Excerpt from this week's: Technical Scoop: War Spark, Signature Energy, Precious Life

The claim by Pakistan is that Iran/U.S. have agreed on a text for a deal that could get the Strait of Hormuz open once again. But then there are ongoing contradictory statements from both Iran and the U.S. Then we note that both Iran and the U.S. are still exchanging fire, despite a so-called deal in the works. So, which is it?

According to trackers, President Trump has declared that a peace deal is imminent at least 38 to 40 times – only to have the war renew once again, regardless of a ceasefire or that a deal is imminent. For investors, it is totally confusing and the reflection in the market is to watch oil prices collapse, only to regain and gold soar, and then to collapse once again. The stock market also responds, but its focus is on IPOs.

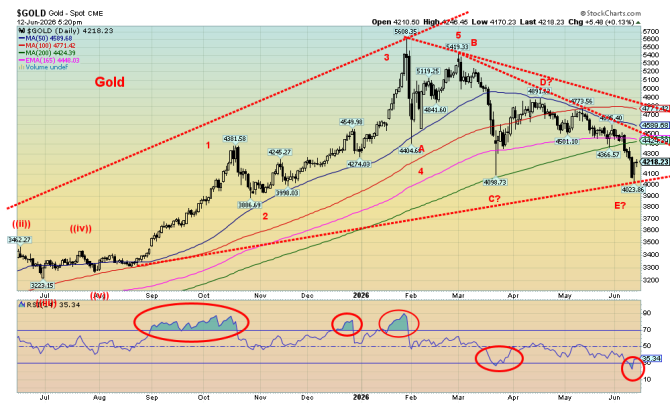

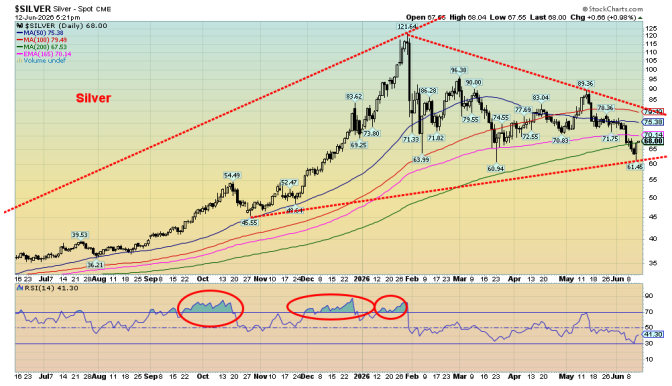

This past week oil fell, but gold barely recovered after falling earlier in the week. This past week gold fell 2.3% but silver rose 0.5%. Platinum was down 3% but palladium jumped 4.7% and copper prices were up again, gaining 3.7%. The gold stocks rose with the Gold Bugs Index (HUI) up 1.2% and the TSX Gold Index (TGD) gaining 0.9%. With silver outpacing, the gold/silver ratio fell 2.8% to 62.0.

What made this an interesting week was that gold made new lows for the move, but silver did not. The gold stocks (HUI, TGD) also made new lows for the move. This could be an interesting divergence if the relationship can hold and signal that a potential low is at hand.

Also encouraging from our standpoint is that copper prices are rising and gold and copper usually go hand in hand. Right now, gold is lagging as copper challenges all-time highs. The suggestion is that gold should rise again with copper. Given supply constraints for copper, we put less stead towards copper falling in sympathy for gold.

Source: www.stockcharts.com

Following the all-time high at $5,608 in January, the pattern for gold that has unfolded appears to us an ABCDE-type of correction. Silver that topped at $121.64 has followed the same pattern, as have the HUI and TGD. What we are seeing is that we may have made a low and completed the E wave down. Naturally, this is not confirmed, so making a pronouncement when we have no confirmation is just speculation.

To confirm, gold must regain back above $4,500 for starters and preferably over $4,800 and close over that level. For silver, we need to regain above $80 and then above $90 to convince us that a low is in. For the TGD, those points are over 890, then over 955. We have considerable work to do. And we must also not make any further lows. If that happens, then we know our E wave is not complete.

It has been a frustrating period for the gold bugs as the reason for holding gold has not gone away. Central banks continue to buy gold. We can’t help but note that foreign holdings of U.S. treasuries actually fell in March (latest report), down $138.4 billion. Notably, China’s holdings of U.S. treasuries fell $41 billion and are

down $113 billion in the past year. However, China’s gold holdings have gone up. Central banks added 244 tonnes of gold in Q1 alone, even as treasury holdings fell.

We are being driven back and forth by the Iran/U.S. war and the ongoing “we have a deal, no we don’t” seesaw. This coming week is the June FOMC and a surprise cut in interest rates would spark gold higher. Naturally, the consensus is stand to pat as inflation is not cooperating. That makes it hard to cut rates, regardless of the desires of President Trump.

We continue to hold that a low is at hand – if not in June, then by early July at the latest. The period from July–September is usually a positive seasonal bull period for gold.

Source: www.stockcharts.com

Read the FULL report here: Technical Scoop: War Spark, Signature Energy, Precious Life

Copyright David Chapman 2026

Disclaimer

David Chapman is not a registered advisory service and is not an exempt market dealer (EMD) nor a licensed financial advisor. He does not and cannot give individualised market advice. David Chapman has worked in the financial industry for over 40 years including large financial corporations, banks, and investment dealers. The information in this newsletter is intended only for informational and educational purposes. It should not be construed as an offer, a solicitation of an offer or sale of any security. Every effort is made to provide accurate and complete information. However, we cannot guarantee that there will be no errors. We make no claims, promises or guarantees about the accuracy, completeness, or adequacy of the contents of this commentary and expressly disclaim liability for errors and omissions in the contents of this commentary. David Chapman will always use his best efforts to ensure the accuracy and timeliness of all information. The reader assumes all risk when trading in securities and David Chapman advises consulting a licensed professional financial advisor or portfolio manager such as Enriched Investing Incorporated before proceeding with any trade or idea presented in this newsletter. David Chapman may own shares in companies mentioned in this newsletter. Before making an investment, prospective investors should review each security’s offering documents which summarize the objectives, fees, expenses and associated risks. Although Artificial Intelligence (AI) may be deployed from time to time, AI output is monitored and adjusted, if necessary, for accuracy. David Chapman shares his ideas and opinions for informational and educational purposes only and expects the reader to perform due diligence before considering a position in any security. That includes consulting with your own licensed professional financial advisor such as Enriched Investing Incorporated. Performance is not guaranteed, values change frequently, and past performance may not be repeated.

About the author

Website: https://www.enrichedinvesting.com

Disclaimer: David Chapman is not a registered advisory service and is not an exempt market dealer (EMD) nor a licensed financial advisor. We do not and cannot give individualised market advice. David Chapman has worked in the financial industry for over 40 years including large financial corporations, banks, and investment dealers. The information in this newsletter is intended only for informational and educational purposes. It should not be considered a solicitation of an offer or sale of any security. The reader assumes all risk when trading in securities and David Chapman advises consulting a licensed professional financial advisor before proceeding with any trade or idea presented in this newsletter. David Chapman may own shares in companies mentioned in this newsletter. We share our ideas and opinions for informational and educational purposes only and expect the reader to perform due diligence before considering a position in any security. That includes consulting with your own licensed professional financial advisor.