The gold price traded quietly sideways for an hour once trading commenced at 6:00 p.m. EST on Thursday evening -- and at 8 a.m. China Standard Time on their Friday morning, it took off higher, only to run into the short sellers of last resort a bit under an hour later -- and an hour after that they'd sold it back below unchanged by a few dollars. It recovered a bit in short order -- and then didn't do much until around 8:20 a.m. in London. It began to head unevenly higher from there, but was tapped a bit lower until around 12:35 p.m. GMT -- and that lasted until about ten minutes before the COMEX open in New York. From that juncture it rallied quietly and a bit unevenly higher until the market closed at 5:00 p.m. EST.

The low and high ticks in gold were reported as $1,931.50 and $1,974.90 in the April contract. The April/June price spread differential in gold was $3.30...June/August was $3.70 -- and August/October was $4.00 an ounce.

Gold finished the Friday trading session at $1,972.90 spot, up $36.40 on the day. Net volume was very heavy at 227,000 contracts -- and there was a bit under 16,500 contracts worth of roll-over/switch volume on top of that...Mostly into June, with a bit into August.

Every rally attempt by silver in Far East trading was turned lower, but it was well bid at just below $25.10 spot the whole time. Like gold, it too began to head higher around 8:20 a.m. in London -- and its moon-shot rally starting at 9 a.m. in New York was capped and turned down hard in short order. But from there it continued its rally in a more subdued fashion. It ran into 'something' once again at 2:45 p.m. in after-hours trading, but shrugged that off in the last hour of trading.

The low and high ticks in silver were recorded by the CME Group as $25.155 and $25.92 in the May contract. The March/May price spread differential at the close in New York yesterday afternoon was the same tiny 0.7 cents an ounce -- May/July was 4.2 cents -- and July/September was 5.4 cents an ounce.

As Ted pointed out on the phone yesterday, the price spread differentials in the future months in silver have tightened up decent amounts since Thursday, an indication that the physical tightness in good delivery bars is getting even worse.

Silver finished the Friday trading session in New York at $25.725 spot, up 58.5 cents from Thursday. Net volume was a bit on the heavier side, but nothing really spectacular, at about 59,500 contracts -- and there was just about 12,800 contracts worth of roll-over/switch volume in this precious metal...mostly into July, with a bit into both September and December.

The platinum price rallied quietly until around 11:15 a.m. China Standard Time on their Friday morning -- and from that point it wandered quietly lower until its low tick was set very shortly after 10 a.m. in Zurich. It proceeded to crawl quietly higher from there until, like silver, it shot higher at the 9:30 a.m. equity market opens in New York. That was dealt with in short order -- and from shortly after the 11 a.m. EST Zurich close, it crept higher until the market closed at 5:00 p.m. EST. Platinum finished the Friday trading session in New York at $1,122 spot, up 43 dollars on the day.

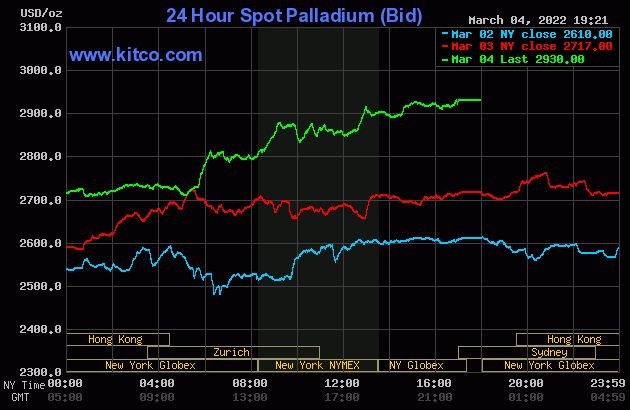

Palladium's rally in early morning trading in the Far East on their Friday was capped and turned lower very shortly before 10 a.m. China Standard Time -- and that lasted for about two hours. From there it didn't do a whole heck of a lot until around 11:15 a.m. in Zurich. From that point it stair-stepped its way quietly and aggressively higher until the market closed at 5:00 p.m. in New York. Platinum finished the day at $2,930 spot, up 213 bucks.

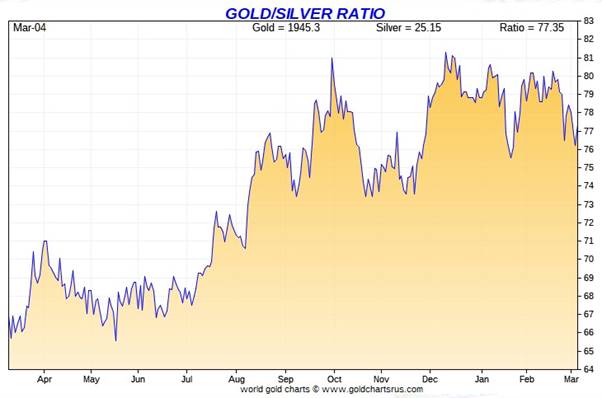

Based on the kitco.com spot closing prices in silver and gold posted above, the gold/silver ratio worked out to 76.7 on Friday...compared to 77.0 to 1 on Thursday.

Here's Nick Laird's 1-year Gold/Silver Ratio chart, updated with the last five trading days worth of data. Click to enlarge.

![]()

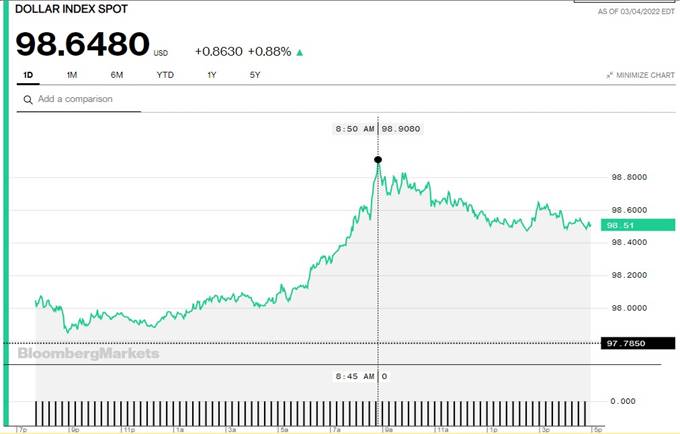

The dollar index closed very late on Thursday afternoon in New York at 97.785 -- and then gapped higher by 27.5 basis points once trading commenced around 7:45 p.m. EST on Thursday evening, which was 8:45 a.m. China Standard Time on their Friday morning. It had a very quiet up/down move to its low tick of the day, which was set a couple of minutes before 10 a.m. CST. From that juncture it wandered very quietly higher until the 'rally' became far more serious starting around 11:08 a.m. in London. The high tick was set at 8:50 a.m. in New York -- and it was all down hill from there until around 2:32 p.m. EST. A tiny rally at that point ended a couple of minutes before 3 p.m. -- and it then continued to chop quietly lower until the market closed at 5:00 p.m. EST.

The dollar index finished the Friday trading session in New York at 98.648...up 86.3 basis points from its close on Thursday -- and about 14 basis points above it indicated spot close on the DXY chart below.

Here's the DXY chart for Friday, thanks to Bloomberg as always -- and the above-mentioned discrepancy should be noted. Click to enlarge.

And here's the 5-year U.S. dollar index chart that appears in this spot in every Saturday column, courtesy of stockcharts.com as always. The delta between its close...98.67...and the close on the DXY chart above, was about 2 basis points above its spot close on Friday. Click to enlarge.

![]()

It's now obvious, that unless the powers-that-be wish it, the DXY has now become totally disconnected from what's happening in the precious metals...as both are rising at the same time.

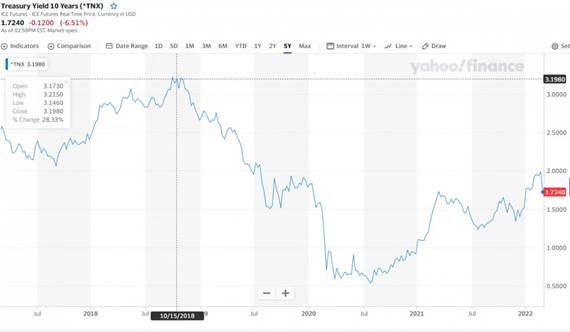

U.S. 10-Year Treasury: 1.7240%...down 0.1200 (-6.51%)...as of 02:59 p.m. EST

Here's the 5-year 10-year U.S. Treasury chart from the yahoo.com Internet site -- and it puts the yield curve into a somewhat longer-term perspective. Click to enlarge.

As you are more than aware, the only reason that yields are where they are, is because the central banks of the world continue to buy up almost all of the sovereign debt being issued. That isn't about to stop anytime soon, despite their preaching about higher interest rates -- and tapering. There isn't any tapering as far as the Fed is concerned, as their bond buying continues unabated...as it does at most of the rest of the world's major central banks.

![]()

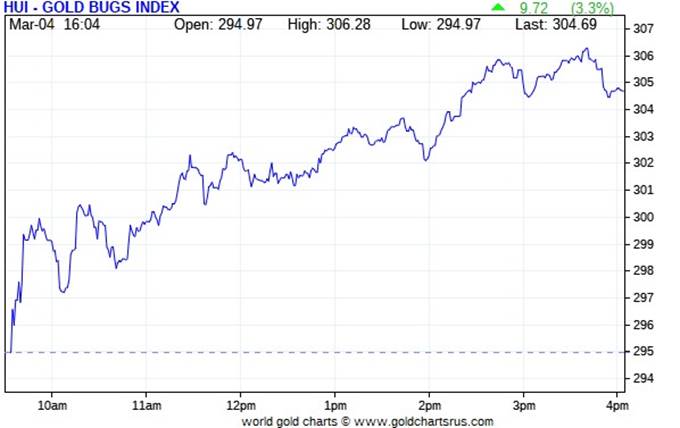

The gold stocks were in rally mode right from the 9:30 a.m. opens in New York on Friday morning -- and that continued until around 3:40 p.m. when there were sold a bit lower into the 4:00 p.m. close. The only reason that happened was because gold was tapped a few dollars lower at that time. The HUI finished the Friday session higher by 3.30 percent.

Computed manually, Nick Laird's Intraday Silver Sentiment/Silver 7 Index closed up a very unimpressive 1.99 percent...not helped at all by Peñoles or Hecla Mining.

And here's Nick's 3-year Silver Sentiment/Silver 7 Index chart, updated with Friday's candle. Click to enlarge.

The absolute star was Pan American Silver, as it closed higher by 4.15 percent. The two pooches were lead by Peñoles, as it actually closed down on the day by 0.35 percent -- and Hecla Mining only closed up by 0.43 percent. I was underwhelmed, as were you I'm sure.

In the interest of full disclosure, I added to my position in Ninepoint Silver Equities Fund yesterday, a mutual fund only available in Canada.

The latest silver eye candy from the reddit.com/Wallstreetsilver crowd is linked here.

![]()

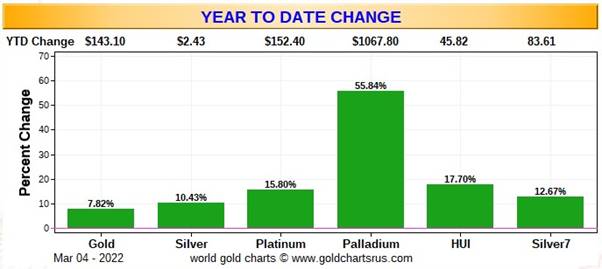

Here are two of the three usual charts that show up in every weekend missive. They show the changes in gold, silver, platinum and palladium in both percent and dollar and cents terms, as of their Friday closes in New York — along with the changes in the HUI and the Silver 7 Index.

Here's the weekly chart...which is all green for the second week in a row -- and the standout feature is the monster gain in palladium, as it closed higher by almost 600 bucks over the last five trading sessions. Silver and its equities outperformed their golden cousins this week, but not by a meaningful amount. Click to enlarge.

There's no month-to-date chart this week, as it's only four days long. It will reappear in this spot in next week's column.

Here's the year-to-date chart -- and the big gains of late has turned this chart all green as well...with the silver stocks being the underperformers vs. its underlying precious metal so far this year. That will change at some point. Palladium's gain year-to-date is nothing short of spectacular...but all it's doing, like the other three precious metals, is attempting to seek it's intrinsic/free-market value. Click to enlarge.

Of course how much longer these gains will be allowed to continue is in the hands of the commercial traders of whatever stripe, as they alone control everything precious metals-related...until the time that they don't.

![]()

The CME Daily Delivery Report showed that 420 gold and a 563 silver contracts were posted for delivery within the COMEX-approved depositories on Tuesday.

In gold, the sole short/issuer was Barclays out of its client account. The largest of the ten long/stoppers was BofA Securities, as they picked up 228 contracts for their house account. Next was the 53 contracts stopped by Australia's Macquarie Futures, followed by JPMorgan picking up 48 contracts. Both amounts were for their respective client accounts.

In silver, the sole short/issuer was JPMorgan out of its house account -- and I know Ted won't be happy to see that. There were five long/stoppers in total, the biggest being Wells Fargo Securities, stopping 195 contracts for its own account...followed by JPMorgan, as they picked up 162 contracts for clients.

This is the second time this week that JPMorgan has been forced to step in as a short/issuer, as someone who had gone long against them demanded delivery -- and they had to pony up. Or it could have been a situation where they had to step in order to prevent what might have been another potential COMEX delivery default.

I'm sure that Ted will have something to say about all this in his weekly review later this afternoon.

In palladium, there were 2 contracts issued and stopped.

The link to yesterday's Issuers and Stoppers Report is here.

Month-to-date there have been 4,101 gold contracts issued/reissued and stopped -- and that number in silver is 8,081 COMEX contracts. In platinum and palladium there have been 69 and 156 contracts stopped respectively.

The CME Preliminary Report for the Friday trading session showed that gold open interest in March increased by 17 contracts, leaving 1,936 contracts still open, minus the 420 contracts mentioned a few paragraphs ago. Thursday's Daily Delivery Report showed that zero gold contracts were posted for delivery on Monday, so that obviously means that 17 more gold contracts were added to March deliveries. Silver o.i. in March fell by 2,605 COMEX contracts, leaving 1,108 still around, minus the 563 contracts mentioned a few paragraphs ago. Thursday's Daily Delivery Report showed that 3,062 contracts were actually posted for delivery on Monday, so that means that 3,062-2,605=457 more silver contracts just got added to the March delivery month. That's a lot!

Total gold open interest at the close on Friday rose by an eye-watering 17,351 COMEX contracts -- and total silver o.i. increased by 4,760 contracts...with both numbers subject to some slight revisions, usually downwards, once the final number are posted on the CME's website later on Monday morning CST.

![]()

There was a fairly decent deposit into GLD and GLDM yesterday, as one or more authorized participants added 130,426 troy ounces of gold to the former -- and 79,193 troy ounces to the latter. There were no reported changes in SLV...which Ted feels is now owed something in the order of 20-25 million troy ounces.

And judging by the rate of deposits into SLV recently, along with the ongoing conversion of shares for physical, one would have to suspect that the authorized participants are shorting the shares in lieu of depositing physical metal. It's a near certainty that Ted will have something to say about this in his weekly review for his paying subscribers this afternoon.

The new short report comes out on Wednesday -- and it's most unfortunate that all of the activity in SLV since the February 28th cut-off, won't be in it.

And on a housekeeping note, Ted and I had a discussion about GLD vs. GLDM on the phone yesterday -- and after an e-mail exchange with Nick, I've discovered that I haven't been reporting their inventory additions and declines in my daily column, which I will start doing immediately...starting today if you noticed above.

Because of this comment from Ted yesterday, I inadvertently under-reported the amount of gold that was deposited in GLD and GLDM in my Friday column. I reported zero ounces for GLD, but 79,476 troy ounces was added to GLDM. I shall not overlook this data point again.

In other gold and silver ETFs and mutual funds on Planet Earth on Friday, net of any changes in COMEX, GLD/GLDM & SLV inventories, there was a net 199,772 troy ounces of gold added -- but a net 2,059,234 troy ounces of silver was taken out, with the lion's share of that coming from Deutsche Bank...1,869,598 troy ounces.

And because I overlooked that deposit in GLDM in yesterday's column, there was actually a net 152,166 troy ounces of gold added to those 'other gold and silver ETFs and mutual funds' on Thursday -- and not the 72,690 that I had reported.

There was no sales report from the U.S. Mint yesterday, so the month-to-date sales are only the ones that were reported on Thursday...8,500 troy ounces of gold eagles -- 5,000 one-ounce 24K gold buffaloes -- and 4,700 platinum eagles -- and zero silver eagles.

As I said in this space last Saturday, these numbers are far below what the mint is capable of producing, so it couldn't be more obvious that the mint is dragging its feet -- and not producing enough to meet demand as the law requires.

If they were producing enough silver eagles to meet demand, then premiums wouldn't be as outrageous as they are. So it's equally obvious that they're holding back production in order not to exacerbate the increasingly squeaky-tight physical market in good delivery bars.

And there's still no Q4/2021 Annual Report from the Royal Canadian Mint.

![]() .........

.........

There was only a small of activity in gold over at the COMEX-approved depositories on the U.S. east coast on Thursday. They reported receiving 13,305 troy ounces...all of which went into Brink's, Inc. There was 321.510 troy ounces/10 kilobars shipped out -- and that left the International Depository Services of Delaware.

There was some paper activity, as 36,422 troy ounces was transferred from the Registered category and back into Eligible. There were four depositories involved -- and the two largest were lead by the 25,648 troy ounces that departed Brink's, Inc. -- and the second biggest transfer was the 9,716 troy ounces that made that same trip over at Manfra, Tordella & Brookes, Inc. The link to all of Thursday's COMEX gold activity is here.

There was pretty decent activity in silver, as there always is. There was 922,883 troy ounces received -- and 73,598 troy ounces shipped out.

In the 'in' category, by far the largest amount was the 629,435 troy ounces/one truckload that arrived at CNT -- and the next biggest was the 286,461 troy ounces that was dropped off at Brink's, Inc. There remaining 6,986 troy ounces found a new home over at the Delaware Depository.

In the 'out' department, there was 70,829 troy ounces that departed CNT -- and the remaining 2,768 troy ounces left Brink's, Inc. There was no paper activity -- and the link to Thursday's COMEX silver activity is here.

It was also pretty busy over at the COMEX-approved gold kilobar depositories in Hong Kong on their Thursday. They reported receiving 600 kilobars...but shipped out 4,580 of them. Except for the 27 kilobars that departed Loomis International, the remaining in/out activity took place over at Brink's, Inc. as always. The link to that, in troy ounces, is here.

![]()

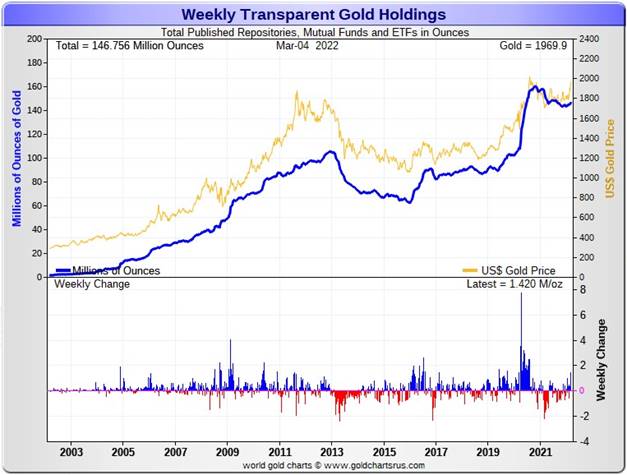

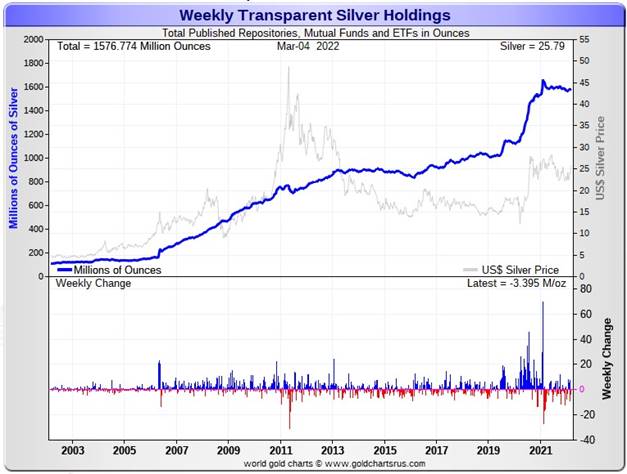

Here are the usual two 20-year charts that show up in this space every Saturday. They show the total amount of physical gold and silver held in all know depositories, ETFs and mutual funds as of the close of business on Friday.

During the week just past, there was a net 1,420,000 troy ounces of gold added -- but a net 3,395,000 troy ounces of silver was removed...with all of that amount, plus more, being conversions of SLV shares for physical...along with the big withdrawal from Deutsche Bank yesterday, that I mentioned above. Click to enlarge.

But in the overall, far more silver has been added to these various ETFs and mutual funds in last month, than has been withdrawn -- and even the withdrawals/exchange for physical in SLV are bullish as well.

And not to be forgotten is the fact that 20-25 million troy ounces of physical silver is owed to SLV, according to Ted.

The physical shortage situation in silver continues to creep along -- and the shrinking price spread differentials in silver since First Notice day is further proof that the physical silver noose is drawing ever tighter in the wholesale market.

Now that silver has broken above its 200-day moving average, ETF and mutual fund demand has exploded -- and retail demand continues to be incandescent.

Something's gotta give sooner or later.

![]()

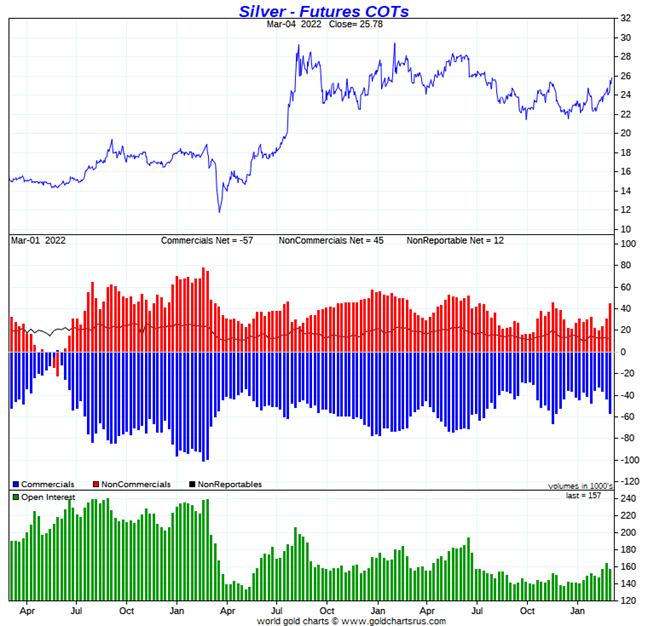

The Commitment of Traders Report for positions held at the close of COMEX trading on Tuesday showed the expected increases in the commercial net short positions in both gold and silver.

And also as expected, it was a Big 4/raptor affair in both...especially in silver, as is most always the case.

In silver, the Commercial net short position increased by a pretty hefty 13,430 COMEX contracts, or 67.2 million troy ounces.

They arrived at that number by decreasing their long position by 4,307 contracts -- and also increased their short position by 9,123 COMEX contracts. It's the sum of those two numbers that represents their change for the reporting week.

Under the hood in the Disaggregated COT Report, it was all Managed Money traders, plus a bunch more, as the increased their net long position by 16,646 COMEX contracts. The other two categories of reporting traders...the Other Reportables and the Nonreportable/small traders went in the opposite direction, as both reduced their net long positions during the reporting week, the former by 2,000 contracts -- and the latter groups by 1,216 contracts.

Doing the math: 16,646 minus 2,000 minus 1,216 equals 13,430 COMEX contracts, the change in the Commercial net short position.

The Commercial net short position in silver now sits at 285.8 million troy ounces...up 67.2 million troy ounces from the 218.6 million troy ounces that they were short in last Friday's COT Report...which is obviously the headline number change mentioned further up.

The Big 8 are short 334.5 million troy ounces in this week's COT Report, up 7.0 million troy ounces from the 327.5 million troy ounces they were short in last Friday's COT Report and, like last week, that all came courtesy of the Big 4 shorts, as the Big '5 through 8' did hardly anything.

The headline change in the Commercial net short position above showed an increase of 67.2 million troy ounces. So it was Ted's raptors once again, the small commercial traders other than the Big 8 shorts that made up the difference during the reporting week...to the tune of 67.2-7.0=60.2 million troy ounces...12,040 COMEX contracts...as they decreased their long position by that amount.

It was their selling of long positions that had the mathematical effect of increasing the commercial net short position.

Don't forget that despite their small size, Ted's raptors are still commercial traders in the commercial category.

The Big 8 are short 334.5/285.8 equals about 117 percent of the Commercial net short position in silver, down from the 150 percent they were short in last week's COT Report -- and all because of all the longs sold by Ted's raptors.

Here's the 3-year COT chart for silver, courtesy of Nick Laird as always. Click to enlarge.

Ho hum...it was yet another raptor/small commercial trader affair during the reporting week -- and that's been the case for many, many months now. The Big 4 shorts increased their net short position, but only by 7.0 million ounces...a drop in the bucket compared to the 334.5 million troy ounces that the Big 8 are currently short in total.

Ted's still of the opinion that there's a commercial trader that's long at least 15,000 COMEX contracts -- and they're hiding out in the Swap Dealer category. He's been mentioning that for a while now, as he's been watching their gross long position in that category creep up by that amount over time -- and it hasn't changed much, despite the price swings. Whoever that might be, it only adds to the bullish case for silver.

And from talking to Ted yesterday, nothing has changed regarding the above.

As you already know, the Big 4 shorts only added to their short position by a small amount during the reporting week -- and he thinks that they're being very cautious about increasing it, because they have been warned by the CFTC not to do so.

But his raptors are getting down to the point where they don't have all that many longs left to sell...9,740 contracts as of Tuesday's cut-off...and even less now. They rarely go on the short side -- and when they do, it's only by a few thousand contracts according to Ted.

So when they run out of long contracts to sell -- and if the Big 4 shorts don't want the silver price to rise further, then they'll have to step in on the short side in a major way. The question at that point will become...will they, or won't they? If they do, we're back to the "same old, same old". But if they don't...we'll have a 3-digit silver price in no time.

Silver is in rally mode now, but obviously being very carefully managed. How high it's allowed to go is entirely up to the commercial traders of whatever stripe...something you know all too well -- and that was on full display on Friday between 9:30 and 10 a.m. in New York...plus earlier in the day in morning trading in the Far East.

The current set-up in the COMEX futures market is still bullish, but obviously not quite as bullish as it was a week ago -- and the commercial net short position is up even more since the Tuesday cut-off...with two more trading days left in the next reporting week.

![]()

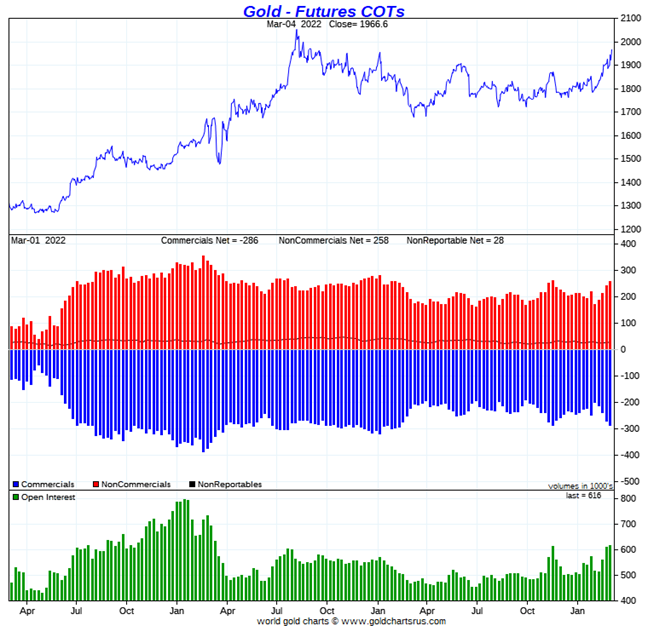

In gold, the commercial net short position rose by 16,087 contracts, or 1.61 million troy ounces of gold.

They arrived at that number by decreasing their long position by 2,451 contracts -- and also added 13,636 short contracts. It's the sum of those two numbers that represents their change for the reporting week.

Under the hood in the Disaggregated COT Report, the Managed Money traders only made up for part of the buying during the reporting week, as they increased their net long position by 9,645 COMEX contracts. The traders in the Other Reportables category also increased their net long position, them by 4,829 contracts...mostly by covering 4,607 short positions. The traders in the Nonreportable/small trader category followed the script as well, increasing their net long position by a further 1,613 contracts.

Doing the math: 9,645 plus 4,829 plus 1,613 equals 16,087 COMEX contracts, the change in the commercial net short position.

The commercial net short position in gold now sits at 28.58 million troy ounces, up 1.61 million troy ounces from the 26.97 million troy ounces they were short in last Friday's COT Report...which is obviously the change in the headline number further up.

The short position of the Big 8 traders is now 26.41 million troy ounces, up 850,000 troy ounces from the 25.56 million troy ounces they were short in last week's COT Report. As expected -- and for the third week in a row, it was the Big 4 that increased their net short position, while the Big '5 through 8' didn't do much.

The headline change in the commercial net short position showed an increased of 1.61 million troy ounces, so that means that Ted's raptors, the small commercial traders other than the Big 8, had to have sold 1.61-0.85=760,000 troy ounces/7,600 COMEX long contracts to make up the difference -- and that's what they did.

Their selling of long positions had the mathematical effect of increasing the commercial net short position by that amount. So it was 52% raptor/48% Big 8 commercial selling that accounted for this week's change.

And don't forget that despite their small size, Ted's raptors are still commercial traders in the commercial category.

From the above numbers, the Big 8 traders are short 26.41/28.58 equals about 92 percent of the commercial net short position in gold...down about 3 percentage points from the approximately 95 percent they were short in last Friday's COT Report.

This means that Ted's raptors, the small commercial traders other than the Big 8, are short the remaining 8 percent of the commercial net short position in gold.

Here's Nick Laird's 3-year COT chart for gold, updated with Friday's data. Click to enlarge.

Although Ted's raptors, the small commercial traders other than the Big 8 shorts, sold a lot of long positions during the reporting week, it was by no means enough -- and that forced the Big 4 shorts [for the third week in a row] to step in to the tune of around 8,500 contracts or so of new shorting, to prevent the gold price from blowing sky high, which it would have done if they hadn't.

And, without doubt, this same combination of selling by the Big 4 shorts and the small traders has continued since the Tuesday cut-off.

Ted's gold whale...whether it be John Paulson or BofA...is still there with about 35-40,000 long contracts in the Other Reportables category -- and he saw no change in that position during the reporting week just past.

Since the Tuesday cut-off, it's a given that there's been a further increase in the commercial net short position in both gold and silver...but there are still two more trading days between now and the Tuesday cut-off for next Friday's COT Report -- and with the state of the world these days, anything can happen -- and probably will.

But there's no question that gold is now in bearish territory -- and it remains to be seen if the commercial traders of whatever stripe can engineer another price decline in the current economic and political environment.

But if there is a correction of any kind in any of the precious metals, it's my opinion that they're dips that should be bought.

![]()

In the other metals, the Managed Money traders in palladium, by increasing their net long position by 266 contracts during the reporting week, have flipped from being net short palladium, to being net long once again by 253 COMEX contracts. In platinum, the Managed Money traders increased their net long position by a tiny 195 contracts during the reporting week -- and are now net long the COMEX futures market by 12,565 COMEX contracts...about 19 percent of total open interest, down about 1 percentage point from last week. The Producer/Merchant category is still net short platinum big time, the only category that is. In copper, the Managed Money traders decreased their net long position by 2,267 COMEX contracts -- but are still net long copper by 30,352 COMEX contracts at the moment...about 759 million pounds of the stuff -- and about 16 percent of total open interest...about unchanged from what they were net long in last Friday's COT Report.

![]()

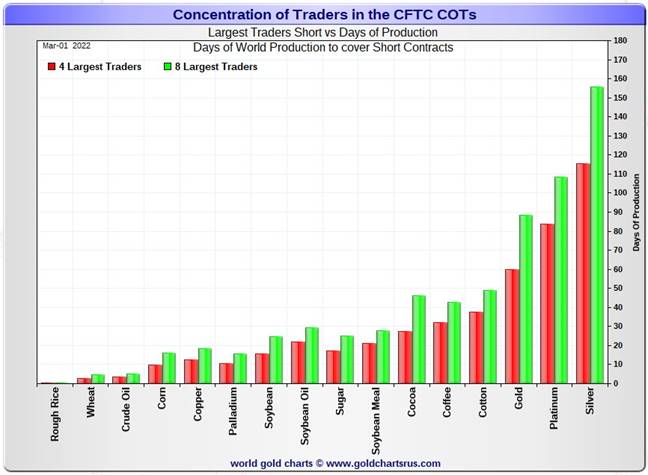

Here’s Nick Laird’s “Days to Cover” chart, updated with the COT data for positions held at the close of COMEX trading on Tuesday, March 1. It shows the days of world production that it would take to cover the short positions of the Big 4 — and Big '5 through 8' traders in each physically traded commodity on the COMEX.

I consider this to be the most important chart that shows up in the COT series -- and it always deserves a minute of your time. Click to enlarge.

In this week's 'Days to Cover' chart, the Big 4 traders are short about 115 days of world silver production, up about 3 days from last week's COT Report. The ‘5 through 8’ large traders are short an additional 41 days of world silver production, up about 1 day from last Friday's report, for a total of about 156 days that the Big 8 are short -- and up 4 days from last week's report. [In last Friday's COT Report, they were short 152 days of world production.]

That 156 days that the Big 8 are short, represents five months and a bit of world silver production, or 334.5 million troy ounces of paper silver held short by the Big 8 commercial traders.

In the COT Report above, the Commercial net short position in silver was reported by the CME Group at 285.8 million troy ounces. As mentioned in the previous paragraph, the short position of the Big 4/8 traders is 334.5 million troy ounces. So the short position of the Big 4/8 traders is larger than the Commercial net short position by 334.5-285.8=48.7 million troy ounces...down 60.2 million troy ounces from last week's COT Report...12,040 COMEX contracts...the amount of long contracts they sold during the past reporting week.

The reason for the difference in those numbers is that these raptors, the small commercial traders other than the Big 8, are net long silver by that amount...48.7 million troy ounces/9,740 COMEX contracts...which is getting close to the bottom of the barrel as I stated in my discussion in the COT Report for silver further up.

As per the first paragraph above, the Big 4 traders in silver are short around 115 days of world silver production in total. That's just about 29 days of world silver production each, on average...up a bit from last Friday's report. The traders in the '5 through 8' category are short 41 days of world silver production in total...10 days and a bit of world silver production each on average -- up a small amount from last week's COT Report.

The Big 8 traders are short 42.5 percent of the entire open interest in silver in the COMEX futures market, which is up from the 40.0 percent they were short in the last COT report. And once whatever market-neutral spread trades are subtracted out, that percentage would certainly be close to the 50 percent mark. In gold, it's 42.9 percent of the total COMEX open interest that the Big 8 are short, up a bit from the 41.8 percent they were short in last Friday's COT Report -- and also close to the 50 percent mark once their market-neutral spread trades are subtracted out.

In gold, the Big 4 are short 60 days of world gold production, up 3 days from last Friday's COT Report. The '5 through 8' are short 28 days of world production, down about 1 day from last week...for a total of 88 days of world gold production held short by the Big 8 -- and up 2 days from last Friday's COT Report. Based on these numbers, the Big 4 in gold hold about 68 percent of the total short position held by the Big 8...up about 2 percentage points from last Friday's COT Report.

Of course the 3-day jump in the Big 4 short position in gold was because of the approximately 8,500 contracts they were forced to go short during this past reporting week as mentioned in the above COT Report.

The "concentrated short position within a concentrated short position" in silver, platinum and palladium held by the Big 4 commercial traders are about 74, 78 and 63 percent respectively of the short positions held by the Big 8...the red and green bars on the above chart. Silver is about unchanged from last week...platinum is down about 1 percentage point from a week ago -- and palladium is down about 4 percentage points week-over-week.

So still nothing has changed. The Big 4/8 traders are still very firmly stuck on the short side in both gold and silver -- and increased their net short position in gold and silver by very decent amounts for the third reporting week in a row...and it was all the Big 4..as the Big '5 through 8' didn't do a thing. As Ted has been saying, it's his raptors, the small commercial traders other than the Big 8, that are mostly running the price management show...especially in silver. That was the case during this last reporting week as well -- and in the many weeks/months preceding that. The Big 4 were obviously active in capping their respective prices when necessary, especially in gold, while the Big '5 through 8 shorts' just sat on their hands.

As I've pointed out before -- and will mention again, the Big 4/8 shorts will never be able to extricate themselves fully from the short side, if that was ever their intent...particularly the Big 4. At some point they're going to have eat the lion's share of the short positions that they currently hold. The only way that can do that is to go into the market and buy longs...or deliver physical metal, but only if the long holders are in a position to accept delivery. A lot of them aren't.

And the moment the rest of the traders in the COMEX futures market sees that, the 'ask' will disappear -- and prices will explode...unless the powers-that-be at the CFTC and CME Group have something nefarious up their sleeves, or they're bailed out by the likes of the Exchange Stabilization Fund.

However, the circumstance in silver have been altered by an unimaginable [and monstrously bullish] amount by Ted's discovery of the approximately 800 million troy ounce physical short position in silver that Bank of America now holds in the OTC market.

He has also come to the conclusion that BofA is short about 30 million ounces of gold in the OTC market as well.

The situation regarding the Big 4/8 shorts in silver, gold [and platinum] continues to be far beyond obscene, twisted and grotesque -- and has been getting worse over the last three weeks. As Ted correctly points out ad nauseam, its resolution will be the sole determinant of precious metal prices going forward.

As always, nothing else matters.

![]()

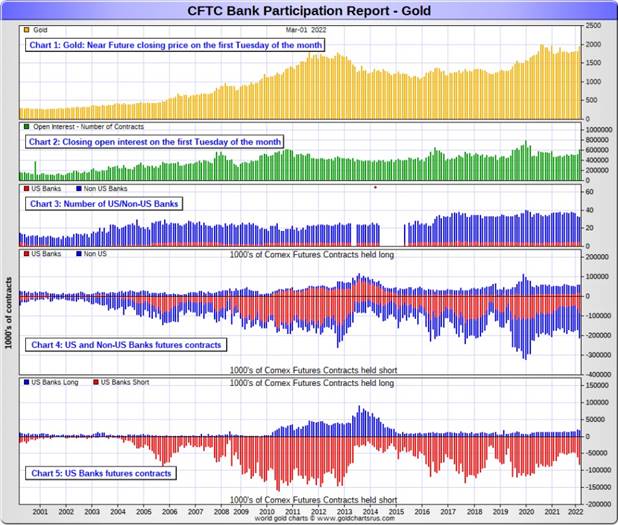

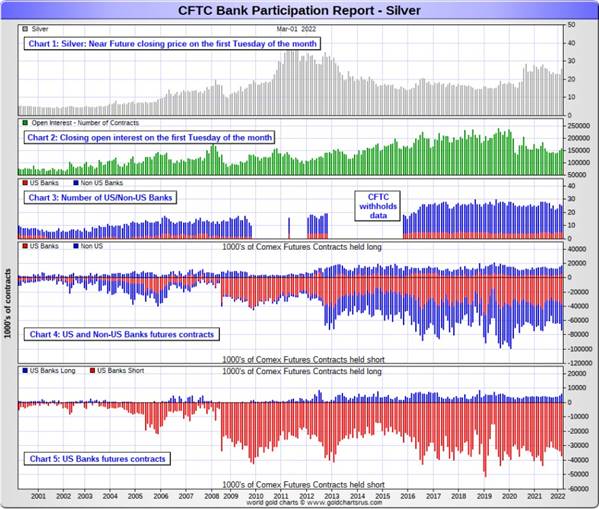

The March Bank Participation Report [BPR] data is extracted directly from yesterday's Commitment of Traders Report. It shows the number of futures contracts, both long and short, that are held by all the U.S. and non-U.S. banks as of Tuesday’s cut-off in all COMEX-traded products. For this one day a month we get to see what the world’s banks are up to in the precious metals. They’re usually up to quite a bit -- and they certainly were this past month.

[The March Bank Participation Report covers the time period from February 1 to March 1 inclusive.]

In gold, 5 U.S. banks are net short 64,587 COMEX contracts in the March BPR. In February’s Bank Participation Report [BPR] these same 5 U.S. banks were net short 39,518 contracts, so there was a whopping big increase of 25,069 COMEX contracts month over month. That's the third month in a row that the U.S. banks have increased their short position in gold.

Citigroup, HSBC USA, Bank of America and Morgan Stanley would most likely be the U.S. banks that are short this amount of gold. I still have my usual suspicions about the Exchange Stabilization Fund, although if they're involved, they are most likely just backstopping these banks.

Also in gold, 27 non-U.S. banks are net short 92,025 COMEX gold contracts. In February's BPR, 28 non-U.S. banks were net short 72,945 contracts...so the month-over-month change shows a big increase of 119,080 COMEX contracts. But it's their first increase in the last three months.

At the low back in the August 2018 BPR...these same non-U.S. banks held a net short position in gold of only 1,960 contacts -- and they've been back on the short side in an enormous way ever since.

I suspect that there's at least three large banks in this group, HSBC, Barclays and Deutsche Bank. I also have my suspicions about Scotiabank/Scotia Capital, Dutch Bank ABN Amro, French bank BNP Paribas, plus Australia's Macquarie Futures as well. Other than that small handful, the short positions in gold held by the vast majority of non-U.S. banks are immaterial and, like in silver, have always been so.

As of this Bank Participation Report, 32 banks [both U.S. and foreign] are net short 25.4 percent of the entire open interest in gold in the COMEX futures market, which is up a bit from the 21.9 percent that 33 banks were net short in the February BPR.

Here’s Nick’s BPR chart for gold going back to 2000. Charts #4 and #5 are the key ones here. Note the blow-out in the short positions of the non-U.S. banks [the blue bars in chart #4] when Scotiabank’s COMEX short position was outed by the CFTC in October of 2012. Click to enlarge.

In silver, 5 U.S. banks are net short 31,126 COMEX contracts in March's BPR. In February's BPR, the net short position of these same 5 U.S. banks was 28,830 contracts, which is only up about 2,300 contracts month-over-month...not a big change. This is the fifth month a row where there has been no material change in the short position in silver held by these 5 U.S. banks. That shows you how careful they've been not to go back on the short side in a big way.

The biggest short holders in silver of the five U.S. banks in total, would be Citigroup, HSBC USA, Bank of America, Morgan Stanley...and now Goldman Sachs...but not JPMorgan according to Ted. And, like in gold, I have my suspicions about the Exchange Stabilization Fund's role in all this...although, also like in gold, not directly.

Also in silver, 20 non-U.S. banks are net short 26,224 COMEX contracts in the March BPR...which is up a pretty hefty amount from the 19,974 contracts that 21 non-U.S. banks were short in the February BPR.

I would suspect that HSBC and Barclays holds a goodly chunk of the short position of these non-U.S. banks...plus some by Canada's Scotiabank/Scotia Capital still. I'm not sure about Deutsche Bank... but now suspect Australia's Macquarie Futures. I'm also of the opinion that a number of the remaining non-U.S. banks may actually be net long the COMEX futures market in silver. But even if they aren’t, the remaining short positions divided up between these other 15 or so non-U.S. banks are immaterial — and have always been so.

As of March's Bank Participation Report, 25 banks [both U.S. and foreign] are net short 36.4 percent of the entire open interest in the COMEX futures market in silver— up from the 32.7 percent that 26 banks were net short in the February BPR. And much, much more than the lion’s share of that is held by Citigroup, HSBC, Bank of America, Barclays -- and Scotiabank -- and possibly one other non-U.S. bank...all of which are card-carrying members of the Big 8 shorts.

I'll point out here that Goldman Sachs, up until late last year, had no derivatives in the COMEX futures market in any of the four precious metals, but did show up in the last OCC Report as being short a bit...most likely in silver.

Here’s the BPR chart for silver. Note in Chart #4 the blow-out in the non-U.S. bank short position [blue bars] in October of 2012 when Scotiabank was brought in from the cold. Also note August 2008 when JPMorgan took over the silver short position of Bear Stearns—the red bars. It’s very noticeable in Chart #4—and really stands out like the proverbial sore thumb it is in chart #5. But as of March of 2020...they're out of their short positions, not only in silver, but the other three precious metals as well. Click to enlarge.

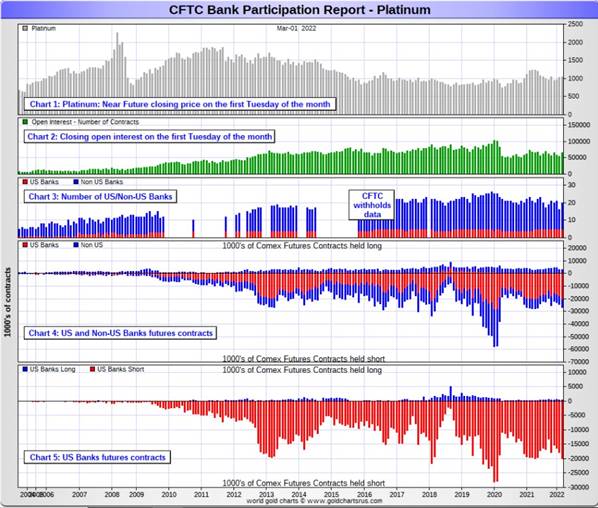

In platinum, 5 U.S. banks are net short 19,622 COMEX contracts in the March Bank Participation Report, which is up 2,259 contracts from the 17,363 COMEX contracts that these same 5 U.S. banks were short in the February BPR.

I will point out here that this is the third month in a row that these 5 U.S. banks have increased their collective short positions in platinum...the Big 8 shorts No. 2 problem child after silver.

At the 'low' back in July of 2018, these U.S. banks were actually net long the platinum market by 2,573 contracts. So they have a very long way to go to get back to just market neutral in platinum...if they ever intend to, that is.

Also in platinum, 15 non-U.S. banks are net short 3,960 COMEX contracts in the March BPR, which is down about 100 contracts from the 4,048 COMEX contracts that 11 non-U.S. banks were net short in the February BPR.

[Note: Back at the July 2018 low, these same non-U.S. banks were net short only 1,192 COMEX contracts in platinum.]

And as of March's Bank Participation Report, 20 banks [both U.S. and foreign] are net short 36.1 percent of platinum's total open interest in the COMEX futures market, which is down a bit from the 39.7 percent that 16 banks were net short in February's BPR.

But it's the U.S. banks that are on the short hook big time -- and the real price managers. They have little chance of delivering into their short positions, although a very large number of platinum contracts have already been delivered during the last year or so. But that fact, like in both silver and gold, has made no difference whatsoever to their short positions held. The situation for them in this precious metal is as equally dire in the COMEX futures market as it is with the other two precious metals...silver and gold...particularly the former.

The reason that they'll never improve their short positions in a big way is the same reason as in gold and silver...the Managed Money traders flatly refuse to go short big time like they used to in the past -- and they're actually net long about 12,600 COMEX contracts at the moment.

Here's the Bank Participation Report chart for platinum. Click to enlarge.

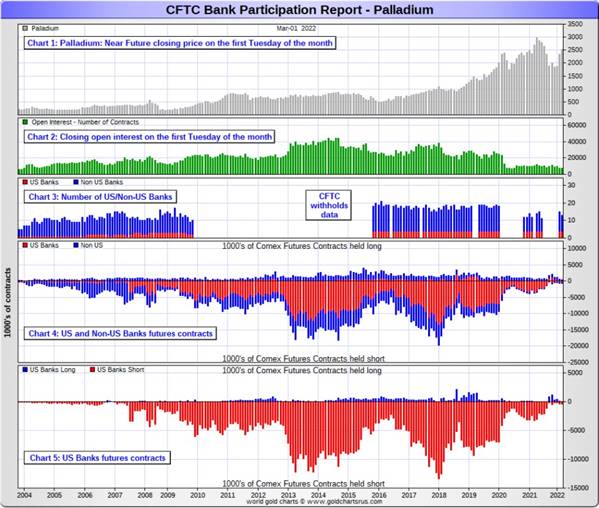

In palladium, 4 U.S. banks are have gone from being net long 306 COMEX contracts in February's BPR, to being net short 385 COMEX contracts in the March BPR. That may not seem like a lot, but in the thinly-traded and very illiquid futures market in palladium, it's quite a bit.

Also in palladium, 9 non-U.S. banks are now back to being net long 130 COMEX contracts in the March BPR, from 11 non-U.S. banks that were net short 86 contracts in February.

And as I've been commenting for almost forever now, the COMEX futures market in palladium is a market in name only, because it's so illiquid and thinly-traded. Its total open interest at Tuesday's cut-off was only 7,242 contracts...compared to 65,383 contracts of total open interest in platinum...157,391 in silver -- and 615,600 COMEX contracts in gold.

The only reason that there's a futures market at all in palladium, is so that the Big 8 traders can control its price. That's all, there ain't no more.

As of this Bank Participation Report, 13 banks [both U.S. and foreign] are net short 1.8 percent of the entire COMEX open interest in palladium...compared to the 2.8 percent of total open interest that 15 banks were net long in February's BPR.

And because of the small numbers of contracts involved, along with a tiny open interest, these numbers are pretty much meaningless.

But, having said that, for the last two years in a row, the world's banks have not been involved in the palladium market in a material way.

Here’s the palladium BPR chart. Although the world's banks are market neutral at the moment, it remains to be seen if they return as big short sellers again at some point like they've done in the past. Click to enlarge.

Excluding palladium for obvious reasons, only a small handful of the world's banks, most likely four or so in total -- and mostly U.S-based, except for HSBC, Barclays and maybe Deutsche Bank...continue to have meaningful short positions in the other three precious metals. It's a near certainty that they run this price management scheme from within their own in-house/proprietary trading desks...although it's a given that some of their their clients are short these metals as well.

The futures positions in silver and gold that JPMorgan holds are immaterial -- and have been since March of 2020...according to Ted Butler. And what positions they do hold, would certainly be on the long side of the market. It's the new 7+1 shorts et al. that are on the hook in everything precious metals-related.

And as has been the case for over a year now, the short positions held by the Big 4/8 traders/banks is the only thing that matters...especially the short positions of the Big 4 -- and how it is ultimately resolved [as Ted said earlier] will be the sole determinant of precious metal prices going forward.

The Big 8 shorts, along with Ted's raptors...the small commercial traders other than the Big 8 commercial shorts...continue to have an iron grip on their respective prices -- and nothing has changed in that regard over the last month. They continue to be the corks in the precious metal price bottle.

That situation will persist until they either voluntarily give it up...or are told to step aside, as it now appears that there's no chance that they will ever get overrun. If that possibility had ever existed in reality, it would have happened already. However, considering the current state of affairs in the world today -- and the looming physical shortage in silver, I suppose one shouldn't rule it out entirely.

I have a lot of stories, articles and videos for you again today, including a couple I've been saving for today's column for length and/or content reason.

![]()

CRITICAL READS

February jobs rose a surprisingly strong 678,000, unemployment edged lower while wages were flat

Job growth accelerated in February, posting the biggest monthly gain since July as the employment picture got closer to its pre-pandemic self.

Nonfarm payrolls for the month grew by 678,000 and the unemployment rate was 3.8%, the Labor Department’s Bureau of Labor Statistics reported Friday.

That compared with estimates of 440,000 for payrolls and 3.9% for the jobless rate.

In a sign that inflation could be cooling, wages barely rose for the month, up just 1 cent an hour, or 0.03%, compared with estimates for a 0.5% gain. The year-over-year increase was 5.13%, well below the 5.8% Dow Jones estimate as more lower-wage workers were hired and 12-month comparisons helped mute more recent gains.

For the labor market broadly, the report brought the level of employed Americans closer to levels before the Covid crisis, though still short by 1.14 million. Labor shortages remain a major obstacle to fill the 10.9 million jobs that were open at the end of 2021, a historically high gap that had left about 1.7 vacancies per available worker.

At least from an employment perspective, the February report confirms that the rampant omicron spread during the winter had little impact.

“This report indicates that the job market is healthy and resilient to the ebbs and flows of the pandemic,” said Daniel Zhao, senior economist for job placement site Glassdoor. “We’ve seen that job gains have been over 400,000 for 10 months in a row.”

As time goes along, I keep getting ever more suspicious of the numbers coming out of the BLS -- and you should read this with a very open mind. This CNBC news item appeared on their website at 8:30 a.m. EST on Friday morning -- and was updated about four hours later. Another link to it is here -- and I thank Swedish reader Patrik Ekdahl for sending it along. The Zero Hedge spin on this is headlined "February Payrolls Smash Expectations Surging to 678K, Highest Since July, But Wages Disappoint" -- and comes courtesy of Brad Robertson.

![]()

![]()

What Will Eventually Cause the Collapse? -- Dennis Miller

Subscriber Steve F. asked Chuck Butler and me what we meant when we said the Fed and government is destroying the economy and wealth of the nation:

“That seems like a subject the average Joe can get his or her head around. Why not put together what that would really look like for us?”

We discussed the subject at great length and wrote about it. I want to expand the discussion with some outtakes of our conversations.

“Markets can stay irrational longer than you can stay solvent.” — John Maynard Keynes

I was uncomfortable with our response. What if we are wrong? We have been anticipating an economic collapse for over a decade, for good reason, yet it has not happened – yet!

Chuck says, “I’ve been like the doomsayer with the sandwich board that says the end is near, for a long-time regarding debt… Just because something is inevitable, doesn’t mean it is imminent.”

Hmm…. what will cause inevitable and imminent to meet?

Start with irrational government spending. Here’s the U.S. Debt Clock, dated February 2012. Our national debt was just under $15 trillion and our annual budget deficit was $1.2 trillion.

Fast forward to February 2022. In a decade, U.S. debt doubled, and the budget deficit is approaching $3 trillion.

If the Fed stops buying government and corporate bonds, the additional interest cost could easily add $1 trillion to the annual deficit.

This longish but interesting commentary from Dennis was posted on his website on Thursday -- and another link to it is here.

![]()

![]()

David Stockman on America's Debt Palooza... From $1 Trillion to $30 Trillion in a Heartbeat

My, how the frog does boil!

Recently, the national debt (aka public debt) crossed the $30 trillion milestone, yet neither Wall Street nor Washington took note. But it did catch our attention and we want to recall why a young budget director was thumping on the Gipper’s chest in the Oval Office photo below.

Namely, we were informing him of the distinctively unwelcome news that the $846 billion public debt we had inherited in December 1980 — which had been accumulated over 190 years by 39 presidents — was already surging within days of the Reagan inauguration. Accordingly, within a matter of just weeks there would be no choice but to ask Congress to raise the debt ceiling above the dreaded $1 trillion mark.

Exactly 41 years later, the public debt — measured appropriately at market value — stands at $30.7 trillion, a figure 36-fold larger than the figure being discussed in the “conversation” below.

This brief commentary from David put in an appearance on the internationalman.com Internet site on Friday sometime -- and another link to it is here.

![]()

![]()

[P]anic buying overwhelmed global commodities markets. The Bloomberg Commodities Index surged 13.0% to the high since 2014 - the “most stunning weekly surge in records that go back to when Nikita Khrushchev was in the Kremlin.” WTI Crude jumped $24.09, or 26.3%, to $115.58 (up 54% y-t-d).

Palladium jumped 27.1%, Nickel 18.7%, Iron Ore (DCE) 15.5%, Aluminum 14.6%, Zinc 11.9%, Copper 10.1%, and Tin 6.9%. In the precious metals, Golds rose 4.3%, Silver 5.9%, and Platinum 6.5%. Too much “money” chasing limited supplies.

It was an ominous week for the global food supply and its price. Wheat (May contract) surged 40.6%, increasing y-t-d gains to 57%. Corn jumped 15% (up 27% y-t-d), and Soybeans rose 5.4% (up 26%).

Here at Day Nine, Everything Has Changed. The Fed and global central bank community have no solutions for the worst European military crisis since WWII. No solutions for spiking energy, food and materials prices. No solution for unfolding shortages of so many vital commodities. No solution for panic buying. No solution if China decides to use its horde of dollars to procure additional supplies of commodities – at any price. No solution for a worsening global supply chain crisis.

No solution for Russian bank insolvencies, collapsing securities values and illiquidity.

None for the paralyzed Central Bank of the Russian Federation. No solution for a new “iron curtain.” No solution for the risk of a nuclear crisis (damaged energy facilities or warheads). No solution for the risk of war expanding to include the U.S. and NATO. There is today little central bankers can say or do to mitigate the myriad risks that have overwhelmed the markets and world.

This commentary from Doug put in an appearance on his website in the very early hours of Saturday morning PDT -- and another link to it is here.

![]()

![]()

There are a lot of 'fog of war' stories to pick and choose from -- and I've linked the headlines for some of them...

1. "Putin tells Macron Russia will achieve its goals in Ukraine" - Reuters - Credit: Patrik Ekdahl

2. "Financial screws turned on Russia as insurers exit, London stocks halted" - Reuters - Credit: Patrik Ekdahl

3. "Russia Likely to Miss Interest Payment for First Time Since 1998 Crisis" - The Wall Street Journal - Credit: Patrik Ekdahl

4. "Putin’s energy shock is broadening into a world food crisis, so brace for rationing" - The Telegraph - Credit: GATA

5. "Ukraine’s NATO Membership 'Will Not Take Place': German Chancellor" - Zero Hedge

6. "JP Morgan, Goldman Scoop Up Distressed Russian Assets As Analysts Fret About Economic Collapse" - Zero Hedge

![]()

![]()

An interesting view from a Norwegian about Zbigniew Brzezinski and the U.S. attempts to dominate the world

The big elephant in the room during the Ukraine conflict is not much mentioned in the big mass media. But without understanding this factor, it is not possible to understand what is happening in Ukraine now. I’m talking about the United States’ strategy for dominating the Eurasian continent, which was formulated after the dissolution of the Soviet Union and the United States helped Yeltsin to cut the lead in Russia. The strategy was summarized by Zbigniew Brzezinski in the book The Great Chessboard from 1997 and followed up during Obama’s election campaign in 2009 with Second Chance which was the basis for Obama’s foreign policy. Brzezinski then also became Obama’s most important informal adviser.

The main idea behind this strategy was that the United States should rule the whole world. To do so, they had to take control of the states on the Eurasian continent, so that no state there became so strong that it could challenge the hegemony of the United States. Ideally, this should happen in a collaboration on the United States’ premises. If it this was not successful, the United States would have to maintain its power by other means, including wars, coups, regime changes, undermining activities and sanctions. All this is in publicly available in this public U.S. document.

In Ukraine, coups with regime change were used. Inside the country, there was intense work by Soros’ NGOs and cooperation with the powerful Nazi unions that secured the coup. Afterward, the friends of the Nazis from all over the world came there to fight the Russians in the Donbass, and then several of them went home to spread their knowledge in Europe and elsewhere.

The United States and the use of reactionary political directions

On the whole, the United States has been a master at educating and using people from such reactionary political directions. In Afghanistan, it was help from smuggled so-called radicalized Islamists who were locked in by the US through Koranic bullets in Pakistan who first did the job, and afterward there was direct war from the U.S. along with a number of vassals, including Norway. It is estimated that after the Soviet Union withdrew from Afghanistan, there were around 100,000 jihadists there. Many of them traveled out of Afghanistan and the United States used them in several sections, in North Africa, in Bosnia, in Chechnya, and in several places.

In Iraq, there were direct wars with American soldiers that managed regime change. In Libya, there was direct war and terrorist bombing plus cooperation with jihadists on the ground that did it. In Syria, violent jihadists were used, but then Russia had learned, among other things, so that the United States did not succeed there, even though with the help of Kurdish soldiers they kept the richest part of the country occupied, and the jihadists still occupy Idlib. This was part of the United States’ strategy to secure world domination. They are constantly striving to follow this strategy. The power of the United States over Ukraine was important for further aggression to the east.

This interesting and worthwhile commentary was posted on theduran.com Internet site last Sunday -- and I've been saving it for today's column. I've read Brzenzinski's book -- and mostly agree with what's in this article. It comes to us courtesy of Roy Stephens -- and another link to it is here.

![]()

![]()

The question to ask is what today’s New Cold War is trying to change or “solve.” To answer this question, it helps to ask who initiates the war. There always are two sides – the attacker and the attacked. The attacker intends certain consequences, and the attacked looks for unintended consequences of which they can take advantage. In this case, both sides have their dueling sets of intended consequences and special interests.

The active military force and aggression since 1991 has been the United States. Rejecting mutual disarmament of the Warsaw Pact countries and NATO, there was no “peace dividend.” Instead, the U.S. policy executed by the Clinton and subsequent administrations to wage a new military expansion via NATO has paid a 30-year dividend in the form of shifting the foreign policy of Western Europe and other American allies out of their domestic political sphere into their own U.S.-oriented “national security” blob (the word for special interests that must not be named). NATO has become Europe’s foreign-policy-making body, even to the point of dominating domestic economic interests.

The recent prodding of Russia by expanding Ukrainian anti-Russian ethnic violence by Ukraine’s neo-Nazi post-2014 Maiden regime was aimed at (and has succeeded in forcing a showdown in response the fear by U.S. interests that they are losing their economic and political hold on their NATO allies and other Dollar Area satellites as these countries have seen their major opportunities for gain to lie in increasing trade and investment with China and Russia.

To understand just what U.S. aims and interests are threatened, it is necessary to understand U.S. politics and “the blob,” that is, the government central planning that cannot be explained by looking at ostensibly democratic politics. This is not the politics of U.S. senators and representatives representing their congressional voting districts or states.

America’s three oligarchies in control of U.S. foreign policy

It is more realistic to view U.S. economic and foreign policy in terms of the military-industrial complex, the oil and gas (and mining) complex, and the banking and real estate complex than in terms of the political policy of Republicans and Democrats.

The key senators and congressional representatives do not represent their states and districts as much as the economic and financial interests of their major political campaign contributors. A Venn diagram would show that in today’s post-Citizens United world, U.S. politicians represent their campaign contributors, not voters.

This very long, but very worthwhile commentary from Michael Hudson was posted on the saker.is Internet site on Monday -- and for obvious length/content reasons, had to wait for today's column. Another link to it is here -- and that's from Roy Stephens as well. Gregory Mannarino's post market close rant for Friday is linked here.

![]()

Why does this influential, unelected globalist entity, the World Economic Forum, really exist?

When Canadian parliamentarian, Colin Carrie, of the Conservative Party, asked Prime Minister Justin Trudeau’s government this week how many Canadian ministers were actually “on board with the World Economic Forum agenda” — before his connection “broke up” in the video conference — he and the Canadians he represents deserved an honest response rather than accusations of spreading “disinformation”, as left-leaning New Democratic Party MP Charlie Angus did.

The World Economic Forum (WEF), colloquially known as “Davos”, for those familiar with the annual pilgrimage by the international elite to the eponymous town in Switzerland, has been on the tips of many tongues over the past two years — notably within the context of the Covid-19 crisis. Just before the Covid pandemic, on October 15, 2019, the organization announced that it was holding a “live simulation exercise to prepare public and private leaders for pandemic response.” If that sounds oddly coincidental, buckle up, because it only gets weirder.

Speaking at a United Nations video conference in the fall of 2020, Justin Trudeau raised eyebrows, with a hint of a potential link between the global pandemic and the Forum. "This pandemic has provided an opportunity for a reset," Trudeau said. "This is our chance to accelerate our pre-pandemic efforts, to re-imagine economic systems that actually address global challenges like extreme poverty, inequality and climate change,” he added, evoking a “reset” concept much promoted by the WEF from the onset of the pandemic, that frames the crisis as an opportunity to fundamentally change the way that developed societies function.

Then in August 2021, Dutch MP Gideon van Meijeren asked Prime Minister Mark Rutte about a letter he wrote to WEF Founder Klaus Schwab in which he said that Schwab’s book, “Covid-19: The Great Reset,” published on July 9, 2020, within the first few months of the pandemic, “inspired him to build back better.” The phrase also happens to be the name of U.S. President Joe Biden’s legislative agenda, which includes increased wealth transfer into the murky black hole of climate change and “social spending.”

It would be easy to chalk it all up to creepy rhetorical coincidence if there wasn’t an actual link between Schwab, Davos, and elected officials like Rutte and Trudeau. It’s a link about which even Schwab himself has bragged.

He’s not kidding. Current Canadian finance minister and deputy prime minister, Chrystia Freeland, is on the WEF’s board of trustees, alongside former Bank of Canada and Bank of England governor, Mark Carney.

This very worthwhile commentary by Rachel Marsden was posted on the rt.com Internet site a week ago today -- and obviously had to wait for today's column. I thank George Whyte for pointing it out -- and another link to it is here. It may take a bit to load, so be patient.

![]()

Despite all that's going on out there, I didn't find any precious metal stories I thought worth posting. However, two gold-related stories from yesterday's column are worth reading if you passed up on them the first time..."China almost certainly owns more gold than the U.S. – here’s why that matters" -- and "Alasdair Macleod: Financial war may crash euro system, end fiat Ponzi, exalt gold". The latter contains heavy references to gold towards the end...but is worth reading in its entirety, regardless.

![]()

The Photos and the Funnies

Continuing our ascent up the Thompson Plateau -- and deep into Douglas Lake CattleCompany territory on May 16. The first photo was taken looking up the road ahead -- and the hill in the middle distance is just about the highest point on this particular section of road. The second photo is my daughter standing besides one of the 'erratics' dumped by a glacier as it receded during the last ice age about 14,000 years ago. The third and fourth photos were taken from the same spot...the third looking in the direction we were headed -- and the fourth looking back over the part of the plateau that we'd just traversed. Click to enlarge.

![]()

The WRAP

“There are decades where nothing happens; and there are weeks where decades happen.” ― Vladimir Ilyich Lenin

![]()

Today's pop 'blast from the past' reached No. 1 on Billboard's Top 100 in 1972 -- and I remember spinning this particular '45' on 50-watt powerhouse CHAR FM radio in Alert, N.W.T. when I was working there as a weather observer in my early 20s. That's as far north you can go on Planet Earth and still be on dry land. That was 50 year ago now. Wow...where has the time gone? The link is here. I could hardly my eyes when I saw how many bass covers there were to this tune -- and it's a busy one. The best one I could find is here.

Today's classical 'blast from the past' is Mozart's Oboe Concerto in C major, K. 314, which was composed in the spring or summer of 1777, for the oboist Giuseppe Ferlendis (1755–1802) from Bergamo. In 1778, Mozart re-worked it as a concerto for flute in D major. The concerto is a widely studied piece for both instruments and is one of the most important concertos in the oboe repertoire.

Here's the Frankfurt Radio Symphony orchestra in a live recording from 14 October 2016, with Andrés Orozco-Estrada conducting. The soloist is François Leleux -- and what a showman he is -- and that's on top of his incredible gift. He's a master at his craft -- and I've seen none finer. No wonder it's had over 2.5 million views. The link is here.

![]()

![]()

With gold closing on its high tick of the day, it is now within spitting distance of $2,000 spot. However, I was none too happy to see total open interest blow out as much as it did yesterday -- and we're definitely in bearish territory in this precious metal from a COMEX futures market perspective after yesterday's price action.

I'm sure that the Big 4 were shorting this all the way up, as the raptors sold longs -- and it remains to be seen whether or not the commercial traders of whatever stripe will allow it to continue.

However, the possibility exists that they may be overrun by events and circumstance this time around. But as Ted Butler has pointed out for several decades now, if that does happen, it will be for the very first time.

As for silver, it turned in another stellar performance yesterday, although the share price activity was more than underwhelming. It's not nearly as bearish from as COT perspective as gold, but would certainly be included in any engineered price decline in that precious metal...along with platinum and palladium.

However, having said that, any engineered price decline, however violent, shouldn't last long -- and in the current environment, might represent one's last buying opportunity before we move much higher.

Not only is silver well above its 200-day moving average, but it also closed above its weekly moving average for the first time since mid-June of last year.

But the 800 lb. gorilla in the silver living room is the looming physical shortage, which now appears to be literally on our doorstep...that, combined with a short position in the COMEX futures and OTC markets that defies belief. Then there's the sharp narrowing of price spread differentials in silver since the March delivery month began...not to mention white-hot retail sales, the likes of which I've never seen before.

Platinum and palladium had huge 'up' days as well...particularly palladium.

But if you look at their respective Kitco charts at the top of today's column, you should note that the rallies in all four were being very carefully controlled. None of them were allowed to run away to the upside. It was most noticeable in silver and gold in early trading in the Far East on their Friday -- and then again starting at 9:30 a.m. in New York. The price control in the other two precious metals was far more subtle.

But, having said all that, it's more than noteworthy that the precious metals have been putting in decent rallies in the after-hours market all week long, with the biggest after-hours rally coming on a Friday, which is rare indeed. What it portends, remains to be seen.

Copper had another monster day, up 16 cent/pound -- and is up 50 cents for the week, which is a monster move for it. Natural gas [chart included] closed above $5.00/1,000 cubic feet by a couple of pennies -- and WTIC recouped all of its Thursday loss -- and then some, closing higher by $8.01/barrel at $115.68/per.

Here are the 6-month charts for the Big 6+1 commodities, thanks to stockcharts.com as always. And I'll point out once more that all of the considerable and very positive price action that occurred after the COMEX close yesterday, is NOT included on their respective candles on their respective charts below. Click to enlarge.

With the so-called Covid crisis now swept from the headlines, the deep state/New World Order crowd are now gunning for Putin and Russia -- and the 'fog of war' is getting thicker with each passing day.

As to how this is going to turn out in the weeks and months ahead is anyone's guess -- and I'm certainly not qualified to speculate on how this is going to shake out over time.

But the deep state/New World Order crowd now have Rahm Emanuel's famous quote tattooed on some body part..."You never let a serious crisis go to waste. And what I mean by that it's an opportunity to do things you think you could not do before."

And I'm sure they won't let this crisis go to waste, either. They may actually be fanning the flames with all this anti- Putin/Russia hysteria going around. All we can do is wait and see in what form it appears, if it does. Their Covid plans died on the vine, although it took a couple of years for the truth to finally do it in -- and this Russian 'excursion' into the Ukraine may work out even better for them.

Whether or not this includes all or part of the so-called "Great Reset" that "reimagines and reinvents our world" according to that psycho Klaus Schwab, is something I'm keeping an eye on...as should you.

But can they make it big enough and bold enough to let the big precious metals shorts off the hook, without having to close the COMEX in the process? A question of great urgency, with no answer at the moment. However, I get the impression that it's resolution is imminent.

But make no mistake about it, the world is changing very fast now -- and a catastrophic event of one type or another lies in our future, as the debt-based monetary system that has been foisted upon us for the last 50 years, is on its very last legs.

The world that emerges on the other side of that event...or events...will be a world that will be almost unrecognizable. The deep state/New World Order crowd has been leading western 'civilization' ever further down the Fascist/totalitarianism path for the last hundred years. They started slowly, but since the inside job that was 9/11 -- the pace has quickened considerably...especially over the last two years or so.

All we can do is to hope to survive it with our body -- and most of our wealth intact. The commodity complex in general -- and the precious metals in particular, are signs that 'Everything Bubble' in all things paper is getting very long in the tooth.

And if the precious metals are allowed to rise even further from here, the stampede into them will be impossible to stop -- and physical metal in both retail and wholesale form will vanish virtually overnight.

Then the central banks of the world will have fulfilled their goal of runaway inflation -- and will comfortably be able to lay the blame elsewhere.

It's for this very reason that I've been "all in" in the precious metals for as long as I have -- and under the present circumstances we find ourselves in, I'm quite content to be so.

See you here on Tuesday.

Ed

About the author

SUBSCRIBE: https://edsteergoldsilver.com/

Ed Steer’s Daily Analysis of the Gold and Silver Markets

After eight years of writing about the precious metals for Casey Research, the folks at Stansberry & Associates—who just recently purchased controlling interest in the company—decided that my ‘niche market’ column didn’t fit into their plans.

Since the time that Casey Research was kind enough to offer me a stand-alone column, it became their most highly-rated blog almost from the outset—and has remained that way up to this date...