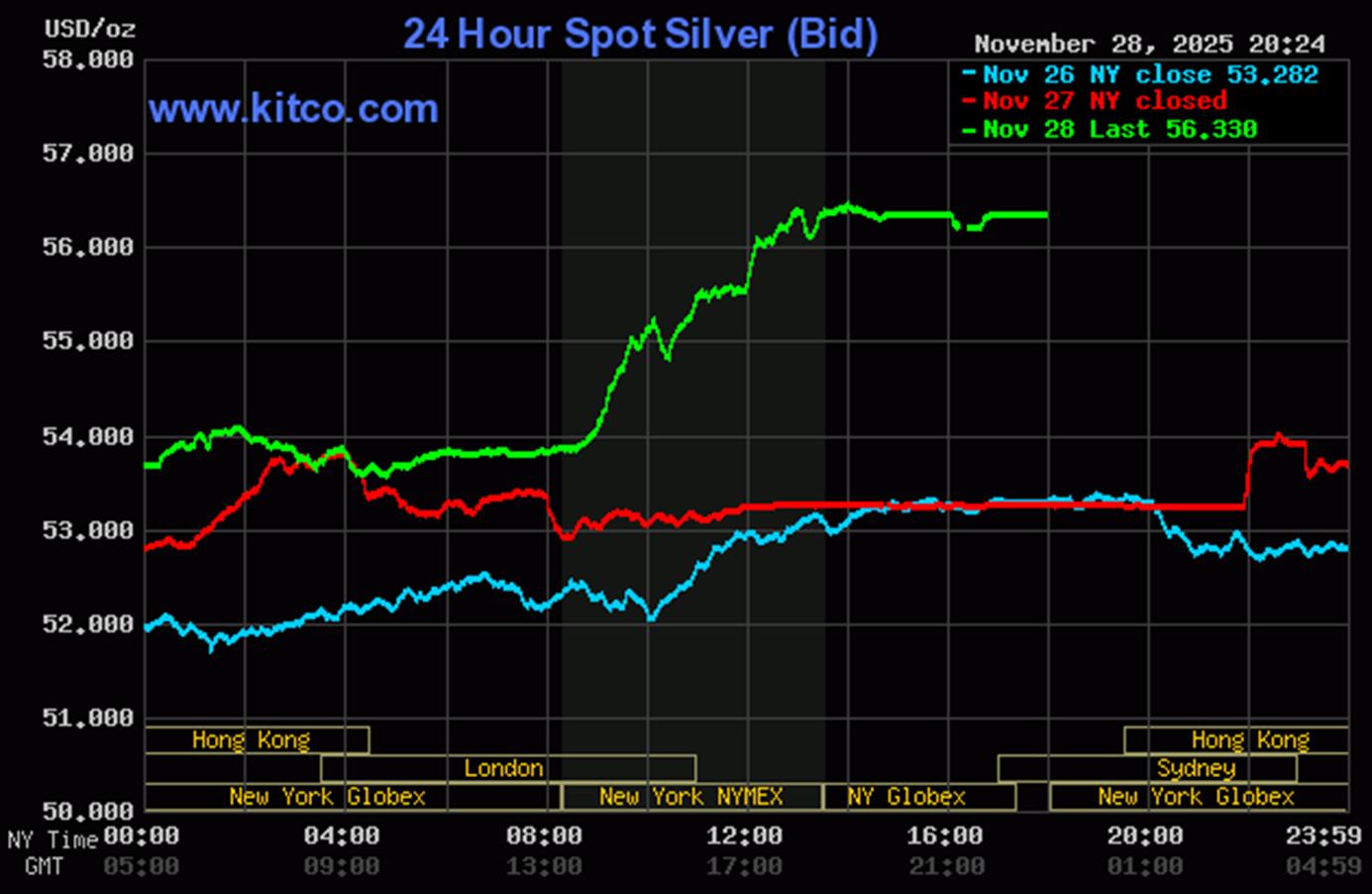

Silver rallied very decently until it ran into 'something' around 11:15 a.m. in Globex trading in Shanghai -- and then got hammered lower until around 12:05 p.m. CST. Its ensuing rally ended around 2:50 p.m. CST -- and it was quietly downhill from that point until shortly before 10 a.m. in London. It then crept quietly higher until it really began to sail starting around 9 a.m. in COMEX trading in New York. Its boomer rally from that juncture ran into varying amounts of 'resistance' until its high tick was set at precisely 2:00 p.m. EST in after-hours trading. It sagged a bit from there until the market closed.

The low and high ticks in silver were recorded by the CME Group as $53.22 and $57.245 in the March contract...and eye-watering intraday move of $4.025 an ounce. The December/March price spread differential in silver at the close in New York yesterday was an unbelievable 71.7 cents, which is unconscionable...March/ May was a hefty 42.4 cents. This means that for every contract rolled out of December into May, it would cost 5,000 oz. X [71.7 + 42.4] = $5,705! The CME Group is just ripping the faces off everyone that wants to roll out of December now. May/July was an equally outrageous 41.0 cents an ounce.

Silver was closed on Friday afternoon in New York at $56.33 spot...up a spectacular $3.09 on the day -- and 12 cents off its Kitco-recorded high tick. Net volume, which also includes Thursday's, was nothing special at a bit over 86,000 contracts...of which 33,000 contracts happened on Thursday -- and there were a bit under 12,000 contracts worth of roll-over/switch volume in this precious metal.

Platinum began to rally at 6:50 p.m. in Globex trading in New York on Thursday evening -- and you can easily spot the three times that 'da boyz' stepped in to prevent its price from running away to the upside...with the last time being at its 12:10 p.m. EST high tick in COMEX trading in New York. It was then sold/ engineered lower until five minutes after the 1:30 p.m. COMEX close -- and was then allowed to rally a bit until trading ended. Platinum was closed at $1,655 spot...up 49 dollars on the day -- and 8 bucks off its Kitco-recorded high tick.

![]()

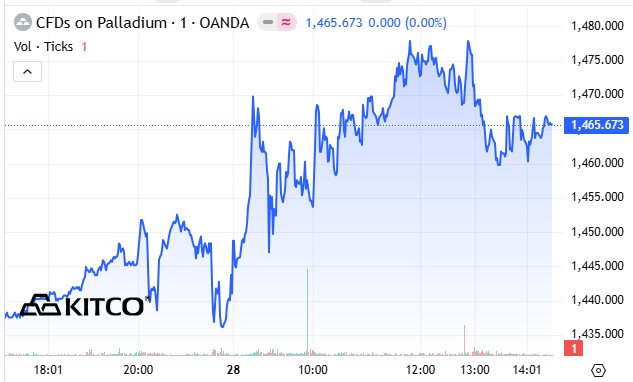

Palladium had a very broad and choppy ride higher in both Globex and COMEX trading on Friday -- and its rally ran into 'grief' around 11:47 a.m. in COMEX trading in New York. It then had an engineered, choppy and descending down/ up move until the markets closed. Palladium was closed at $1,431 spot...up 20 bucks on the day -- and 13 dollars off its Kitco-recorded high tick.

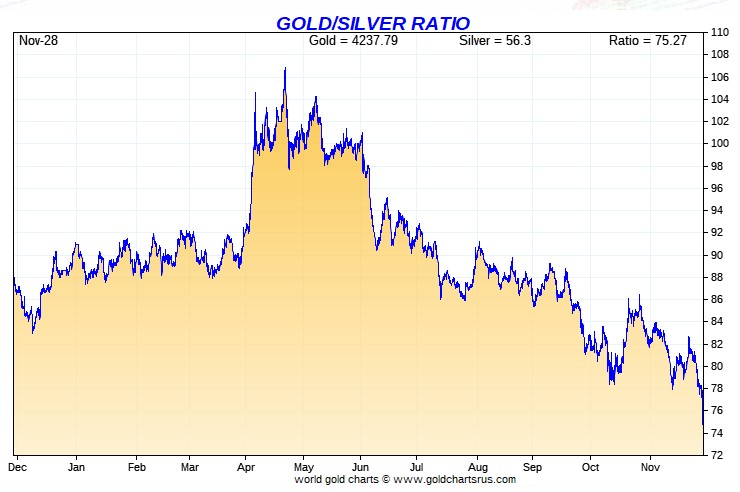

Based on the kitco.com spot closing prices in silver and gold posted above... the gold/silver ratio worked out to 74.9 to 1 on Friday...compared to 78.1 to 1 on Thursday.

Here's the 1-year Gold/Silver Ratio chart from Nick -- and updated with this past week's data. Click to enlarge.

![]()

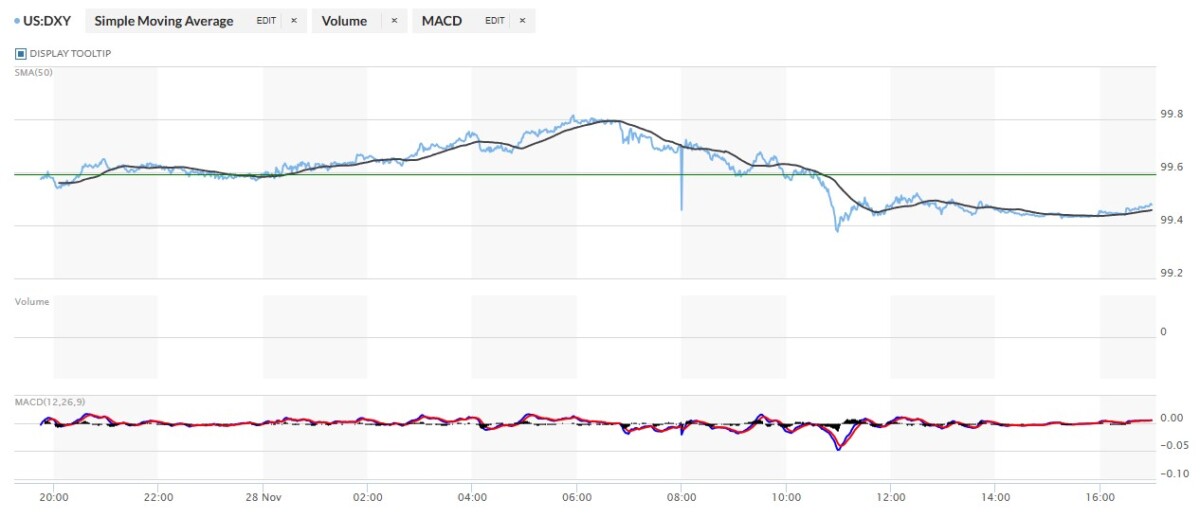

The dollar index closed very late on Thursday afternoon in New York at 99.60 -- and then opened lower by 2 basis points once trading commenced at 7:45 p.m. EST on Thursday evening...which was 8:45 a.m. China Standard Time on their Friday morning. It then wandered very quietly sideways until a quiet rally commenced starting around 12:53 p.m. CST. That topped out at 10:55 a.m. GMT in London -- and it was downhill from that point until it rolled over hard starting around 10:20 a.m. in New York. 'Gentle hands' appeared at 10:59 a.m. EST -- and it then chopped a bit higher until around 12:30 p.m. It then had a very quiet and descending down/up move until the market closed at 5:00 p.m. EST.

The dollar index finished the Friday trading session in New York at 99.48...down 5 basis points from its close on Thursday -- and 12 basis points from its close on Wednesday.

Here's the DXY chart for Friday...thanks to marketwatch.com as usual. Click to enlarge.

![]()

Here's the 6-month U.S. dollar index chart...courtesy of stockcharts.com as always. The delta between its close...99.60....and the close on DXY chart above, was zero basis points. Click to enlarge.

![]()

As has been the case for a very long time now...the goings-on in the currencies have been completely decoupled from the price action in the precious metals. This is always the case when the collusive commercial traders are running the show in the COMEX/Globex trading system...like they are now.

U.S. 10-year Treasury: 4.0170%...up 0.0190/(+0.4752%)...as of the 1:59:54 p.m. CST close

The Fed was forced to step in around 10:52 a.m. EST on Friday morning to prevent the ten-year from closing far higher than it was allowed.

The 10-year Treasury was down 4.6 basis points on the week...but only so because of the daily interventions by the Fed.

Here's the 5-year 10-year U.S. Treasury chart from the yahoo.com Internet site -- which puts the yield curve into a somewhat longer-term perspective. Click to enlarge.

The 10-year hasn't been allowed to trade above its 4.92% high tick set back on October 15, 2023 -- and has been in almost continual decline since. But I still suspect that we've seen the 3.9482% low for this cycle...which was set back on October 22. As for a rate cut at the upcoming December FOMC meeting...place your bets.

![]()

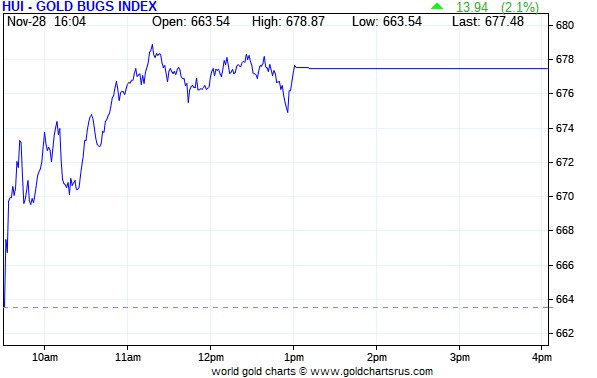

The gold shares began to chop unevenly higher as soon as the markets opened in New York on Friday morning -- and their respective high ticks were set around 11:15 a.m. They then chopped a tad lower until trading ended at 1:00 p.m. EST. The HUI close up an unimpressive 2.10 percent.

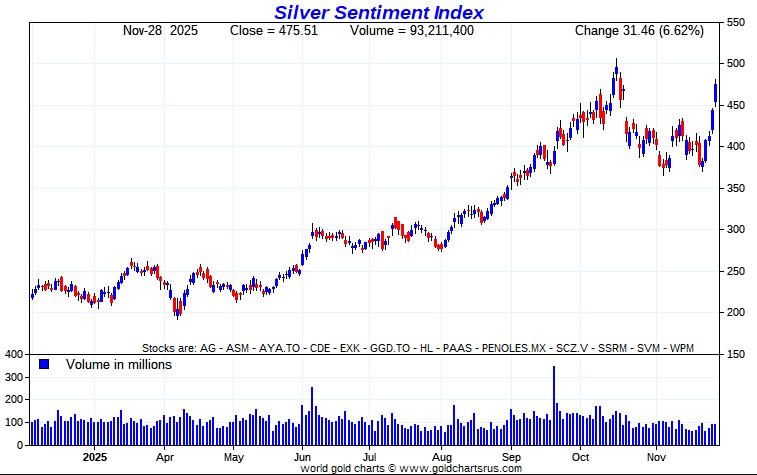

And despite silver's big $3+/5.80% gain on the day, Nick Laird's Silver Sentiment Index only closed higher by 6.62 percent. I was underwhelmed. Click to enlarge.

The only three silver companies with double-digit gains yesterday were Endeavour Silver, First Majestic Silver -- and Aya Gold & Silver...closing higher by 15.20...12.73 and 12.00 percent respectively. The biggest underperformer was Peñoles, as it closed up only 1.60 percent -- and on exceedingly low volume.

Trading volumes were very low for most of these stocks -- and in almost all cases, volumes didn't even make it up to their average daily volume levels. I suspect it had to with the fact that it was Black Friday -- and high absenteeism. That, I suspect, was the same reason that the precious metal equities didn't perform all that well...especially the silver stocks.

There was this news from Santacruz Silver Mining on Thursday that I missed.

The silver price premium in Shanghai over the U.S. spot price on Friday was 3.96 percent.

The reddit.com/Wallstreetsilver website, now under 'new' and somewhat improved management, is linked here. The link to two other silver forums are here -- and here.

![]()

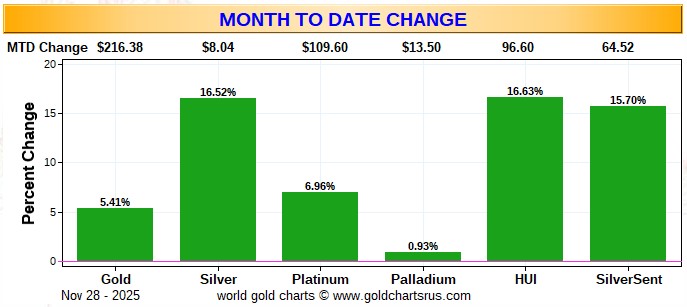

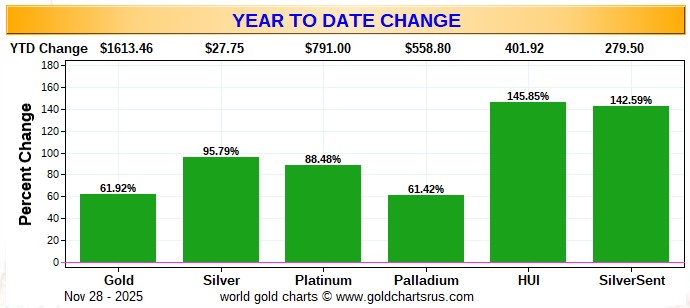

Here are two of the usual three charts that appear in this spot in every weekend missive. They show the changes in gold, silver, platinum and palladium in both percent and dollar and cents terms, as of their Friday closes in New York — along with the changes in the HUI and the Silver Sentiment Index.

Because Thursday was a holiday in the U.S....there no weekly chart...as Nick's formula for computing the weekly gain is the last five trading days which, in this case, would include the previous Friday...November 21...making it useless. But as 'useless' as it is...the Silver Sentiment Index was up 24.17% over the last five trading sessions in New York.

Here's the month-to-date chart which now shows all of November -- and although silver continues to outperform gold -- and by an outrageous percentage, that hasn't helped its associated equities...where the metal has actually outperformed the shares, which is hard to believe. Like last week, the HUI is still the king of the castle. Click to enlarge.

Here's the year-to-date chart -- and even though the silver price has outperformed the gold price by more than 50% on a relative basis vs. gold year-to-date, its associated equities still trail the gold shares. I didn't think that would be possible...especially considering that silver is now at new nominal all-time high...but the charts don't lie. The silver equities should be 50% higher than they are now to be equal to the gains in the gold equities vs. the gold price itself. Click to enlarge.

Despite the fact that silver has now broken the $56 barrier -- and the silver well in London is running close to empty, the gold/silver ratio remains at a farcical 74.9 to 1 as of the Friday's close. The 'normal' and historical ratio is around 15 to 1...which would put silver at about $281. And if priced at the ratio of 7:1 that it comes out of the ground at, compared to gold...that would put silver at $602 an ounce. So a triple-digit silver price is in our future -- and all that remains to be resolved is what that number will be -- and how soon 'da boyz' allow it to happen.

![]()

The CME Daily Delivery Report for Day 2 of December deliveries showed that 5,074 gold and 975 silver contracts were posted for delivery within the COMEX-approved depositories on Tuesday.

In gold, the largest short/issuer was British bank HSBC, issuing 3,333 contracts out of it house account -- and next down the list after them was Morgan Stanley, issuing 998 contracts out of its house account as well. In third spot was Australia's Macquarie Futures, issuing 499 contracts in total ...276 from its house account -- and the other 223 from its client account.

There was a monster list of long/stoppers -- and the two largest were JPMorgan and Canada's Scotia Capital/Scotiabank, picking up 2,052 and 1,037 contracts respectively...the latter for their house account.

In silver, the two biggest short/issuers were JPMorgan and and Australia's Macquarie Futures, issuing 744 and 109 contracts...all from their respective client accounts. The three largest long/stoppers were JPMorgan, Canada's RBC [Royal Bank of Canada] Capital Markets -- and Deutsche Bank...picking up 465, 167 and 164 contracts respectively...JPMorgan for its client account.

In palladium, there were 264 contracts issued and stopped -- and the largest short/issuer for those was French bank BNP Paribas...issuing 520 contract out of its client account.

The link to yesterday's Issuers and Stoppers Report is here -- and it's worth a minute of your time if you have the interest.

Only two days into the December delivery month, there have already been 23,970 gold/2.397 million troy ounces...plus 8,305 silver contracts/ 41.525 million troy ounces...issued and stopped so far -- and the delivery month has just started. One can only fantasize as to what these numbers will be when the books are closed on December 31.

The CME Preliminary Report for the Thursday and Friday trading session combined showed that gold open interest in December dropped by 19,239 COMEX contracts, leaving 7,712 still around...minus the 5,074 contracts out for delivery on Tuesday as per the above Daily Delivery Report. Wednesday's Daily Delivery Report showed that 18,896 gold contracts were actually posted for delivery on Monday, so that means that 19,239-18,896=343 gold contracts disappeared from the December delivery month.

Silver o.i. in December cratered by 6,959 COMEX contracts, leaving 2,907 still open, minus the 975 contracts out for delivery on Tuesday as per the above Daily Delivery Report. Wednesday's Daily Delivery Report showed that 7,330 silver contracts were actually posted for delivery on Monday, so that means that 7,330-6,959=371 more silver contract were added to December deliveries. That's a lot!

Total gold open interest in the Preliminary Report on Thursday night fell by 11,478 COMEX contracts, which would be mostly delivery related -- but total silver o.i. rose...but only by 426COMEX contracts. I'm sure the gross number was more than that, but the big deliveries on First Day Notice masked that fact -- and the COT Report that shows this, wont' be out until late December at the earliest.

[I checked the final total open interest number for gold for Wednesday -- and it showed only a tiny decline...from -109 contracts, down to -1,343 contracts. Final total silver o.i. for Wednesday actually rose...from 7,172 COMEX contracts...up to 7,255 contracts. I sure hope that it was those uneconomic and market-neutral spread trades being added, but there's no way to know for sure.]

Gold open interest inJanuary in the Preliminary Report on Friday night rose by 76 contracts, leaving 3,012 still around -- and silver o.i. in January increased by 273 contracts, leaving 4,069 still open. I'll have the final numbers for Friday in Tuesday's column...as preliminary numbers for a future delivery month can be wildly misleading.

![]()

![]()

There were no reported changes in GLD yesterday...but an authorized participant added a scant 906,950 troy ounces of silver to SLV.

It's a given that both these ETFs are owned copious amounts of metal...SLV in particular. It remains to be seen if any of that silver ever materializes...or did the authorized participants short the required number of SLV shares in lieu of depositing physical metal? We'll know for sure/hopefully in the next short report that's due out on Tuesday, December 9...as yesterday was the cut-off for it.

The SLV borrow rate started the Friday session at 1.37% -- and closed at 1.13%...with 9.7 million shares available to short by the end of the day. The GLD borrow rate began the day at 0.32% -- and finished it at 0.35%... with 6.7 million shares available.

In other gold and silver ETFs and mutual funds on Earth on Thursday and Friday combined ...net of any changes in COMEX, GLD and SLV activity, there were a net 86,920 troy ounces of gold added...but a net 176,280 troy ounces of silver were removed.

There was no sales report from the U.S. Mint.

The Royal Canadian Mint posted their Q3/2025 Report on their website -- and it showed that their gold bullion sales [mostly gold maple leafs] in that quarter were down 7.5% from Q3/2024. Year-to-date, sales are down 12.3% ...to 367.1 million troy ounces...from 418.4 million troy ounces ytd/2024. Silver maple leaf sales in Q3/2025 were down 45.8% compared to Q3/2024. Year-to-date silver maple leaf sales are down 43.6% to 6.469 million...from 11.476 million ytd/2024.

The link to their Q3/2025 quarterly report is here -- and the relevant data is on page 9.

![]()

![]()

There was huge activity in gold over at the COMEX-approved depositories on the U.S. east coast on Wednesday. Nothing was reported received...but 209,590 troy ounces were shipped out involving four different depositories.

The two largest amounts were the 123,959 troy ounces that left Asahi -- and the 54,978.210 troy ounces/1,710 kilobars that departed Brink's, Inc.

There was monster paper activity, as 1,129,501 troy ounces were transferred involving four different depositories -- and all of it from the Registered category and back into Eligible...most likely to save on storage fees. The largest amount by far were the 1,104,669 troy ounces that made that trip over at Brink's, Inc.

I continue to suspect that all these gold outflows from the COMEX since the start of October...4.298 million troy ounces...has to do with a looming delivery problem on the LBMA.

The link to all of Wednesday's monster gold action is here.

There was decent activity in silver, as 556,693 troy ounces were dropped off at Asahi -- and a total of 657,249 troy ounces were shipped out.

The largest 'out' amount were the 434,727 troy ounces that left JPMorgan... with the remaining 222,522 troy ounces departing Asahi.

There was monstrous paper action, as a net 11,300,086 troy ounces were transferred from the Registered category and back into Eligible. The largest amount by far were the 13,412,156 troy ounces transferred in that direction over at JPMorgan -- and the 987,975 troy ounces transferred in that same direction over at CNT. There were 1,214,094 troy ounces/two truckloads adjusted out of existence in the Eligible category over at Brink's, Inc. -- and what that was about...who knows.

The link to all of Wednesday's monster silver action is here.

The Shanghai Futures Exchange updated their silver inventories as of the close of business on their Friday -- and it showed that a further 382,789 troy ounces/ 11.906 tonnes were added... leaving their silver inventories at 17.969 million troy ounces/558.882 metric tonnes.

![]()

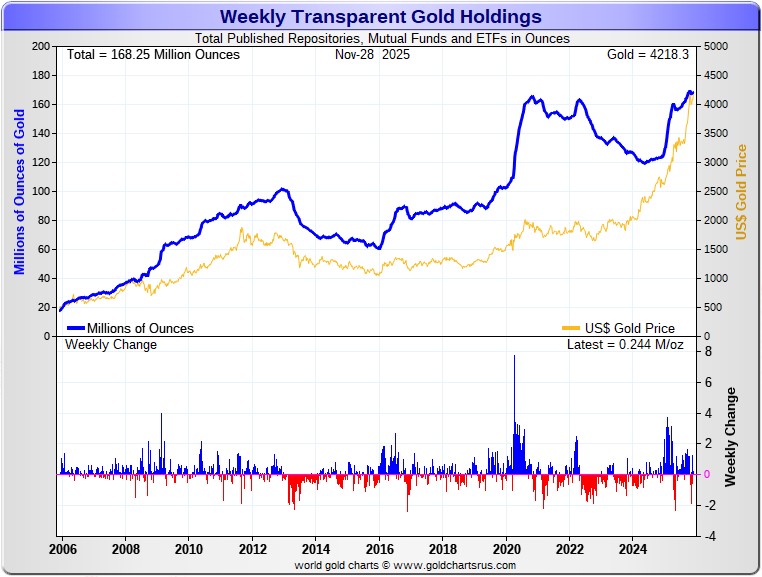

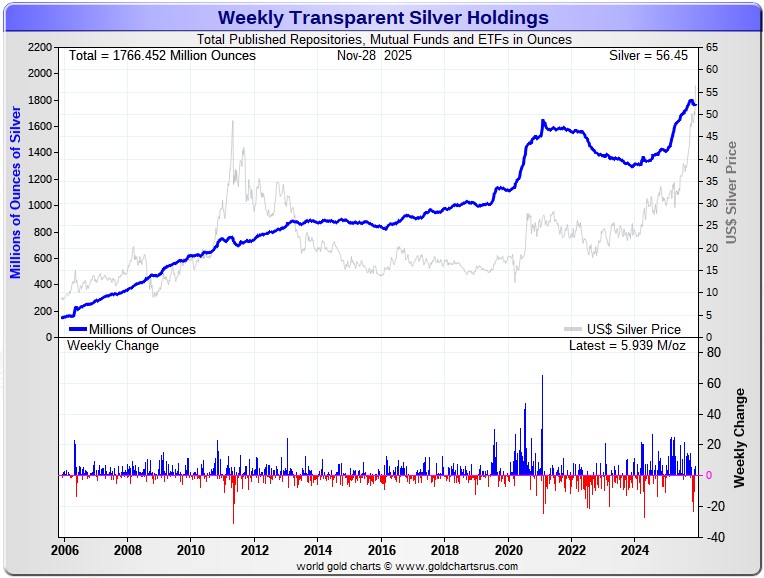

Here are the usual 20-year charts that show up in this space in every weekend column. They show the total amounts of physical gold and silver held in all known depositories, ETFs and mutual funds as of the close of business on Friday.

During the business week just past, there were a net 244,000 troy ounces of gold added -- and a net 5.939 million troy ounces of silverwere added as well.

According to Nick Laird's data on his website, a net 1.022 million troy ounces of gold were added to all the world's known depositories, mutual funds and ETFs during the last four weeks. The two largest 'in' amounts were the 1.153 million oz. that went into China's ETFs, followed by the 1.117 million troy ounces into those Crypto currencies/Tether in this case. The only large withdrawal that mattered were the net 1.811 million troy ounces that left the COMEX -- and all London-bound, I suspect.

The amount of gold in all the world's ETFs and mutual funds remains barely above its old all-time high of late 2020...but should be far higher considering that gold is now some distance north of $4,000 the ounce.. more than double the price it was back then.

It should be noted that the amount of silver held in all these depositories, ETFs and mutual funds is a very noticeable amount above its old all-time high inventory level of January 2021. But it should be far higher than it is, because silver is also handily more than double the price it was back then.

A net 1.741 million troy ounces of silver were also removed during that same 4-week time period.

The biggest 'in' amount over that four-week period were the 13.527 million troy ounces shipped into SLV...followed by the 5.523 million troy ounces into iShares/SSLN. That was followed by the 2.512 million ounce into Aberdeen -- and the 1.584 million oz. into WisdomTree. The only 'out' amount that mattered were the 25.667 million that left the COMEX -- and mostly London bound.

Retail sales are just OK -- and from what I've been told, dealers aren't having any trouble getting inventory...which is a big change from six or so weeks ago when everything was as tight as a drum.

However, physical demand in silver at the wholesale level remains enormous/ rapacious. COMEX silver deliveries have been huge all year. November deliveries ended the month at 19.68 million troy ounces...which is amazing, considering the fact that November is not a scheduled delivery month for either silver or gold. There were also a whopping 1.267 million troy ounces of gold issued and stopped in November as well.

And, as mentioned further up in the Daily Delivery Report, we're only into Day 2 of December deliveries -- and there have already been 2.397 million troy ounces of gold...plus a knee-wobbling 41.525 million troy ounces of silver issued and stopped.

This "rapacious" silver demand will continue until available supplies are depleted...which now appears imminent once more -- and we're also fast approaching the sixth year of a structural deficit in silver according to the ongoing reports from The Silver Institute.

The vast majority of precious metals being held in these depositories are by those who won't be selling until the silver price is many multiples of what it is today.

Sprott's PSLV is the third largest depository of silver on Planet Earth with 204.6 million troy ounces...unchanged for the second week in a row -- and a great distance behind the COMEX, which has now been demoted to the second largest silver depository, where there are 456.8 million troy ounces being held...down a further 3.9 million troy ounces this past week...but minus the 103 million troy ounces being held in trust for SLV by JPMorgan.

That 103 million ounce amount brings JPMorgan's actual silver warehouse stocks down to around the 95.6 million troy ounce mark...quite a bit different than the 198.6 million they indicate they have...down a net and further 1.0 million troy ounces on the week.

PSLV remains a very long way behind SLV as well -- now the largest silver depository...with 501.9 million troy ounces as of Friday's close...up 11.3 million ounces from last week.

The latest short report [for positions held at the close of business on Friday, November 14] showed that the short position in SLV declined by a smallish 7.97%...from the 56.38 million shares sold short in the prior report...down to 51.89 million shares in this latest short report that came out this past Tuesday...9.40% of total SLV shares outstanding. This amount remains grotesque, obscene, hideous -- and fraudulent beyond all description...as there is no physical silver backing any of it as the SLV prospectus requires.

BlackRock issued a warning five or so years ago to all those short SLV that there might come a time when there wouldn't be enough metal for them to cover. That would only be true if JPMorgan decides not to supply it to whatever entity requires it. However, we are far beyond that point now, as the short position in SLV will never be covered through the deposit of physical silver, as it just doesn't exit -- and never will.

The next short report...for positions held at the close of trading on Friday, November 28...yesterday...will be posted on The Wall Street Journal's website on Tuesday afternoon EST on December 9.

Then there's that other little matter of the 1-billion ounce short position in silver held by Bank of America in the OTC market...with JPMorgan & Friends on the long side. Ted said it hadn't gone away -- and he'd also come to the conclusion that they're short around 25 million ounces of gold with these same parties as well. Once the silver price approaches three digits, we'll see if they need to get bailed, like Bear Stearns did back in 2008 -- and for the same reason.

The latest OCC Report for Q2/2025 came out a bit over two months ago now -- and it showed that the precious metal derivatives held by the four largest U.S. banks only increased by $25.8 billion/4.89% from Q1/2025...which is nothing much at all -- and that's despite the fact that precious metal prices rose fairly substantially during that time period.

JPMorgan's precious metals derivatives rose from $323.5 billion, up to $358.5 billion in Q2/2025 -- and Citigroup's also rose, but not by much, from $142.8 billion...up to $150.7 billion. BofA's fell from $61.7 billion, down to 44.7 billion -- and the derivatives position held by Goldman Sachs is a piddling and immaterial $219 million -- down from the $269 million held in Q1/2025.

But with JPMorgan holding 64.7% of all the precious metals derivatives... Citibank holding 27.2% -- and Bank of America about 8% of the total of the four reporting banks, it's only JPMorgan and Citigroup that matter.

And as I keep pointing out in this spot every weekend, the OCC indicator is flawed for two very important reasons, as way back 10-15 years ago, this report used to include the top dozen or so U.S. banks -- and included the likes of Wells Fargo and Morgan Stanley, amongst others... that are card-carrying members of the Big 8 shorts. Now the list is down to just four banks...so a lot of data is hidden...which is certainly the reason why the list was shortened. On top of that, the list doesn't include the non-U.S. banks that are members of the Big 8 shorts: British, French, German, Canadian -- and Australian.

On Friday the CFTC put up the next Commitment of Traders Report...this one as of the Tuesday cut-off on October 11. As I mentioned two weeks ago, the CFTC won't be caught up to date until Friday, January 23, 2026...so all the COT data published between now and then is very much 'yesterday's news' -- and I shan't bother reporting it. However, I will mention that the commercial net short positions in both gold and silver continue to decline at a goodly clip.

![]()

CRITICAL READS

Frustration, Confusion Ripple Across Markets on CME Outage

The Chicago Mercantile Exchange Group proudly describes itself as the place “where the world comes to manage risk.” Except on Friday, the world was shut out.

Trading of futures and options was halted due to a fault at a data center, spilling over into multiple markets and affecting contracts covering trillions of dollars.

More than nine hours after the first alert appeared on the CME website, the company said services were starting to come back.

During the outage, there was disruption to S&P 500 futures as well as the EBS foreign exchange platform and everything from Treasuries to U.S. crude oil.

In Singapore, one oil trader said when the initial alert was issued around 10:30 a.m. local time on Friday, they thought it was a hoax because the trades and quotes were still streaming in. But a few minutes later, the screen suddenly froze and they were booted out of the NYMEX platform.

With the go-to service out, screens that would usually be a flickering wall of numbers ground to a halt, and traders had to seek out other options to keep trading and operating.

The Bloomberg story from 7:03 a.m. PST on Friday morning was picked up by yahoo.com -- and I found it on Sharps Pixley. Another link to it is here.

![]()

![]()

It's not just that U.S. and global markets are now in a hyper volatile condition. Marketplace liquidity has turned acutely unstable. In general, global markets are in a state of liquidity overabundance, fueled by unprecedented leveraged speculation across markets. At the same time, risk aversion has made some headway in key sectors including crypto and AI. Overheated markets are vulnerable to risk aversion developing into a more systemic de-risking/ deleveraging dynamic.

Bucking the market rally, Nvidia declined 1.2% this week. The stock is down 12.7% for the month. Strategy sank 34.5% in November, Super Micro Computer 35.7%, Oracle 23.3%, Coinbase 21.0%, Arm Holdings 20.9%, Dell 18.2%, Palantir 16.7% and AMD 15.6%. CoreWeave collapsed 45.6% this month. Yields on CoreWeave’s 9% 2031 bond surged 255 bps to 11.47%. Oracle CDS jumped 37 bps during November to 120 bps, with prices up 75 bps over three months. After trading at 6.0% on October 3rd, yields on Oracle’s 5.95% 2055 bond jumped 45 bps to end November at 6.45%.

Bitcoin sank $18,700, or 17%, during November. At November 21st lows, bitcoin was 26% lower m-t-d. Bitcoin ended the month down 28% from the October 6th intraday high (126,273). For the month, XRP was down 15%, Solana 26%, Binance Coin 26%, and Dogecoin 19%. Ethereum sank 21% in November, with prices off 39% from August highs.

The late-month recovery somewhat stabilized trading dynamics, but the cryptocurrencies have suffered a serious round of deleveraging. We can assume that huge amounts of leverage have accumulated in this highly speculative marketplace.

Doug's weekly commentary is always worth reading -- and this weekend's commentary showed up on his Internet site just before midnight PST last night. Another link to it is here.

![]()

Nigeria Ignites a Global Rebellion Against the Dollar Rule

What happened in Nigeria recently isn’t just another currency dispute. It’s the moment the American empire’s mask slipped completely off. President Trump just threatened military action against a sovereign African nation for making an economic decision about its own oil exports. Think about that for a second.

The U.S. is threatening war because Nigeria dared to accept payment in currencies other than the dollar. This isn’t diplomacy. This isn’t even traditional coercion. This is the desperate flailing of a declining empire that can no longer distinguish between its interests and the world’s interests. And the most shocking part Nigeria isn’t backing down.

For the first time in decades, we’re witnessing an African nation look the United States directly in the eye and say no, not just to our demands but to our threats. And that no is reverberating across every continent, inspiring other nations to question why they should continue submitting to American financial dominance. This moment will be remembered as the beginning of the end for dollar hegemony. But more than that, it reveals how completely Washington has lost touch with the reality of a multi-polar world where America’s word is no longer law. When Nigeria announced it would accept payment for oil exports in currencies other than the U.S. dollar, the reaction from Washington was swift and telling. Instead of diplomatic engagement or economic incentives, Trump’s response was immediate escalation.

Accept our currency dominance or face vicious military consequences. The language was deliberately threatening, designed to intimidate not just Nigeria but any other nation considering similar moves.

This article put in an appearance on the frontpageafricaonline.com Internet site on Friday -- and I found it embedded in a GATA dispatch. Another link to it is here.

![]()

Zimbabwe to raise royalties on gold producers amid bullion boom

Zimbabwe will hike royalties on gold producers as it moves to take advantage of recent record high bullion prices, a 2026 national budget speech showed on Thursday.

As part of a raft of revenue measures aimed at boosting state income and supporting local industry, gold miners will pay a 10% royalty if prices exceed $2,501 per ounce, according to the document.

"In order to ensure the mining sector contributes a fair share of revenue to the Fiscus during periods of commodity price boom, as well as eliminate arbitrage between categories of miners, I propose to harmonise and review the royalty structure for all gold producers," Finance Minister Mthuli Ncube was quoted as saying in the speech.

Zimbabwe largely relies on gold and tobacco exports for foreign exchange.

Its biggest gold producers include Kuvimba Mining House, Padenga, Caledonia Mining Corporation and Rio Zim.

This brief Reuters story, filed from Harare, showed up on their Internet site at 8:52 a.m. PST on Thursday morning -- and I found it embedded in a GATA dispatch. Another link to it is here.

QUOTE of the DAY

![]()

The WRAP

"Understand this. Things are now in motion that cannot be undone." -- Gandalf the White

![]()

Today's pop 'blast from the past' is one I've feature a couple of times before over the years, but it popped into my head when I saw the silver chart yesterday. It was by a British band that easily falls into the "one-hit wonder... but what a hit it was" category.

It was the main title theme to the film The Man from Hong Kong -- and was a worldwide hit in the latter part of 1975, reaching No. 3 on the Billboard Hot 100 and No. 4 on the Adult Contemporary chart in the United States.

It should be instantly recognizable -- and the link is here. There's a bass cover to this, of course, but there's not much to it. However, infusion26 lays it down just right -- and is linked here.

Today's classical blast from the past is Wolfgang Amadeus Mozart's Sinfonia Concertante for Violin, Viola and Orchestra in E♭ major, K. 364 which he composed in 1779 while on a tour of Europe that included Mannheim and Paris.

The solo viola part is written in D major instead of E♭ major...with the instrument tuned a semitone sharper (scordatura technique), to give a more brilliant tone. This technique is less common when performed on the modern viola and is used mostly in performance on original instruments. However, modern violists that choose to play scordatura the way Mozart originally composed it, will more easily project over the orchestra. Mozart didn't invent this technique...but used it to good effect in this work.

Here are Julian Rachlin & Sarah McElravy doing the honours...accompanied by the Norwegian-based Kristiansand Symphony Orchestra -- and this is as good as it gets. The link is here.

![]()

What a day! One doesn't know here to start...but it's a certainly appears that Ted Butler's "Bonfire of the Silver Shorts" was lit yesterday...but on very low holiday volume.

Gold's decent rally got it further above [almost $200] its 50-day moving average -- and it would certainly appear that the worst is behind us. It still has some ways to go before hitting overbought on its RSI trace.

Silver's second boomer rally of the week now has it back into overbought territory by a bit on its RSI trace...but if Ted's "bonfire" is allowed to run it course, then that won't matter. It's at a new nominal high -- and now $7+ bucks above its 50-day moving average.

Although silver closed higher by 5.80 percent on Friday, Nick's Silver Sentiment Index closed up only 6.62 percent. Despite silver's shiny new nominal high price, the silver shares still have a bit to go before they're at new highs as well.

Platinum shows a gap up on its 6-month chart after yesterday's price action ...but that's because Friday's candle contains Thursday's price activity as well. It had a big 'up' move on that day, despite the fact that New York was closed.

It was a wild trading session in palladium in its current front month...which is March, the same as silver...as it traded in a $153 price range on Thursday and Friday combined -- and is now a decent distance above its 50-day moving average.

Copper touched its 50-day moving average at its intraday low tick on Thursday, but by the time the Friday session was done...it finished up a net 6.5 cents at $5.187/pound.

Natural gas closed at a new high for this move up, as it finished the Friday trading session at $4.77/1,000 cubic feet...up a net 21 cents over the last two trading sessions. WTIC closed higher by 79 cents at $59.44/barrel.

Here are the 6-month charts for the above Big 6+1 commodities...thanks to stockcharts.com as always -- and are are worth a look if you have the interest. Don't forget that they include Thursday's price moves as well. Click to enlarge.

Since 'da boyz' set silver's intraday low tick for the current 'wash, rinse & spin' cycle back in very late October, it has tacked on almost 11 bucks since...with over half of that added since Monday's close.

I would suspect that a decent amount of the price activity we've seen this week involves short covering...especially on Wednesday and yesterday. There's lots more to come.

Silver open interest is down a bit more than 30,000 contracts since the middle of October...with some of that involving short covering by the bullion banks in the last Bank Participation Report headlined in one of my columns earlier this week. Right now, total silver o.i. is 151,796 COMEX contracts, which means that there are 151,796 short contract holders that are bleeding red ink -- and that's just one of four precious metals.

If one had put on a one contract short position in silver at the very end of October when 'da boyz' set its current low tick for this 'wash, rinse & spin' cycle, that short holder would have shelled out $11x5,000=$55,000 in margin calls by the COMEX close yesterday...plus the $3,000+ cost of the roll out of December and into March. For a small trader, that's a lot of money. What about those smaller traders that are short 10, 20, 35, 50 or more contracts -- and have been short for three months...or three years, or longer? You can do the math yourself.

Then there are the large traders that hold hundreds if not thousands of contracts? The Big 8 commercial traders are net short 64,483 COMEX silver contracts as of the last COT Report we have data for...October 14...about 8,000 contracts each. The shorts in gold and silver, collectively, have $60+ billion in unbooked margin call losses -- and are all screaming in pain. How soon will they be forced to cover regardless of the cost? That's what we're witness to at the moment.

Don't ever forget...as Ted Butler kept pointing out...a short contract, is an open contract -- and MUST be closed out at some point, regardless of what the price is. A short covering rally feeds on itself, like it's doing now -- and will at some point go parabolic...unless a short seller of last resort steps in front of the market, which has been happening with increasing frequency -- and again yesterday as well.

The question in our face now, is will the collusive commercial traders of whatever stripe step in front of this almost runaway upside move in silver like they did back October 17...yes, or no? That's all there is, there ain't no more -- and their treachery should never be underestimated when their backs are against the wall like they appear to be now.

But they can't keep it up forever -- and at some point there has to be a market-clearing event of some type...which will reset the prices in all four precious metals, plus copper -- and whole swath of other commodities as well. This will bring on the CME's and CFTC's 'disorderly market' scenario -- and who knows what the financial powers-that-be do then. Think about the LME nickel debacle of several years back...except in silver it will be thousands of times worse -- and global in scope.

Reader Paul Fitzgerald sent us market maven Alyosha's commentary from Friday on silver -- and here it is...

"COMEX silver made new contract highs in all listed months today and settled at an all-time high close. Any short positions from the beginning of time to the present are in debit tonight. The CME hasn’t hiked margins yet, but I wouldn’t be surprised if they do it on Monday. Remember, higher margins put pressure on the weak side of the market.

Chinese inventories are at decade lows and Shanghai vaults drew down another 1.8 mm toz last week. According to Metals Focus, India imported 51 mm toz in October so they’re probably still on the bid. According to the post, most of it came from London; China was the second-largest source at 12 mm toz. The structural shortage is increasing. This is another AI energy story vis a vissolar PV.

I don’t have access to precise daily spot flows in and out of NY warehouses, but in general from what I can glean on the CME website, more than 50 million toz have gone from NY to London since October 1, [It's 87.888 million troy ounces in actual fact -- Ed] and movement of physical silver through, into, and out of both NY and London has been extremely fluid, indicating global demand for physical XAG is hot. However, exchange open interest is very low in all-time samples, and silver is not a crowded COT spec futures trade.

There is no way of forecasting where or when silver prices will find balance now. Just tie a knot and hang on."

So...silver has the largest short position in the COMEX futures market of any commodity in world history -- and most likely has a new record high short position in SLV as of the market close yesterday. China's silver inventories are at 10-year lows...the LBMA is running on fumes & vapours -- and 88 million troy oz. has left the COMEX since October 1. India has been buying silver like there's no tomorrow in both September and October -- and its price in the futures market was set ablaze yesterday. Based on that, one would be correct in assuming that it days with a 2-digit price, are numbered.

I await the Sunday night Globex open in New York with more than passing interest.

I'm done for the day -- and the week -- and I'm still "all in."

See you here on Tuesday.

Ed

About the author

SUBSCRIBE: https://edsteergoldsilver.com/

Ed Steer’s Daily Analysis of the Gold and Silver Markets

After eight years of writing about the precious metals for Casey Research, the folks at Stansberry & Associates—who just recently purchased controlling interest in the company—decided that my ‘niche market’ column didn’t fit into their plans.

Since the time that Casey Research was kind enough to offer me a stand-alone column, it became their most highly-rated blog almost from the outset—and has remained that way up to this date...